Business

Fed projections point to higher rates as inflation worries grow

Federal Reserve officials kept interest rates unchanged on June 17, but the real signal was in their projections: policymakers were split between staying put and pushing rates higher as inflation worries intensified. The Federal Open Market Committee left its benchmark overnight borrowing rate in a range of 3.5% to 3.75% at the June 16-17 meeting, Kevin Warsh’s first as Fed chair.

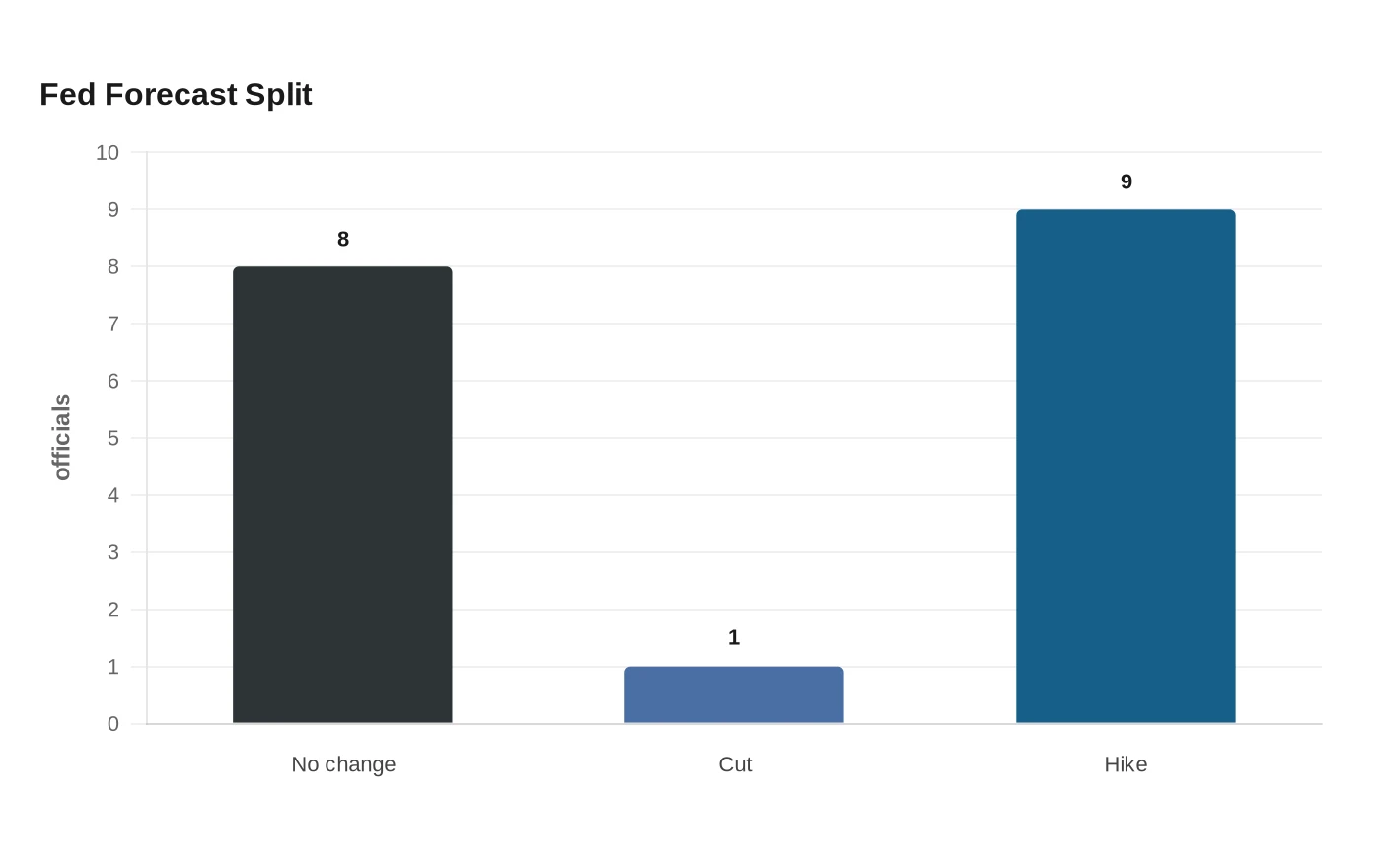

The new Summary of Economic Projections showed a median forecast for the federal funds rate at the end of 2026 rising to 3.8% from 3.4% in March. That shift pointed to a harder line than the market had been watching, with participants split three ways: eight expected no change, one saw a cut and nine anticipated at least one hike. The message was not that a move was imminent, but that the center of gravity inside the Fed had shifted toward tighter policy.

Warsh did not submit a personal dot in the June plot, and he said at his post-meeting news conference that he did not think it was helpful in conducting policy. He also signaled openness to a broader review of the Fed’s communication tools, an important detail for an institution whose forecasts and language often move markets as much as the rate decision itself. The June policy statement was shorter than before and removed language that had implied a bias toward future cuts.

That language change mattered because the Fed had been holding rates in the same range since it cut borrowing costs by 75 basis points in late 2025. Now, with inflation still elevated and the labor market remaining solid, the central bank appeared less interested in signaling near-term relief and more focused on keeping policy restrictive long enough to restrain price pressures.

The projections also underscored how quickly the debate inside the Fed had changed. Officials submitted forecasts for growth, unemployment and inflation alongside their rate views, and the rate path suggested they were weighing not just whether to wait, but whether the next policy mistake would be moving too soon or not tightening enough. For markets, the hold was the headline; the division over cuts versus hikes was the bigger story.

Sources

- [1]nytimes.com

- [2]federalreserve.gov

- [3]cnbc.com

- [4]reuters.com