Business

$20,000 2-year CD could earn savers more, if rates hold

A 4.25% two-year CD on $20,000 would turn into about $21,736 before taxes, but the real-world payoff is thinner once Uncle Sam and inflation take their cut. Bankrate says the best CD rates are still above 4% APY, with its top tracked two-year offer at 4.25%, yet at a 22% federal tax rate on the interest and 4.2% annual inflation, that $20,000 grows to only about $19,667 in today’s dollars of buying power.

Why the insurance matters, and why it does not change the math

The safety backstop is solid: FDIC insurance covers at least $250,000 per depositor, per insured bank, per ownership category, and CDs are included alongside checking, savings, and money market deposit accounts. That protection matters, but it does not erase the cost of locking money away, because CDs are time deposits and early withdrawal penalties may apply; for noncompounding time accounts with stated maturities longer than one year, interest cannot remain on deposit and payout is mandatory.

That distinction is the whole story for ordinary savers. A CD can be safe and still be a poor fit if the real return is weak, especially when the account is meant to sit untouched for only two years. The insurance protects principal against bank failure, not against inflation, taxes, or the opportunity cost of tying up cash.

What a $20,000 two-year CD actually delivers

At 4.00% APY, $20,000 grows to about $21,632 after two years, which is $1,632 in gross interest. After a 22% federal tax on that interest, the gain falls to about $1,273, and the inflation-adjusted value slips to about $19,593 in today’s dollars. The top 4.25% offer improves the picture only slightly, lifting the nominal ending balance to about $21,736 and the inflation-adjusted value to about $19,667.

That means the extra 25 basis points from 4.00% to 4.25% buys you only about $104 more before tax over two years, and roughly $81 more after federal tax. It is an improvement, but not a windfall, and it shows why savers should focus on the entire yield after taxes and inflation rather than the headline APY alone.

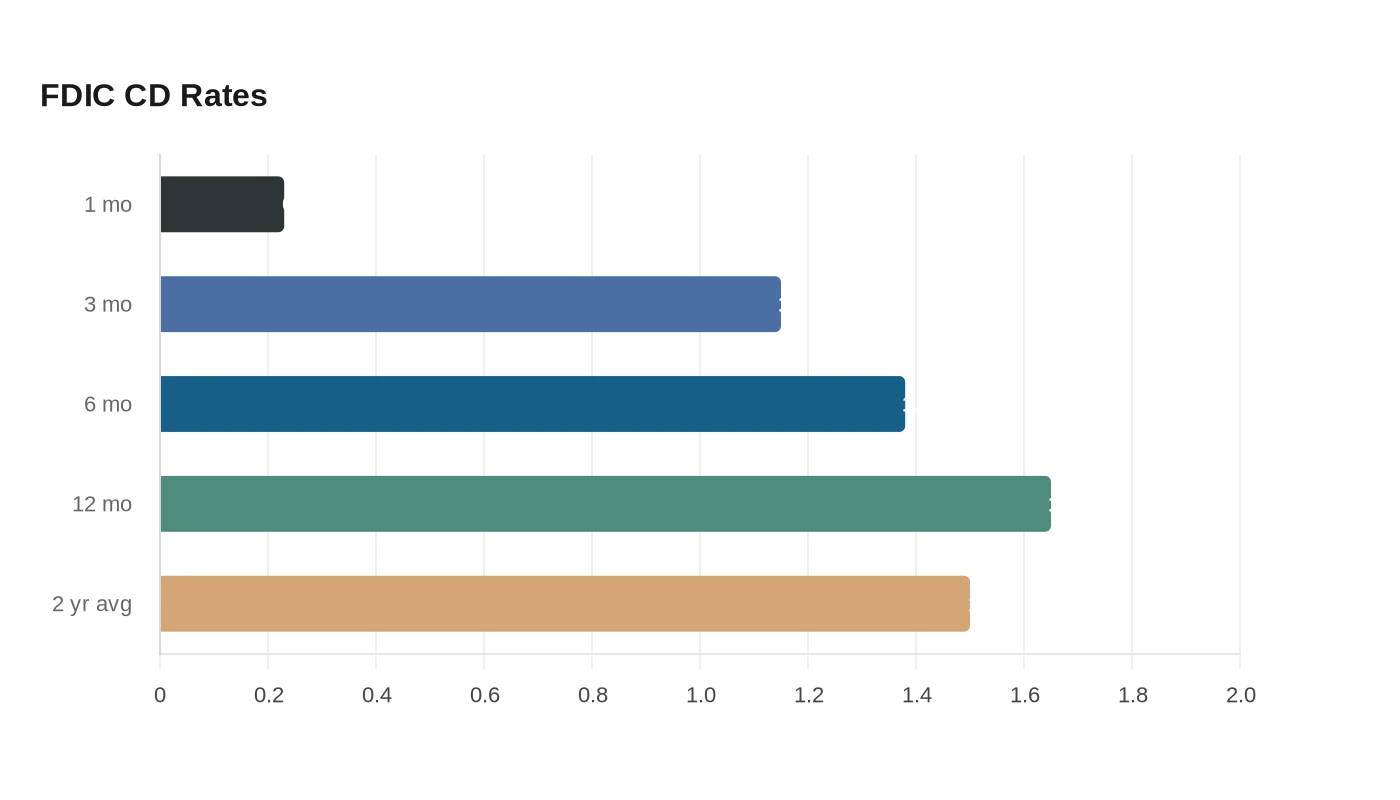

For context, the FDIC’s national CD rates on June 15 were 0.23% for a 1-month CD, 1.15% for a 3-month CD, 1.38% for a 6-month CD, and 1.65% for a 12-month CD. A June 2026 source tracking FDIC data puts the average 2-year CD rate at about 1.50%, which is far below the best advertised offers and is the reason shopping around still matters.

How CDs compare with the other cash parking spots

High-yield savings is the obvious liquidity rival. Bankrate says the top savings rate is 4.15% APY, while the national average savings yield is 0.61%, so the spread between the best online accounts and traditional savings remains huge. If a 4.15% account held steady for two years, $20,000 would grow to about $21,694 before tax and about $19,637 in today’s dollars after a 22% federal tax on interest and 4.2% inflation, which is slightly better than the top CD on this narrow math but without the lockup.

Treasurys offer a similar nominal yield with one important tax advantage. The Treasury curve showed a 2-year yield of 4.09%, and the IRS says Treasury bill, note, and bond interest is subject to federal tax but exempt from state and local income taxes. If that yield held for two years, $20,000 would become about $21,669 before tax and about $19,620 in today’s dollars after a 22% federal tax on the interest, and the state-tax exemption can make the after-tax result more attractive for investors in taxable accounts.

Money market funds can be easier to access, but the yield cushion is thinner. Morningstar shows Fidelity Government Money Market Fund with a 3.60% trailing 12-month yield, which would leave $20,000 at about $21,466 before tax and about $19,473 in inflation-adjusted buying power after a 22% federal tax on the interest. That is still a respectable parking place for cash, but it trails the best CDs and Treasury notes on this comparison.

What is driving the rate backdrop

The policy setting helps explain why these offers are still available. The Federal Reserve’s H.15 release showed the federal funds effective rate at 3.62% on June 8 to 12, 2026, which keeps short-term market yields elevated enough for banks to advertise 4%-plus CDs in some cases. At the same time, the Bureau of Labor Statistics said consumer prices were up 4.2% over the previous 12 months in May 2026, so a decent nominal yield still has to fight its way through a fairly strong inflation headwind.

That is why the lock-in question matters more than the headline APY. Bankrate says a CD lets savers lock in a fixed rate for a set period and earn guaranteed growth, which is useful if rates fall, but the tradeoff is clear if rates stay elevated or cash is needed early. A rate that looks strong on paper can still leave you underwater in real terms once tax, inflation, and liquidity are priced in.

For a two-year reserve you truly will not need, a top CD can still be a reasonable shelter against falling rates. For emergency cash, or money that might be needed before maturity, the combination of early withdrawal penalties and weak real returns makes the case for staying liquid much stronger.

Sources

- [1]cbsnews.com

- [2]fdic.gov

- [3]bankrate.com

- [4]ycharts.com

- [5]federalreserve.gov