Business

CD rates near 4% could boost returns on $30,000 deposits

A $30,000 CD opened in July at 4.10% APY would earn about $1,230 in a year before taxes, while the 1.65% national average for one-year CDs would pay only about $495.

Where CD rates sit now

The best one-year CDs are still paying more than double the national average, and the strongest rates remain clustered around 4%. NerdWallet's best one-year CD rate is 4.10% APY, its highest tracked overall CD rate is 4.30% APY on a 17-month CD from Connexus Credit Union, and Bankrate's top tracked rate is 7.50% APY from SF Fire Credit Union even though the broader market is still around 4%.

The Federal Open Market Committee kept the federal funds target range at 3.5% to 3.75% on June 17, and its next scheduled meeting is July 28-29. CD rates have generally been trending down in 2026, although some online banks have lifted competitive short-term offers since late March.

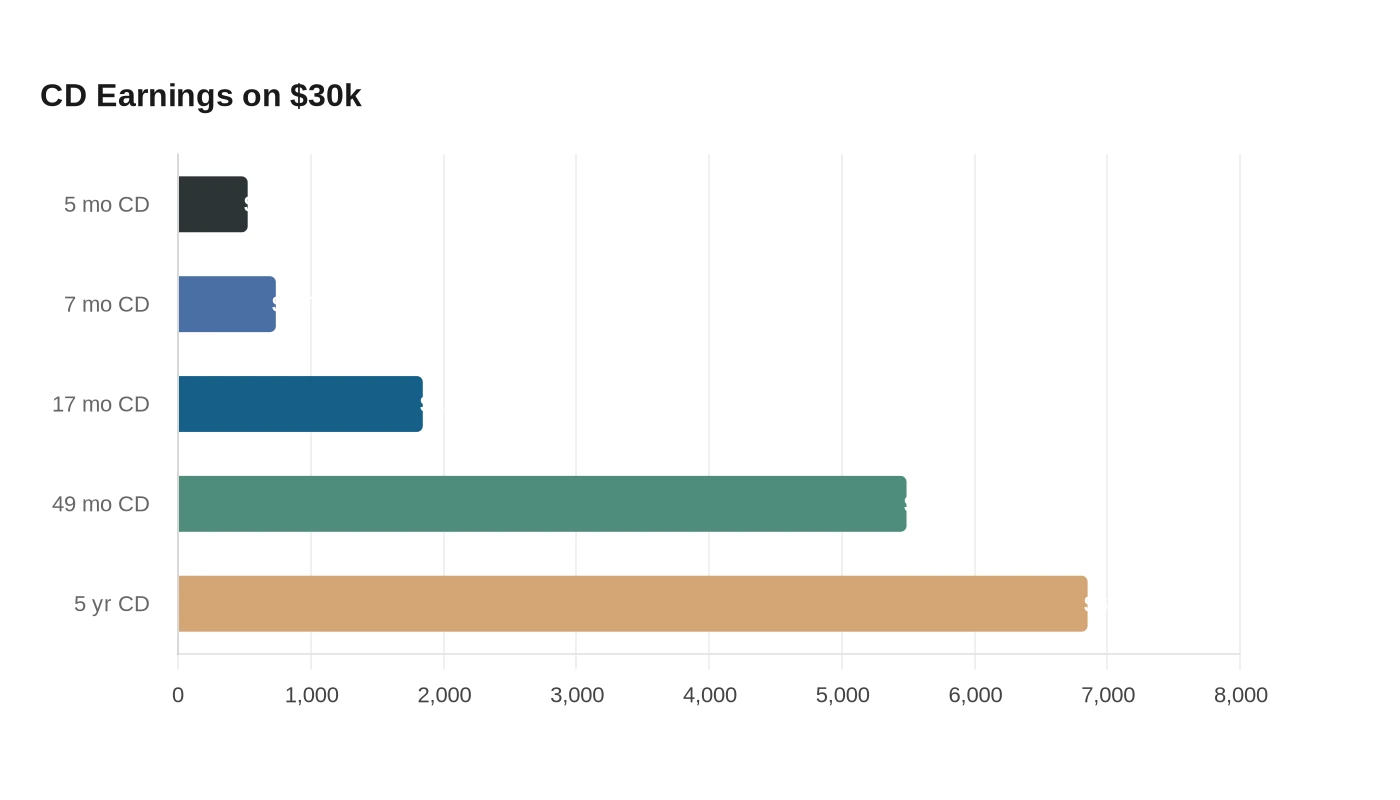

What $30,000 earns across common terms

On a $30,000 balance, the math changes with the term. A 5-month or 7-month CD at 4.25% APY would generate about $525 and $737 respectively, and the 17-month leader at 4.30% APY would return about $1,844 over the full term. Longer maturities compound the cash return further, with a 49-month CD at 4.20% APY producing about $5,488 and a 5-year CD at 4.20% APY producing about $6,852 if held to maturity.

APY is annualized, so the longer CDs do not pay dramatically different rates, they simply let the deposit compound for more months.

Taxes, inflation and the cost of breaking the term

Taxes trim those gains quickly. Using a 24% federal bracket as a simple benchmark, the $1,230 earned by a 4.10% one-year CD falls to about $934.80 after tax, the $1,245 from a 4.15% high-yield savings account falls to about $946.20, and the $1,212 from a 4.04% one-year Treasury constant maturity falls to about $921.12. On a $30,000 balance, the yield gap between the best savings account and the best one-year CD is only $15 before tax, or about $11.40 after federal tax.

Inflation makes the picture harder. The Bureau of Labor Statistics put consumer prices 4.2% higher over the 12 months ending in May 2026, which means a 4.10% CD does not fully keep pace even before tax. Using that inflation rate and the same 24% bracket, the CD still leaves about $312 in lost purchasing power on a $30,000 balance over a year, while the top high-yield savings account narrows that loss to about $301 and the one-year Treasury sits around $325 before accounting for state-tax savings.

Early withdrawals are the biggest trap. In Bankrate's survey, CD penalties typically run from 60 to 365 days of interest, and a three-month interest penalty on a $30,000 CD at 4.10% APY works out to about $307.50, roughly a quarter of the year’s gross return. A six-month penalty would be about $615, which is large enough to erase most of the advantage of locking the money in the first place.

How CDs compare with high-yield savings and Treasurys

High-yield savings accounts remain the closest substitute when liquidity matters. Bankrate’s top savings rate is 4.15% APY, and its national average is still just 0.62% APY, so online savings accounts are paying far more than traditional accounts while still allowing easy access to cash for emergencies or near-term spending.

Treasurys offer a different trade-off. The Federal Reserve’s 1-year constant maturity rate is 4.04%, a little below the best one-year CD, but Treasury interest is subject to federal tax while being exempt from state and local taxes. That exemption can make Treasurys more attractive for savers in states with income tax, especially when the headline yields are this close.

When locking cash makes sense

A CD makes the most sense when the money can stay untouched through the full term and you want the certainty of a fixed rate. CDs lock in a fixed rate for a set period, which matters when the Fed is holding rates steady and deposit yields can soften if banks decide they no longer need to pay as much for cash. With the Fed’s next meeting set for July 28-29, a saver opening a CD this month is really deciding whether to freeze today’s rate before the next policy move resets the market’s expectations.

The best move depends on the cash’s job. If the money is part of an emergency reserve or could be needed before maturity, the almost-identical yield on a top savings account is hard to ignore. If the money is truly idle, the combination of a 4% handle on APY, a known maturity date and the possibility of preserving that rate if yields slide lower later in the year can justify locking it up.

Sources

- [1]cbsnews.com

- [2]nerdwallet.com

- [3]bankrate.com

- [4]federalreserve.gov