Business

BofA, Deutsche Bank now expect Fed rate hikes later this year

Bank of America and Deutsche Bank are challenging the market’s base case by saying the Federal Reserve may not be done tightening. Both firms now expect rate hikes later this year, a sharp shift from the view that the Fed would keep policy unchanged through the rest of 2026, as inflation stays sticky and the labor market remains firm.

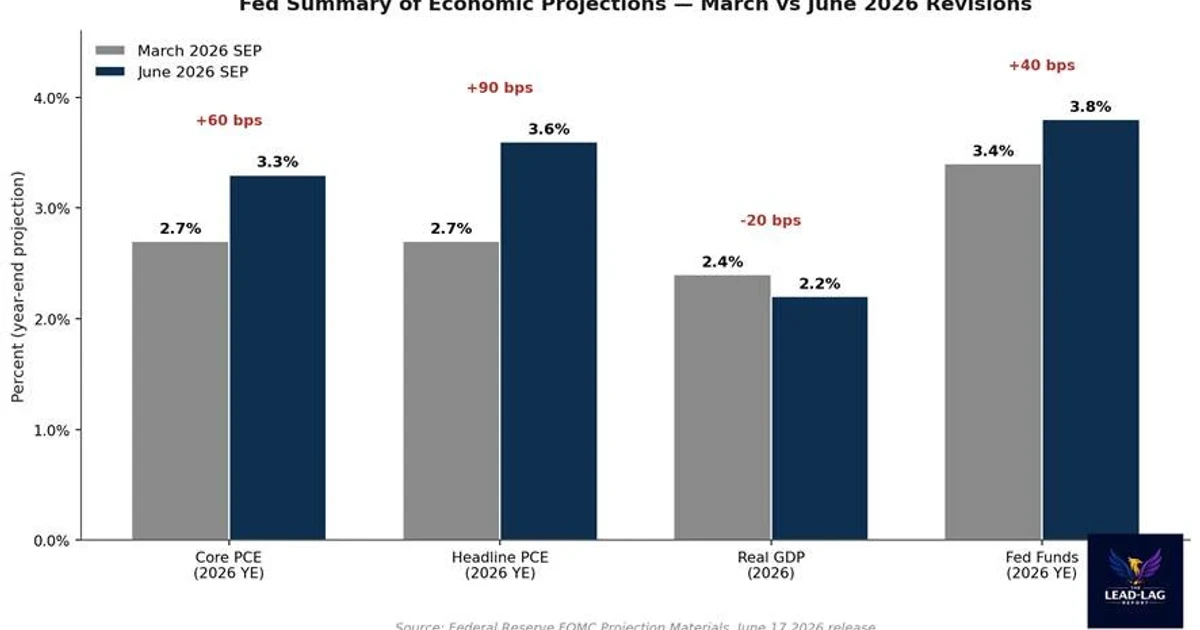

The move follows the Federal Open Market Committee’s June 16-17 meeting, when policymakers unanimously held the benchmark overnight borrowing rate in a 3.5% to 3.75% range and removed language that had pointed toward cuts. In the June 17 Summary of Economic Projections, the median year-end 2026 fed funds rate rose to 3.8% from 3.4% in March, with the median growth forecast at 2.2%, unemployment at 4.3% and PCE inflation at 3.0%. That combination signals a central bank still expecting positive growth, but not enough cooling in prices to be comfortable yet.

BofA now expects three quarter-point increases in September, October and December, for a total of 75 basis points. That is the most aggressive rate-hike call among the brokerages cited, and it reflects what BofA sees as a more hawkish reaction function under new Fed Chair Kevin Warsh. Deutsche Bank has also turned more hawkish, forecasting two 25-basis-point moves in September and December, or 50 basis points in total. Warsh did not submit a dot in the June projection grid, and after the meeting he said he was forming task forces to review major Fed operations and communications, including press conferences, dot plots, meetings, transcripts and minutes.

The banks’ shift lands against a market still leaning the other way. Nearly half of Fed policymakers now expect rates to rise this year, and markets were pricing roughly 41.2 to 42 basis points of hikes in 2026, below both Wall Street calls. BNP Paribas and Macquarie are also among the minority of brokerages expecting hikes, but most others still see no change for the rest of the year.

For households and companies, the consequence is straightforward: mortgage costs, credit-card rates and business borrowing could stay elevated, or even rise again, longer than many investors had assumed. That would keep pressure on floating-rate loans, corporate refinancing and consumer debt service just as policymakers are signaling they may be more willing to defend price stability than to cushion growth.

Sources

- [1]finance.yahoo.com

- [2]kitco.com

- [3]cnbc.com

- [4]federalreserve.gov

- [5]usnews.com