US News

FTC warns debt relief companies can be risky, urges caution

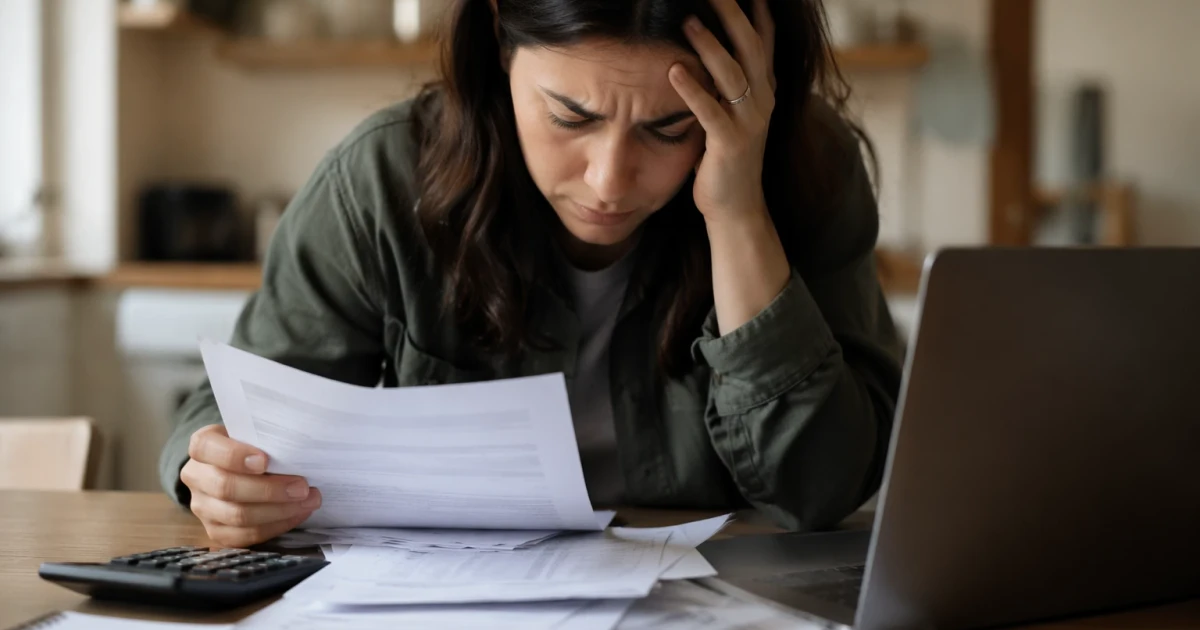

Consumers shopping for debt relief got a blunt warning: walk away from any company that asks for money before it has actually reduced a debt or enrolled an account in a debt management plan. Federal regulators warn that upfront fees, vague promises and missing paperwork are among the clearest signs that a debt relief shop may be risky.

The Federal Trade Commission has brought scores of law-enforcement actions against bogus credit-related services and, with states, hundreds of additional lawsuits. In 2010, the agency amended its Telemarketing Sales Rule to protect people seeking debt relief services, barring for-profit companies that sell those services over the telephone from charging a fee before they actually settle or reduce a consumer’s debt. The rule also requires providers to disclose key information and forbids misrepresentations.

The FTC reinforced that warning in 2025: legitimate organizations do not try to charge consumers before they settle debts or enter a debt management plan. It also urged consumers to get any agreement in writing, a safeguard that can help expose hidden fees, unrealistic timelines and other terms that may not be obvious in a sales pitch.

The Consumer Financial Protection Bureau warns that debt relief or settlement companies may offer to renegotiate, settle or otherwise change debt terms, but working with them can be risky.

For some households, a safer route may be nonprofit credit counseling. The National Foundation for Credit Counseling is a nonprofit network of certified credit counseling agencies founded in 1951. It serves all 50 states and all U.S. territories and offers one-on-one financial reviews and personalized financial action plans through certified counselors.

Consumers can also go directly to a credit card company and ask for a payment plan, which can sometimes be arranged free of charge. That option can avoid third-party fees altogether and may give households more control over how they deal with unsecured debt.

Sources

- [1]cbsnews.com

- [2]ftc.gov

- [3]consumerfinance.gov

- [4]consumer.ftc.gov

- [5]nfcc.org