US News

Eliminate payroll tax cap to help shore up Social Security

Social Security’s financing problem is not abstract, and it is not just about insolvency. The real choice is who pays to keep the system whole: workers above the wage cap and their employers, everyone on the payroll tax base, or future retirees through lower benefits. Under the 2024 Trustees Report, the combined trust funds were projected to be depleted in 2035, and the program’s cost was already running above total income from 2024 onward.

What the cap does now

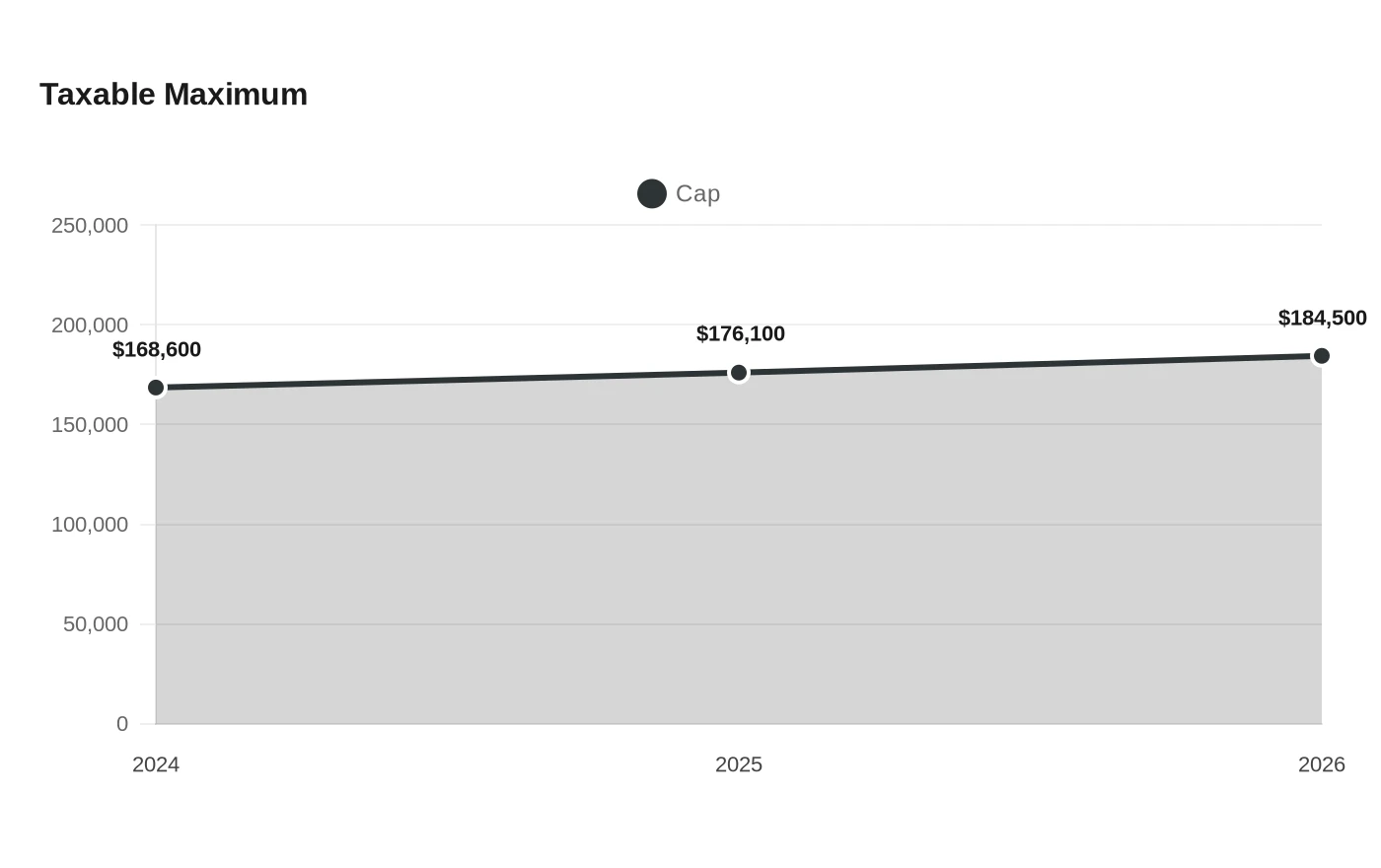

Social Security is financed through a dedicated payroll tax. Under current law, employees and employers each pay 6.2 percent of covered wages up to the taxable maximum, while self-employed workers pay 12.4 percent. In 2024, that maximum was $168,600; it rose to $176,100 in 2025 and is $184,500 in 2026, with the annual limit adjusted each year based on average wage growth. Earnings above that cap are neither taxed for Social Security nor counted in the benefit formula.

That structure matters because the cap is not a fixed ceiling in practice. It moves up each year, and it has done so for decades as Social Security, enacted in 1935, has been amended many times. Any proposal to remove the cap would therefore be a deliberate shift in policy, not a tweak to a frozen threshold.

How much eliminating the cap would raise

The Social Security Administration’s chief actuary has modeled a straightforward version of the idea: eliminate the taxable maximum beginning in 2025, apply the full 12.4 percent payroll tax to all earnings, and give no extra benefit credit for wages above the current-law cap. Under the 2024 Trustees Report assumptions, that policy would improve the long-range actuarial balance by 2.55 percent of taxable payroll and improve the 75th-year balance by 2.60 percent of payroll. Put differently, it would close about 73 percent of the 75-year funding gap and 56 percent of the shortfall in the program’s 75th year.

That is a large amount of revenue, but it is not a complete fix. The 2024 Trustees Report put the long-range shortfall at 3.50 percent of payroll and the annual 75th-year gap at 4.64 percent. So a full elimination of the cap would do most, but not all, of the work needed to restore solvency under those assumptions.

Who would pay more

The burden of eliminating the cap would fall squarely on people with wages above the taxable maximum, plus their employers. A worker earning at or above the 2026 cap would pay up to $11,439 in Social Security tax, and the employer would match that amount. Self-employed workers with earnings above the cap would owe the full 12.4 percent on those additional dollars.

This is why the cap debate is really a distributional debate. The Social Security Administration’s own population profile says almost 20 percent of current and future covered workers are projected to have earnings above the taxable maximum in at least one year, but the heaviest burden would still land on the highest earners and the businesses that employ them. Because the no-benefit-credit version of cap elimination taxes those extra wages without boosting future benefits on them, it functions more like a targeted tax increase on high-income labor than a new promise of higher retirement checks.

How it compares with other fixes

The cap is only one way to close the gap. A broad payroll-tax increase would spread the cost more evenly across every paycheck, and the chief actuary estimates that raising the payroll tax rate from 12.4 percent to 16.0 percent in 2025 and later would eliminate 100 percent of the long-range shortfall. That option is cleaner mathematically, but it would ask every covered worker and employer to pay more, not just those above the cap.

Benefit cuts are the other side of the ledger. If Congress did nothing, the 2024 Trustees Report said the combined trust funds would be depleted in 2035, after which continuing income would cover about 83 percent of scheduled benefits. That implies an across-the-board cut of roughly 17 percent, a result that would hit retirees, disabled workers and survivors alike.

Retirement-age changes are often marketed as a gentler fix, but the numbers show they still shift costs onto workers by cutting lifetime benefits. One SSA option, increasing the normal retirement age from age 67 to 68 for people age 62 starting in 2025, would eliminate only 12 percent of the long-range shortfall. A more aggressive option that lifts the normal retirement age to 69 would do more, but even that SSA estimate closes 47 percent of the long-range gap, still short of a complete solution.

Why the cap remains central to the debate

AARP has described eliminating or raising the wage cap as a commonly discussed solution, and that framing captures the basic policy trade-off. Because the cap already rises with wage growth, lifting or removing it would not be a one-time patch. It would permanently change who finances the program, pushing more of the repair bill onto top earners while preserving the basic benefit structure for everyone else.

That is why the cap fight keeps returning to center stage. Social Security has survived repeated amendments since 1935, but the financing math is now forcing Congress to choose between higher taxes on the most affluent workers, broader taxes on everyone, or lower benefits for future retirees. Eliminating the payroll tax cap would not solve the whole problem, but it would make the cost of doing so visibly more progressive.

Sources

- [1]nytimes.com

- [2]ssa.gov

- [3]crsreports.congress.gov

- [4]aarp.org