Business

Fed holds rates steady, but some borrowing options are cheaper

The Fed left rates unchanged again, but borrowers still have a few ways to borrow for less than the market’s headline pain suggests. On June 17, the Federal Open Market Committee voted 12-0 to keep the federal funds target range at 3.50% to 3.75%, its fourth straight meeting without a change, even as officials shifted their year-end rate outlook higher and stripped out language that had hinted at future cuts.

That matters because the cheapest money is still not cheap. Federal Reserve consumer credit data show credit-card APRs remain in the low-20% range, a level that keeps revolving balances expensive even after months of unchanged policy. LendingTree says debt consolidation accounted for 31.3% of personal-loan inquiries, a sign that many borrowers are still trying to refinance costly card debt into something more manageable.

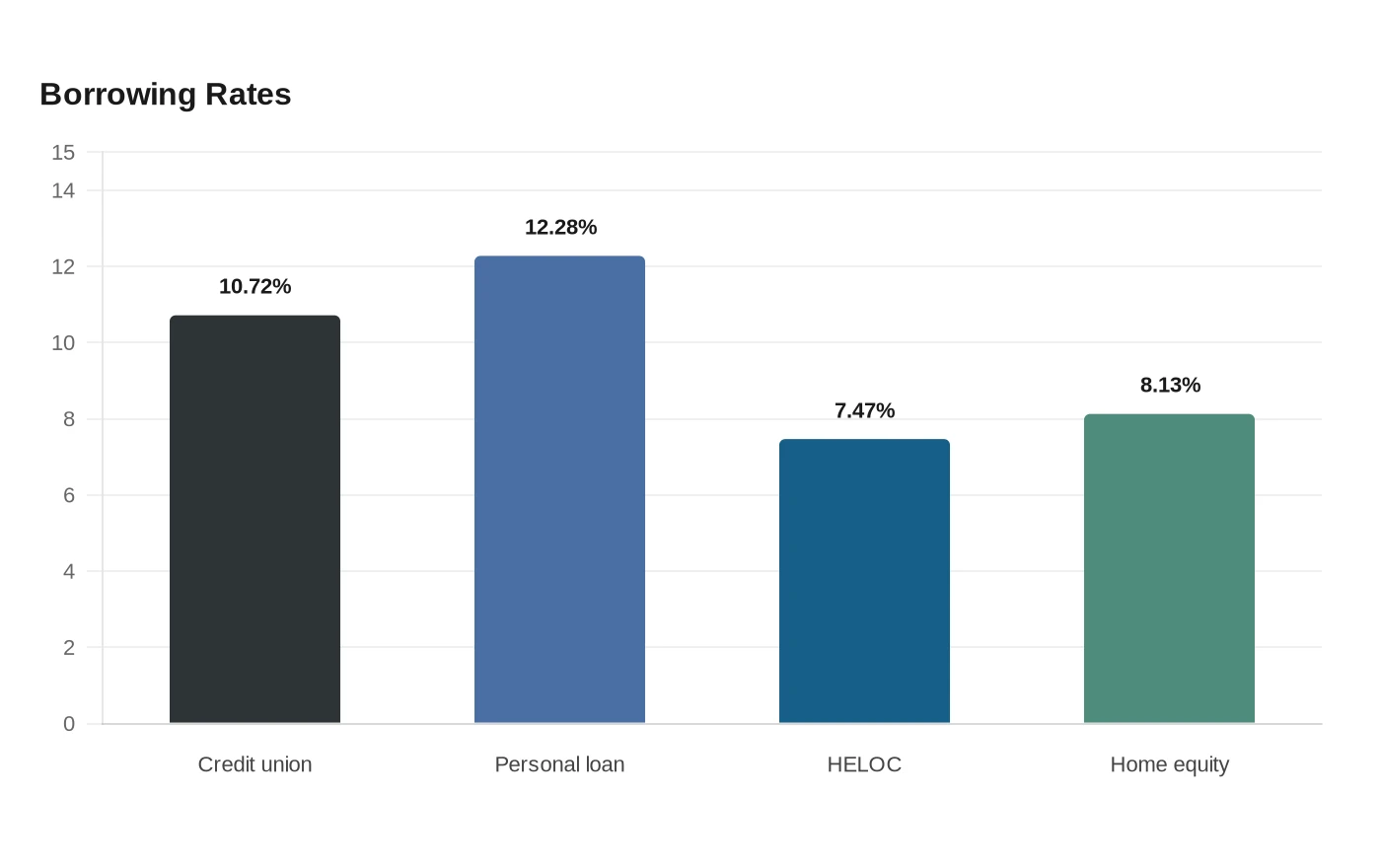

For shoppers comparing borrowing options, the first lane is a credit-union personal loan. Bankrate said the national average rate on a three-year personal loan at a credit union was 10.72% in the third quarter of 2025, below the broader personal-loan average. Some of the lowest advertised rates are reserved for highly qualified borrowers, including promotional credit-union offers in Virginia that started around 3.99% to 5.15%, but those deals are typically limited to applicants with strong credit and clean borrowing profiles.

The second lane is a standard unsecured personal loan from a competitive online lender. Bankrate put the average personal-loan rate in June at 12.28% for a borrower with a 700 FICO score taking out $5,000 over three years, while borrowers with excellent credit could see rates as low as 6.20%. That is still materially cheaper than card debt, but the gap narrows fast once credit weakens or the borrower needs a larger loan.

The third lane is home-equity borrowing for owners who have built up value in their homes. Bankrate said the national average HELOC rate was 7.47% on June 17, while the average home-equity loan rate was 8.13%. Those rates make home-equity borrowing one of the least expensive options available, and home-equity loans offer fixed payments, but the trade-off is stark: the home secures the debt.

The Fed’s latest pause suggests the high-rate era is not ending quickly, and its more hawkish projections point to less room for relief later in the year. For borrowers, that leaves a clear hierarchy: credit unions first, competitive personal loans next, and home equity last, only when the lower rate is worth the collateral risk.

Sources

- [1]cbsnews.com

- [2]federalreserve.gov

- [3]bankrate.com

- [4]lendingtree.com

- [5]monitorbankrates.com