Business

$35,000 in a money market account could earn more than $1,300 a year

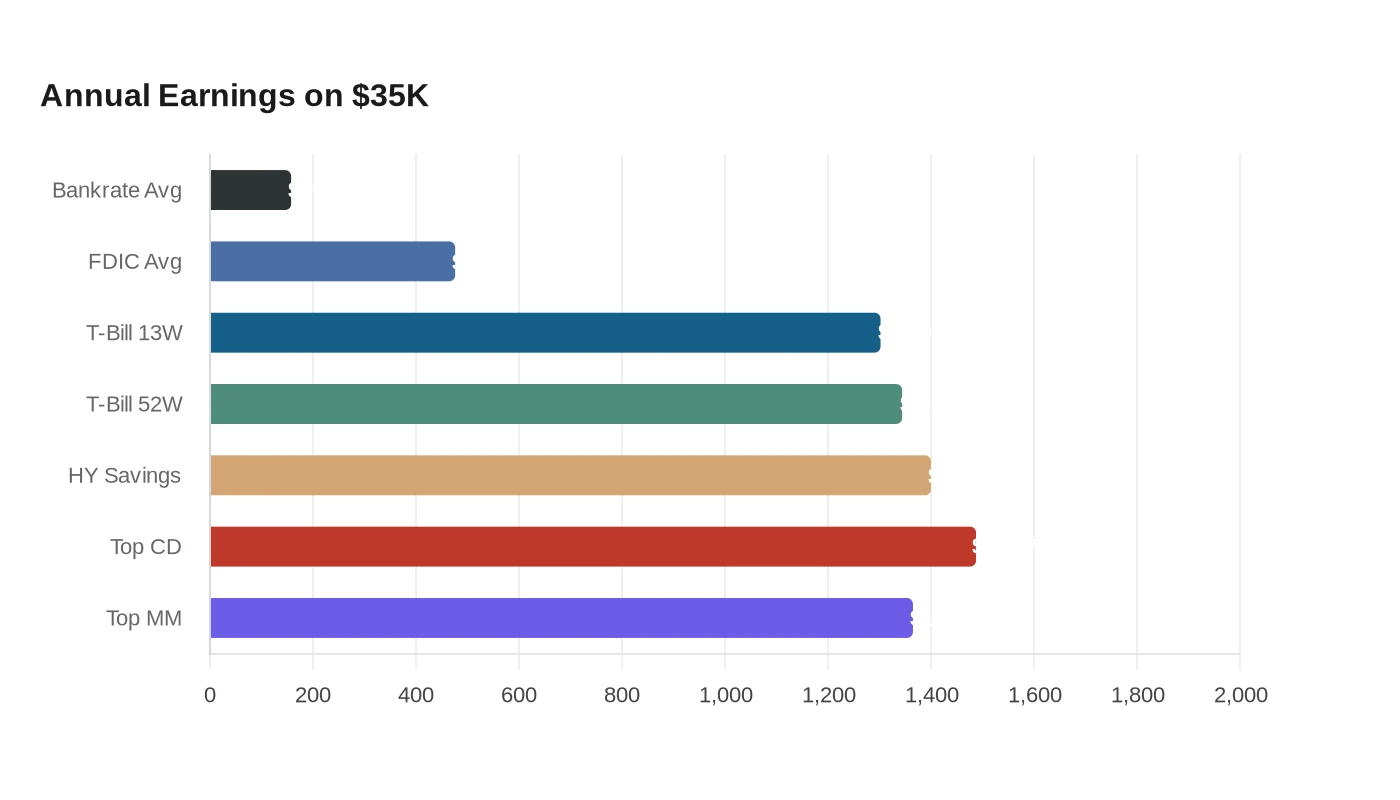

Money market accounts make the most sense for middle-class savers parking an emergency fund or home-down-payment cash who want insured liquidity, not the absolute highest yield. On a $35,000 balance, the payoff runs from about $157.50 a year at Bankrate’s 0.45% national average APY to about $1,365 at the current 3.90% top advertised rate.

The appeal is safety as much as yield. The Consumer Financial Protection Bureau says money market accounts are offered by banks and credit unions and are insured by the FDIC or NCUA up to $250,000 held by the same owner or owners. Bankrate also says these accounts often come with check-writing privileges and debit card access, which gives them more flexibility than many traditional savings accounts.

National pricing still shows a wide spread between average and best-in-market returns. The FDIC’s June 15 rate data puts the average money market rate at 1.36%, with a rate-cap adjusted ceiling of 4.37%. At that average, a $35,000 balance would earn about $476 in a year. The FDIC also says money market and certificate of deposit averages are based on the $10,000 and $100,000 product tiers, which helps explain why advertised online rates can look stronger than the national averages.

That gap matters when savers compare alternatives. Bankrate says the best high-yield savings accounts are paying around 4% APY, which would generate about $1,400 a year on $35,000. Bankrate’s top CD rates are around 4.25% APY, or about $1,487.50 a year, but CDs require locking up the money for a set term. Treasury bills offer another option: the Treasury’s June 15 daily rates showed a 13-week bill at 3.72% and a 52-week bill at 3.84%, equal to about $1,302 and $1,344 a year on $35,000.

Taxes can tilt the math. Treasury interest is subject to federal tax but exempt from state and local income taxes, a break that can matter in higher-tax states. Even so, the bigger challenge is inflation. Consumer prices rose 4.2% over the 12 months ended in May 2026, so even a 3.90% money market yield is still losing ground in real terms before taxes.

Bankrate expects savings and money market APYs to keep trending downward in 2026, which makes today’s rates worth watching closely. For cash that needs to stay safe, liquid and immediately available, a money market account still earns its place.

Sources

- [1]cbsnews.com

- [2]fdic.gov

- [3]bankrate.com

- [4]consumerfinance.gov