Business

740 credit score often needed for the best mortgage rates

Freddie Mac’s weekly survey put the national average 30-year fixed mortgage at 6.49% and the 15-year fixed at 5.82% for the week ending July 9, 2026. A 740 credit score is usually where mortgage pricing starts to improve in a noticeable way, but the cheapest loans often sit one tier higher, around 760 and above.

FICO says its scores are used by 90% of top U.S. lenders. The typical borrower is not far below the line, though: Experian put the average U.S. credit score at 713 in 2025, and FICO’s spring 2026 credit insights placed the national average at 714.

Where the rate break actually shows up

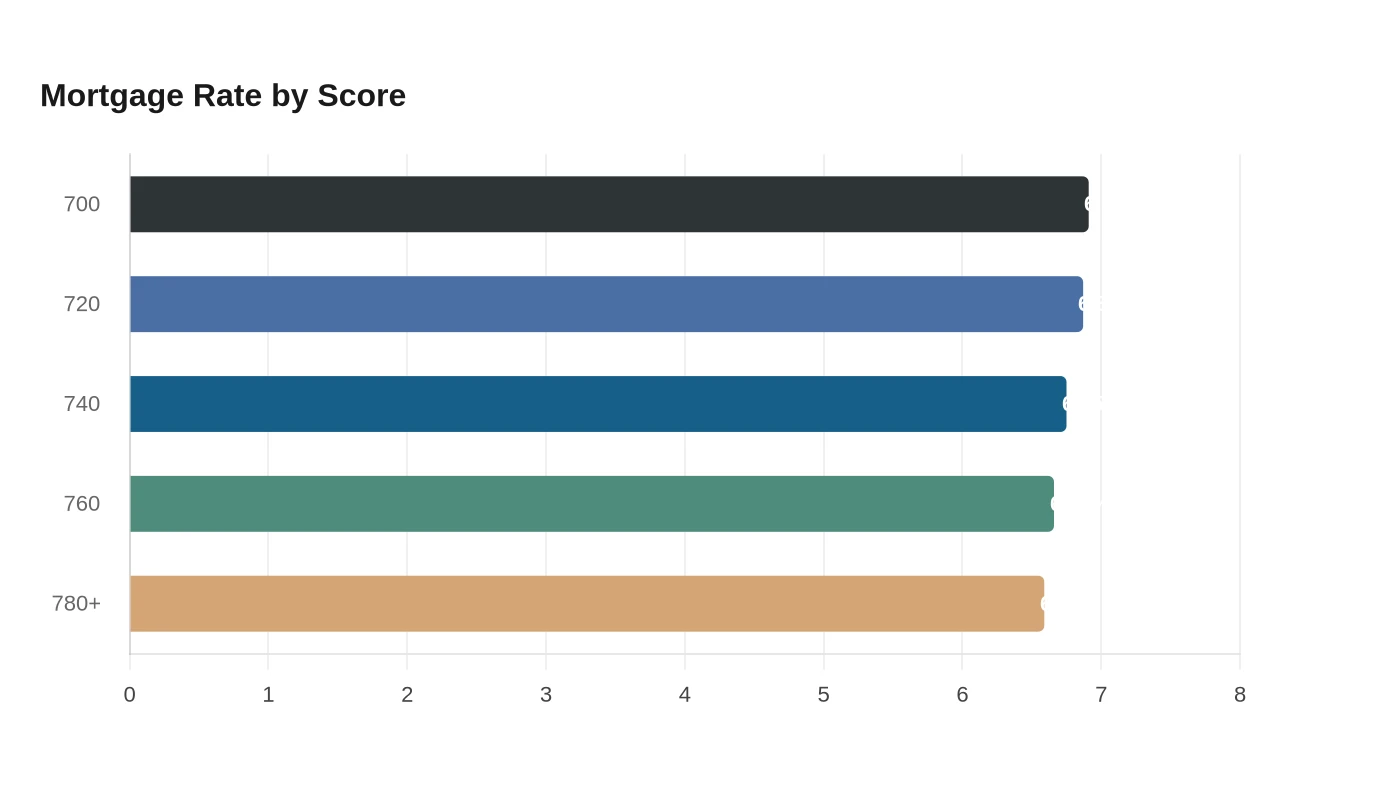

The most useful way to read mortgage pricing is by score band, not by the idea of a single perfect number. Experian published a July 2026 Curinos snapshot showing the 30-year conventional rate stepping down as the score rises: 700 at 6.91%, 720 at 6.87%, 740 at 6.75%, 760 at 6.66%, and 780 or higher at 6.59%, with the higher score tiers flattening out after that. The same table assumes a $350,000 mortgage and a 30-day rate lock.

On that $350,000 example, moving from 740 to 760 lowers the monthly payment by about $20.90 and cuts total interest by roughly $7,524 over 30 years. Moving from 740 to 780 lowers the monthly payment by about $37.10 and trims total interest by about $13,356.

For a more conventional tier view, broader market snapshots show the same pattern in broader bands: loans priced for borrowers with scores of 760 or higher are cheaper than loans for 700 to 759, which are cheaper than 680 to 699, and so on. On a $300,000 mortgage in one current snapshot, the 760-plus tier carried a 6.566% APR and $387,326 in total interest, while 700 to 759 carried a 6.846% APR and $407,393 in total interest, a gap of $20,067.

Why conventional loans price this way

Fannie Mae does not price a conventional mortgage on score alone. Its loan-level price adjustments are assessed using the representative credit score along with other loan features such as loan purpose, occupancy, number of units, product type and other eligibility inputs, and the current LLPA matrix on its site is effective beginning January 28, 2026. For pricing purposes on all loans, Fannie Mae uses the representative credit score, which is why a small move over a tier boundary can change the final rate sheet.

The Consumer Financial Protection Bureau advises borrowers to compare how changes in credit score, down payment, loan term and loan type affect both interest rate and total costs. The bureau’s examples assume a $400,000 primary residence purchase, 10% down, a 700 credit score, a conventional 30-year fixed loan, and a 60-day rate lock.

When lower scores can still get you to closing

Government-backed loans are more forgiving, but they are not free passes. Under HUD rules, FHA financing is not available if the Minimum Decision Credit Score is below 500, borrowers with scores from 500 to 579 are limited to 90% loan-to-value, and borrowers at 580 or higher are eligible for maximum financing.

VA-backed home loans are more flexible still. The Department of Veterans Affairs does not set a minimum credit score for VA loans, although lenders can impose their own credit standards, and VA guidance still requires satisfactory credit and income for the loan amount you want to borrow.

When to wait, and when to lock

The cleanest reason to wait is when you are sitting just below a pricing cliff. If a few weeks of balance paydown, a corrected reporting error, or simply time can move you from 740 to 760, the current market data suggest that small jump can save about $7,524 on a $350,000 loan, before considering any other fees or points. If you are already in the 780-plus band, the July 2026 snapshot shows no additional rate improvement above 780 through 840, so the payoff from chasing a few more points may be limited.

Locking sooner makes more sense when the score gain is uncertain or the market is moving against you. The 6.49% average for 30-year fixed loans is still high enough that a delay can erase the benefit of a modest score bump, and CFPB’s scenario tool is designed for exactly this kind of comparison.

Sources

- [1]cbsnews.com

- [2]freddiemac.com

- [3]consumerfinance.gov

- [4]fanniemae.com

- [5]selling-guide.fanniemae.com

- [6]answers.hud.gov

- [7]va.gov

- [8]myfico.com

- [9]experian.com