US News

Fed paper finds unauthorized immigration raised rents, home prices modestly

Federal Reserve Bank of Dallas Working Paper 2607 finds that unauthorized immigration raised local rents and home prices in markets where housing supply could not quickly adjust. It does not show that immigration alone explains the pandemic-era surge in housing costs, and it does not justify treating every national affordability problem as the product of one policy failure.

What the Dallas Fed paper actually says

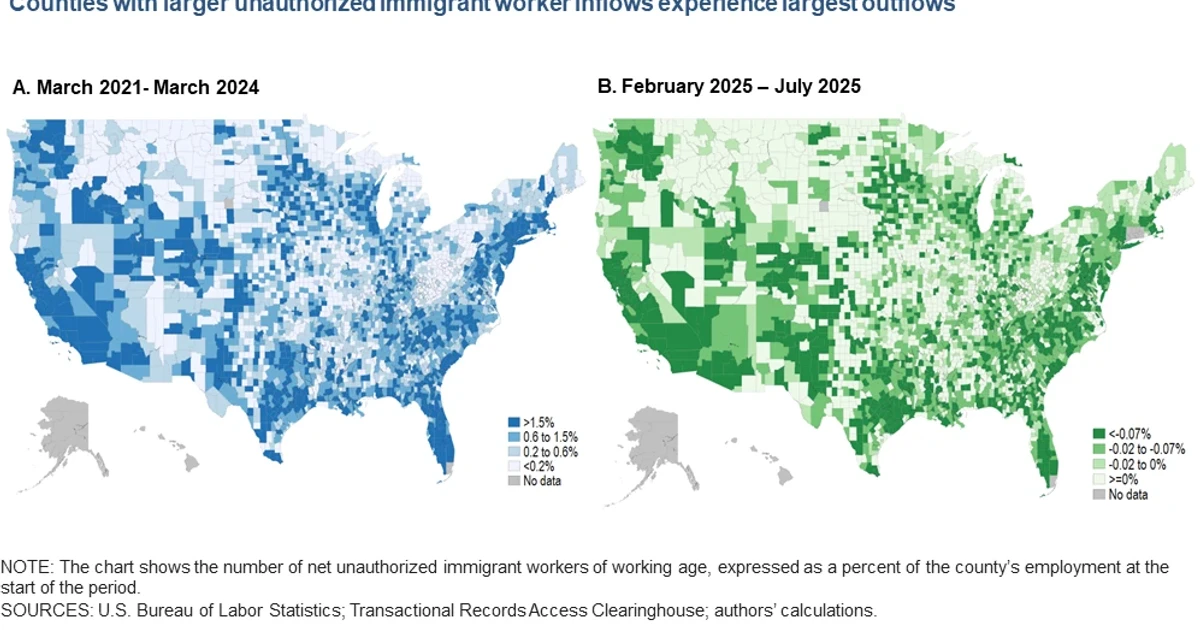

Daniel J. Wilson and Xiaoqing Zhou used newly available administrative microdata to study unauthorized immigration and local housing markets in Federal Reserve Bank of Dallas Working Paper 2607, published in March 2026. They write that the United States saw an “unprecedented boom” in unauthorized immigration from early 2021 to early 2024, followed by a rapid slowdown beginning in mid-2024.

In markets with short-run inelastic housing supply, these inflows acted like a housing-demand shock. Wilson and Zhou estimate that unauthorized immigration raised local home prices by about 2.2 percent and rents by about 1.4 percent, while also boosting employment, reducing labor income per capita, and reducing government transfers.

That is a different claim from the one often heard in campaign rhetoric. The paper describes localized price pressure in tight markets; it does not say immigration was the main engine of the national housing crisis, and it does not say immigrants were responsible for the entire rise in home values or rents.

Why the headline numbers are easy to misuse

One point of confusion is the 22.4 percent figure attached to the total weighted-mean increase in house prices over the boom period. That number describes the overall price change during the period the authors study. It is not a direct estimate that unauthorized immigration alone caused a 22.4 percent or 30 percent increase in housing prices.

Political shorthand often collapses several different quantities into one accusation. A model-based estimate of a 2.2 percent local price effect is not the same thing as a broad claim about the entire market, especially in a period when pandemic disruptions, remote work, construction slowdowns, mortgage-rate spikes and regional demand shifts were all moving housing costs at once.

The paper also leaves open the role of market tightness. Its own mechanism depends on supply being slow to respond, which means the effect is larger where new construction is constrained and smaller where homes can be added more quickly. In other words, the same population shock does not land the same way everywhere.

Timing is the missing piece in the political argument

The timing of the immigrant surge does not line up neatly with the first wave of housing inflation. Harvard’s Joint Center for Housing Studies found that the recent immigrant surge does not match the sharp rise in rents and home prices that began at the start of the pandemic in 2020 and 2021.

Housing costs were already accelerating before the later surge in unauthorized immigration intensified, which suggests the market was responding to deeper structural pressures that predated the latest border fight.

The Federal Reserve has also long treated housing as the largest expense for most families. Even modest increases in rents and mortgage costs can strain household budgets. When those costs rise in already tight markets, the pain falls hardest on renters, first-time buyers and lower-income households who have the fewest buffers.

The bigger drivers are still supply, financing and regional demand

Housing supply constraints remain one of the most durable forces shaping prices. Fed research has previously found that housing supply shortages have sizeable effects on house prices, and that is consistent with what families see on the ground: too few homes in the places where jobs, schools and transit make them valuable.

Financing conditions matter too. A separate Federal Reserve analysis by Aditya Aladangady, Jacob Krimmel and Tess Scharlemann found that about 44 percent of the decline in moves among mortgage holders between 2021 and 2022 could be attributed to the widening gap between borrowers’ existing rates and market rates. Another Fed study found that the 2022 lock-in shock reduced time on market by 29 percent and increased house prices by 8 percent.

The housing market froze from the inside. When owners are locked into cheaper mortgages, fewer homes come up for sale. That reduces mobility, keeps supply tight and pushes prices higher in places where demand remains strong.

Regional demand still matters as well. Growth in high-wage metro areas, migration within the United States and the uneven pace of new construction all shape where prices rise fastest. The Dallas paper fits into that broader picture as one local demand shock among many, not as a stand-alone explanation for the national crisis.

What this means for the policy debate

Donald Trump and his allies have repeatedly argued that undocumented immigration worsens housing affordability. The Dallas Fed paper gives that argument some empirical support in one specific sense: unauthorized immigration can raise rents and home prices in local markets that cannot add supply quickly enough.

But the study also reinforces a more complicated conclusion. If policymakers focus only on immigration, they miss the conditions that turn population growth into higher housing costs: zoning that limits new construction, financing constraints that freeze turnover, and a housing stock that has not kept pace with demand in many regions.