Business

Adobe raises revenue forecast on stronger AI tool adoption, subscriptions

Adobe raised its full-year revenue forecast on Thursday after stronger adoption of its AI tools and higher subscription spending lifted results beyond expectations. The bigger sales target gives investors a fresh test of whether generative AI can become durable recurring revenue, even as the company enters a period of leadership transition with chief financial officer Dan Durn set to depart.

The company now expects fiscal 2026 revenue of $26.5 billion to $26.6 billion, above its prior forecast of $25.9 billion to $26.1 billion. Adobe also lifted its third-quarter revenue target to $6.67 billion to $6.72 billion, signaling that demand carried into the new quarter.

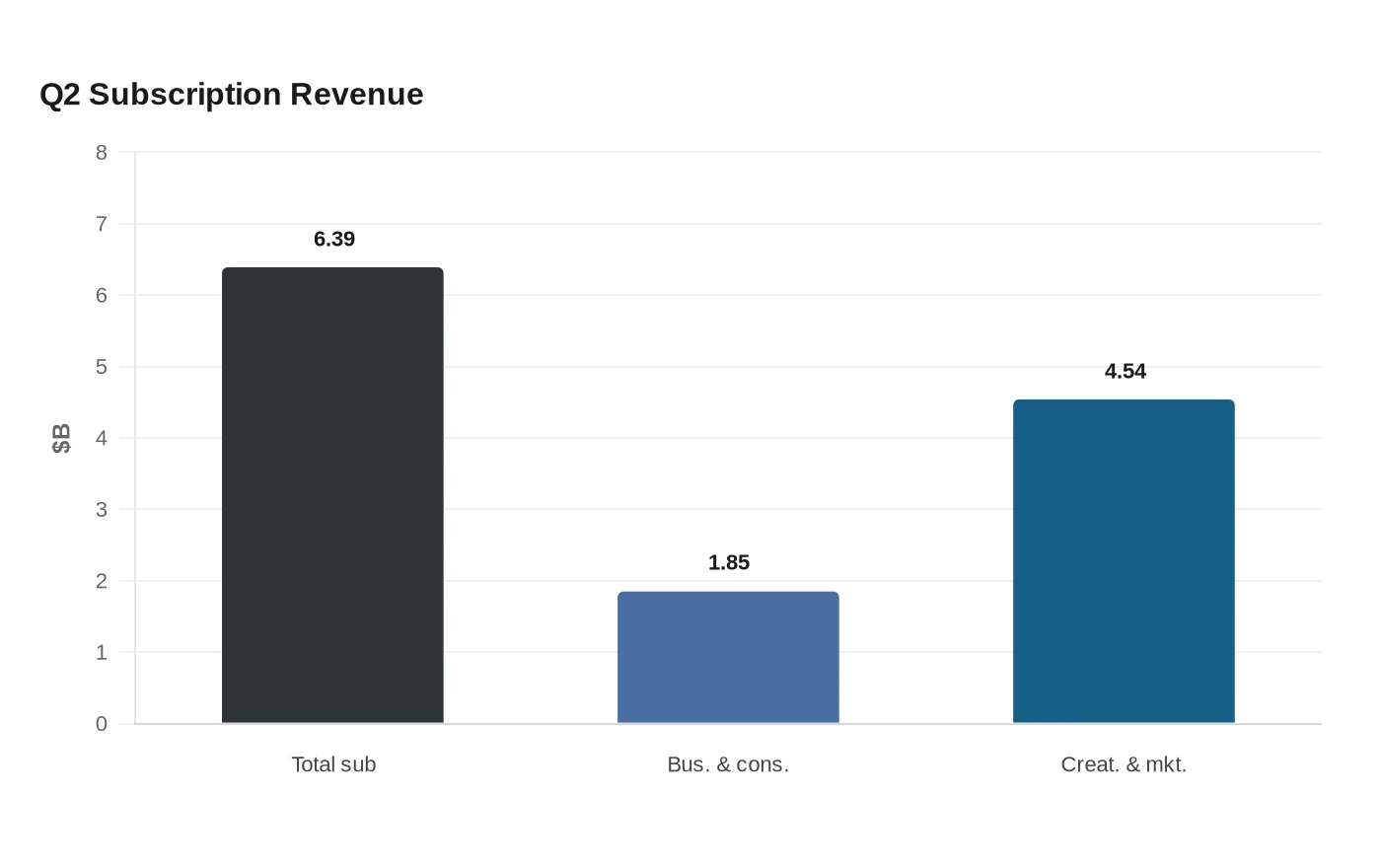

For the fiscal second quarter, Adobe reported record revenue of $6.62 billion, up 13% from a year earlier. Subscription revenue rose 14% to $6.39 billion, with Business Professionals & Consumers subscription revenue climbing 16% to $1.85 billion and Creative & Marketing Professionals subscription revenue increasing 13% to $4.54 billion. Those figures suggest Adobe is still converting product usage into paying customers at scale, rather than relying only on experimentation with new AI features.

A key metric for that shift was Adobe’s AI-first annualized recurring revenue, which tripled year over year and exceeded $500 million. Total annualized recurring revenue exiting the quarter reached $27.10 billion, including about $480 million from Semrush. Adobe completed its acquisition of Semrush on April 28, a move the company has said strengthens its ability to support discoverability and conversion in the AI era.

The earnings update lands at a sensitive moment for the company’s top ranks. Adobe said Durn will leave on June 15, and Steve Day, senior vice president of corporate finance, will serve as interim CFO. In March, Adobe also said chief executive Shantanu Narayen would transition out of the role after a successor is named, ending an 18-year run while he remains chair of the board.

That combination of stronger operating results and executive turnover leaves Adobe in a familiar but demanding position: it must prove that AI features can deepen its subscription model without disrupting it. For investors, the quarter offered evidence that adoption is accelerating. The larger question is whether that momentum can hold long enough to justify the company’s higher revenue target.

Sources

- [1]money.usnews.com

- [2]adobe.com

- [3]news.adobe.com