Business

China emerges as the new power setting global oil prices

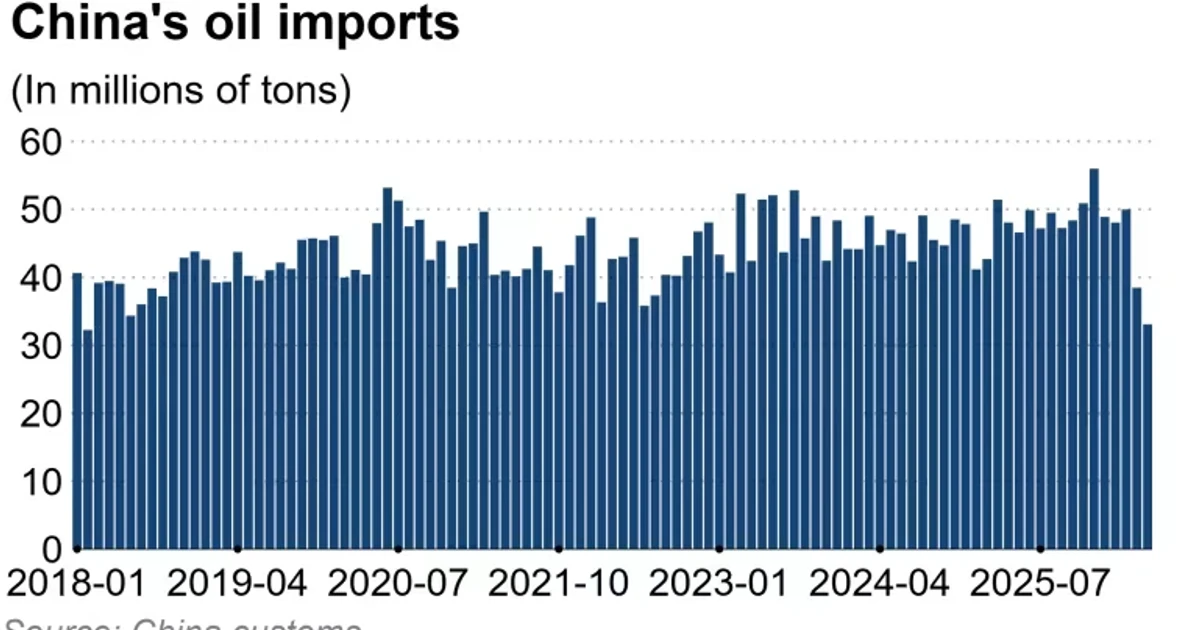

China has moved from being the world’s biggest oil buyer to being one of the market’s decisive price setters. The shift is not just about how much crude it imports, but whether that oil is burned in refineries or parked in storage, a choice that can tighten supply or absorb it before it reaches the open market. That gives Beijing a lever that now matters alongside, and sometimes more than, OPEC’s production decisions.

China’s reserves now rival the old price setters

The U.S. Energy Information Administration estimated that China added an average of 1.1 million barrels a day to strategic oil inventories in 2025, pushing those stocks to nearly 1.4 billion barrels by December 2025. That is far larger than the U.S. Strategic Petroleum Reserve, which held about 413 million barrels in December 2025 and roughly 409 million barrels on April 10, 2026. The comparison captures the scale of China’s market influence: it has built a stockpile large enough to shape pricing even without publicly disclosing official reserve levels.

Because Beijing does not release a full inventory tally, traders and analysts infer the size of its strategic reserves from import flows, refinery throughput and storage construction. That opacity itself matters. When a buyer that large can shift barrels between consumption and storage without a public target, it becomes harder for the market to guess when extra demand is temporary restocking and when it is a lasting change in balance.

How Beijing can create a floor or a ceiling

China’s leverage works in both directions. When prices fall, it can buy aggressively and move crude into storage, absorbing supply and helping create a price floor. When prices rise, it can slow imports, lean on existing inventories and allow refiners to run without immediately chasing additional barrels, which can cap rallies and create a ceiling.

That is why Chinese demand has become so important during supply shocks. During the recent Iran-related disruption, China was able to cut imports sharply without drawing down reserves, which helped soften the kind of price spike that usually follows geopolitical stress. In practical terms, that means a disruption no longer translates as cleanly into a one-way price jump, because the market now has to factor in whether China will buy, stockpile or stand aside.

The effect also reaches the U.S. economy. Crude oil is the feedstock for gasoline and diesel, so a Chinese decision to soak up barrels can tighten global supply, raise refined-product costs and show up in American pump prices. When fuel costs rise, they feed directly into inflation measures through transportation and shipping, which is one reason Beijing’s storage policy matters well beyond Asia.

OPEC+ still moves the market, but it no longer moves it alone

OPEC’s traditional power came from adjusting output. That is still true, but the group is operating in a market where China’s demand side can offset or reinforce those moves. Reuters reported that OPEC+ delayed the start of oil output increases until April 2025 and pushed the full unwinding of cuts to the end of 2026, a sign that the group was trying to avoid flooding the market too quickly.

On March 1, 2026, eight OPEC+ members met virtually and said they would adjust output again while citing market stability and low inventories. That language shows the coalition is still focused on managing expectations, but the backdrop is different now. If China is stockpiling, OPEC+ can ease prices only so far before Beijing’s buying absorbs the extra supply. If China pulls back, even restrained OPEC+ production can feel ample.

The result is a subtler balance of power. OPEC+ still shapes supply, but China increasingly determines how much of that supply becomes visible to the market. In a world where the biggest importer can behave like both a consumer and a strategic reserve manager, the old producer-led model no longer explains price movements on its own.

What the latest buying pattern says about demand

China’s crude demand has also shown that it is highly responsive to price. In June 2025, it imported 12.14 million barrels a day, with volumes rising from Saudi Arabia and Iran. Traders linked that increase to lower prices and restocking after refinery maintenance, which is the kind of buying behavior that reinforces the idea of China as a swing buyer rather than a steady, passive importer.

That pattern matters because it blurs the line between commercial demand and policy-driven stockpiling. When imports rise because refiners need feedstock, the market reads it one way. When imports rise because strategic inventories are being built, the market reads it another. In both cases, though, China is taking barrels off the spot market and supporting prices.

The same logic appears in the latest trade flows. Reuters reported on July 10, 2026 that Iranian oil supplies at sea were rising after Tehran ramped up exports during the interim peace deal with the United States, while China’s teapot refiners were turning toward rival Middle East supplies. That suggests Chinese buyers are still choosing among producers rather than simply absorbing whatever arrives, which keeps competition among exporters alive even when geopolitical tensions are high.

Why the next leg of the market still runs through China

Bloomberg reported on July 13, 2026 that China’s crude imports were expected to recover as stockpiling returned later in 2026, with analysts and traders anticipating another build in strategic inventories. If that happens, the market will again have to price a large, strategic buyer whose decisions can either tighten the balance or soften a shock.

For producers, that means leverage is no longer concentrated only in Vienna or in OPEC+ meetings. For consumers, especially in the United States, the consequence is that gasoline prices and inflation are now exposed to decisions made in Beijing as much as to production targets set by oil exporters. China’s stockpiling has become a global macroeconomic variable, and it is now one of the clearest forces defining where oil prices stop falling and where they stop rising.

Sources

- [1]nytimes.com

- [2]eia.gov

- [3]finance.yahoo.com

- [4]opec.org

- [5]iranintl.com

- [6]worldenergynews.com

- [7]msn.com

- [8]bloomberg.com