Business

Canada's economy stalls as tariffs and weak growth weigh on outlook

Canada’s economy is barely moving: real GDP was unchanged in the first quarter of 2026 after a 0.2% decline in the previous quarter, while per-capita GDP rose 0.2% only because the population fell for a second consecutive quarter. May brought an 88,000-job rebound and pushed unemployment down to 6.6%, but that followed a net loss of 112,000 jobs in the first four months of the year. The result is an economy that looks steadier in the monthly labour data than it feels in households’ budgets, and one still caught between a tariff shock and a deeper question about its long-run growth path.

The flat quarter hides a fragile mix

The first-quarter GDP number was not held back by one simple weak spot. Higher imports, especially gold, were offset by inventories, while lower business and government capital investment was balanced only partly by stronger household spending, leaving final domestic demand 0.1% lower. That is a narrow base for growth, and it helps explain why Canada’s 1.7% real GDP gain in 2025, already the slowest annual pace since 2020, has not translated into a convincing upswing in 2026.

The labour market has been equally uneven. Statistics Canada’s May survey showed the first significant employment gain since November 2025, but it came after a prolonged stretch of weakness, including a net decline of 112,000 jobs from January through April. A 6.6% unemployment rate is still far from crisis levels, yet it is high enough to tell you that firms have not fully regained confidence and that the economy is running with visible slack.

Why households feel the slowdown more sharply than the headline data suggest

The OECD’s 2025 survey of Canada says the country’s macroeconomic framework remains robust, supported by strong public finances and a well-capitalised banking sector, but it also flags the pressures that land directly on households: tariffs with the United States, high household mortgage debt, high debt-service costs and declining housing affordability. That combination matters because it means an average family can face tighter finances even when the national accounts look merely flat rather than clearly negative.

The deeper concern is that Canada’s soft patch is landing on top of a long-running productivity problem. OECD material has warned that years of weak investment and tepid productivity growth have to be reversed if Canada is going to improve living standards, and its newer work still points to housing affordability and trade resilience as key vulnerabilities. The per-capita GDP uptick in the first quarter was therefore less a sign of strength than a reminder that output is not keeping pace with the pressures households face.

Tariffs are the immediate drag

The Bank of Canada said in its April 29 outlook that US tariffs and uncertainty around the Canada-United States-Mexico Agreement are the main factors shaping the outlook. It expects current US tariffs to remain in place and have a persistent negative effect on activity, while inflation is projected to rise in the near term before easing toward 2% in early 2027. That is the clearest official signal yet that the central bank sees this as more than a temporary trade wobble.

The Bank’s message is important because it connects trade policy to the real economy rather than treating tariffs as a narrow export issue. If tariffs stay, the economy does not simply lose a few shipments to the United States; it also loses investment, clarity and the confidence firms need to hire and expand. That is why the current slowdown has a policy dimension that reaches beyond the usual business-cycle debate.

Forecasts are moving lower, not higher

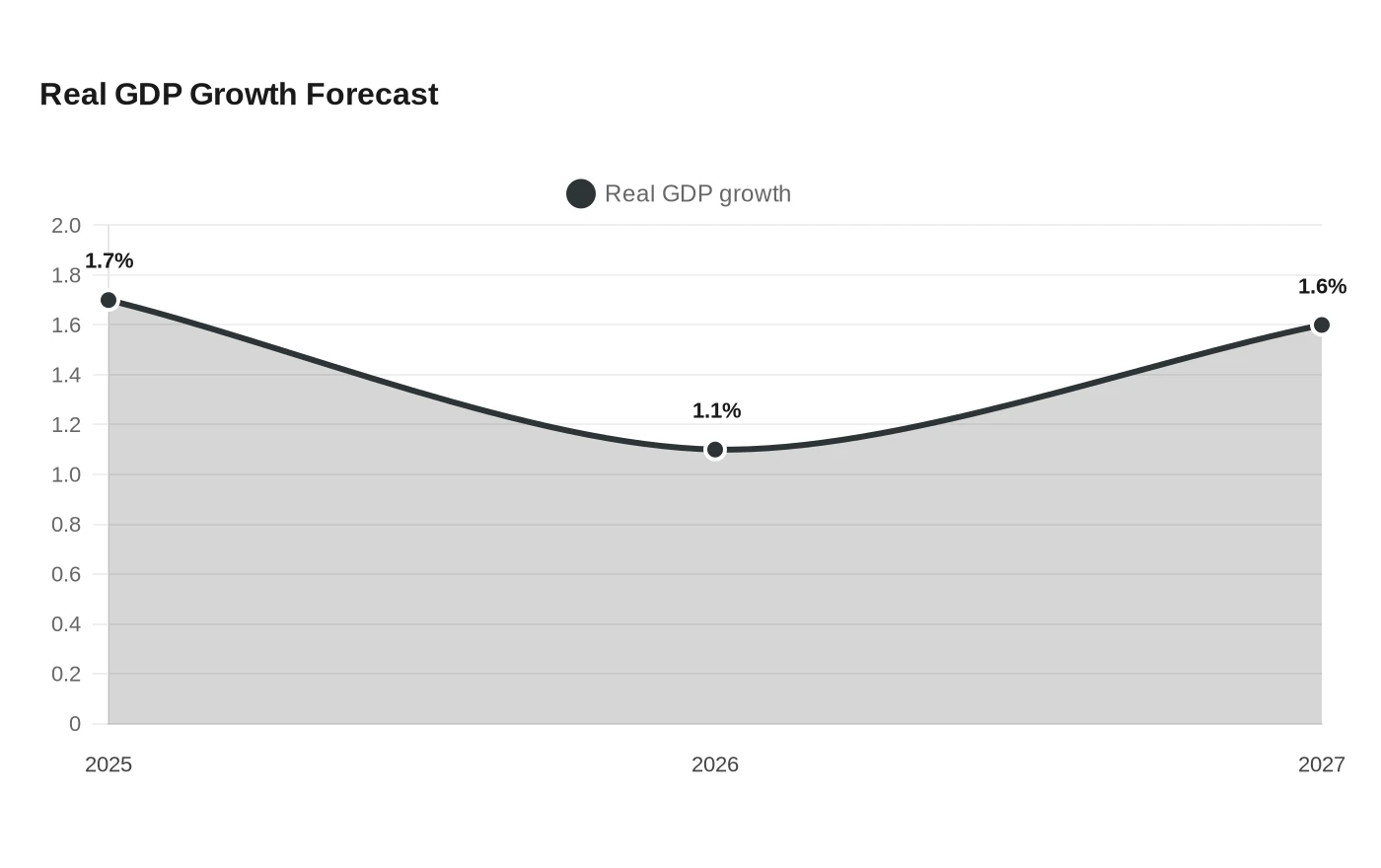

The Parliamentary Budget Officer’s June 2026 outlook says Canada grew 1.7% in 2025, then projects real GDP growth of 1.1% in 2026 and 1.6% in 2027 if the tariff environment is treated as permanent. National Bank of Canada has become more cautious still, cutting its 2026 growth forecast to 0.7% after the weak first-quarter GDP reading and continued trade uncertainty. Taken together, those forecasts point to a country that is still growing, but at a pace that is too soft to ease pressure on incomes, investment or housing costs.

That widening gap between the better months and the weaker outlook is what makes the current moment hard to read. A quick rebound in hiring can coexist with a weaker growth trend if firms remain cautious and households continue to carry heavy mortgage burdens. In that sense, Canada is not facing an all-or-nothing choice between recession and expansion; it is confronting the possibility of persistently low-speed growth.

How Canada compares with peers

The federal Spring Economic Update 2026 says Canada is expected to have the second-fastest real GDP growth in the G7 in the IMF’s April 2026 outlook, and it notes that Canada has added nearly three times as many jobs per capita as the United States since the start of 2025, 3.4 per 1,000 people versus 1.2. Those numbers matter because they show Canada is not lagging every peer on every measure. But they also show how selective the good news is: the labour market can look resilient while living standards still feel pinched.

That is the core tension in Canada’s outlook. On the surface, growth is still positive, unemployment is not surging and Canada remains ahead of some peers on near-term expansion. Underneath, productivity remains weak, housing is expensive, household debt is heavy and tariffs threaten to keep business investment subdued. The best reading of the data is that Canada is experiencing a painful squeeze now, but the reason households feel it so sharply is that the economy was already vulnerable before the tariffs arrived.

Sources

- [1]bbc.co.uk

- [2]www150.statcan.gc.ca

- [3]bankofcanada.ca

- [4]oecd.org

- [5]pbo-dpb.ca

- [6]nbc.ca

- [7]budget.canada.ca