Business

Fed leaders split over whether higher rates are needed to curb inflation

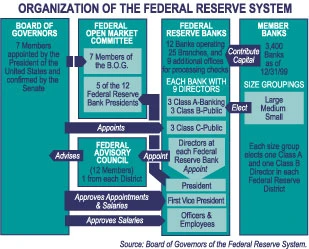

The Federal Reserve left its benchmark rate unchanged at 3.50% to 3.75% at its June 16-17 meeting, keeping borrowing costs pinned near their current level while leaders debated how much more restraint inflation still needs. The split now centers on whether the central bank can restore price stability without holding rates higher for longer.

That argument matters because the Fed’s 2% inflation goal, measured by the personal consumption expenditures price index, has been in place since January 2012 and was reaffirmed in its 2025 strategy statement. The St. Louis Fed says PCE inflation has stayed above that target since March 2021, and inflation was still 2.9% in 2025. At the same time, the unemployment rate rose to 4.3% in January 2026 from 3.4% in April 2023, sharpening the tension between the Fed’s dual mandate of price stability and maximum employment.

Officials have signaled they are not ready to declare victory. Recent Federal Open Market Committee communications said the committee would adjust policy if inflation pressures persist and that inflation expectations remain central to its decisions. That leaves the market facing a simple but uncomfortable test: unless the Fed sees a durable move back toward 2% in PCE inflation, relief in borrowing costs is unlikely to come quickly.

The hardest part of that judgment is that the last leg of disinflation usually comes from the slowest-moving parts of the economy, especially services and housing. Those categories tend to keep pressure on prices even after goods inflation eases, which is why the debate inside the Fed is no longer just about how high rates should go, but how long they need to stay there.

History still hangs over the discussion. The Great Inflation lasted from 1965 to 1982, and in October 1979 Paul Volcker announced anti-inflation measures that helped restore the Fed’s credibility but also ushered in a painful recession. That precedent is now the cautionary tale for current policymakers: if inflation proves sticky again, the central bank may decide that the only way to win is to keep borrowing costs elevated until price growth clearly breaks back to target.