Business

Bailey defends Bank of England bond sales as crisis buffer

Andrew Bailey is defending the Bank of England’s gilt sales as a necessary reset, not a retreat, arguing that the central bank needs to preserve room to act when the next crisis hits. The stakes reach far beyond the Bank’s own balance sheet: the pace of quantitative tightening can affect government borrowing costs, mortgage pricing and how much firepower the Bank retains for the next emergency.

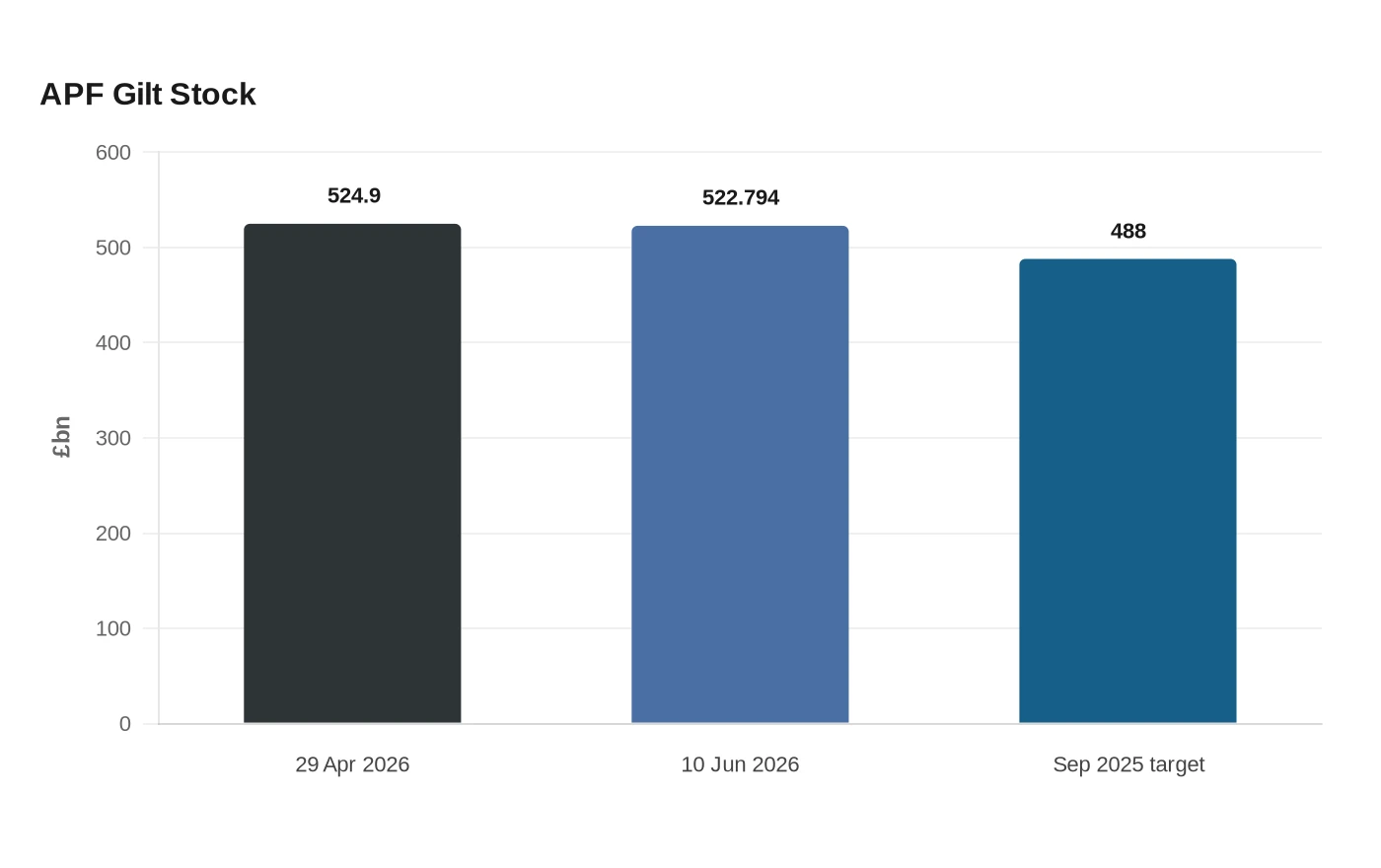

The Asset Purchase Facility still held £522.794 billion of gilts as of 10 June 2026, while HM Treasury said the stock was £524.9 billion on 29 April 2026. In September 2025, the Monetary Policy Committee voted 7-2 to reduce the gilt stock by £70 billion over the following 12 months, to £488 billion, after the Bank bought £875 billion of gilts between 2009 and 2021 to steady the economy through the financial crisis and the pandemic.

Bailey has cast that unwind as a normalization step. He has argued that quantitative easing was essential when support was needed, but that the policy should now be reversed as those emergencies fade. He has also pushed back against critics including Nigel Farage and Richard Tice, saying the financial impact is similar whether gilts are sold or simply held to maturity, and that the Bank’s broader mandate requires it to protect both monetary policy and financial stability. The Bank has said unwind should be gradual and predictable, with Bank Rate remaining the Monetary Policy Committee’s active policy tool.

That argument lands in a politically sensitive place because the costs of QT are not abstract. Reuters reported in August 2025 that quantitative tightening may have added as much as 0.25 percentage points to the cost of 10-year UK government borrowing, a real fiscal burden at a time when debt servicing already commands close scrutiny. The Asset Purchase Facility is indemnified by HM Treasury, so risks and future cash transfers can ultimately fall to the Exchequer, keeping ministers closely engaged in how fast the stock is wound down.

The Bank has already shown it is willing to adjust the process to limit market disruption. It slowed QT in September 2025 and shifted sales away from long-dated gilts, signaling that even a policy framed as normalization can tighten financial conditions if it is pushed too far. With the APF still composed solely of gilts and its stock updated through regular Treasury-Bank correspondence every six months, the debate now turns on whether the unwind is prudent balance-sheet repair or an active policy choice that risks squeezing the economy just as the Bank tries to keep its crisis buffer intact.