Business

Fed says all 32 biggest US banks pass stress test

All 32 of the nation’s biggest banks cleared the Federal Reserve’s annual stress test, showing that the country’s largest lenders would stay above minimum capital levels even after a severe global recession.

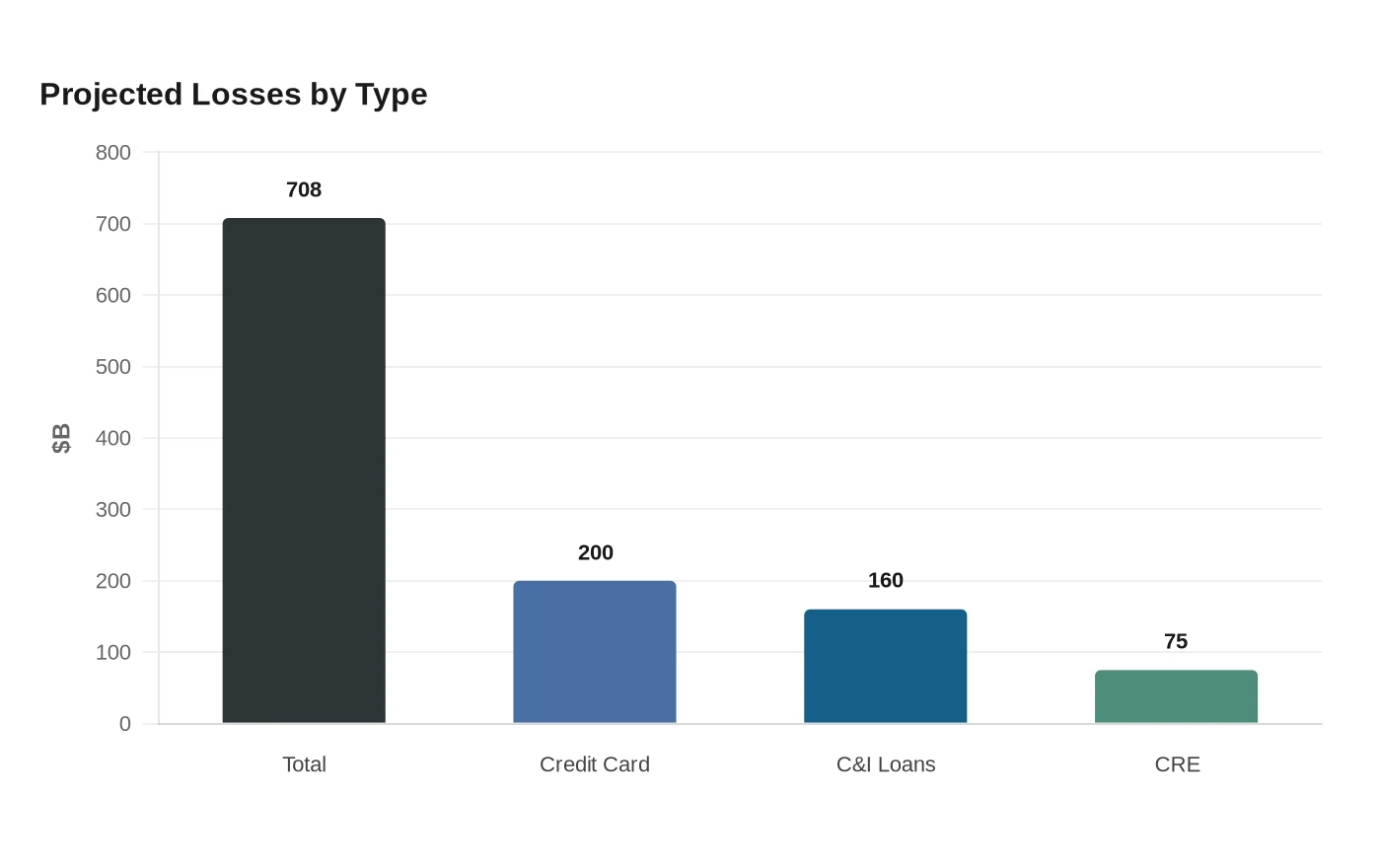

The Fed’s 2026 scenario assumed unemployment would rise from 5.5 percent to 10 percent, U.S. housing prices would fall 30 percent, commercial real estate values would drop 39 percent and the stock market would plunge 58 percent. Under those conditions, the 32 banks would take more than $708 billion in losses, including about $200 billion in credit card losses, $160 billion in commercial and industrial loan losses and $75 billion in commercial real estate losses. Even so, the sector’s combined common equity tier 1 capital ratio fell only 1.6 percentage points, from 12.8 percent to 11.2 percent.

Soon after the Fed’s release, JPMorgan Chase raised its quarterly dividend 10 percent to $1.65 a share and authorized a new $50 billion buyback program effective July 1. Goldman Sachs raised its quarterly dividend 11 percent to $5 a share, Morgan Stanley lifted its dividend 15 percent to $1.15 a share and reauthorized a $20 billion buyback, Wells Fargo expected to raise its dividend 11 percent to 50 cents a share, and State Street increased its dividend 10 percent.

The central bank said the 2026 results will not change large bank capital requirements, which are set to remain in place until 2027. The next round will use stress capital buffer models informed by public feedback. The aggregate capital decline was smaller than last year’s 1.8 percentage point drop, even though projected losses climbed above $708 billion from more than $550 billion a year earlier, helped in part by higher loan income and smaller hypothetical declines in interest rates.

Sources

- [1]usnews.com

- [2]federalreserve.gov

- [3]cnbc.com

- [4]finance.yahoo.com