Business

How a $100,000 short-term CD can earn around 4% APY safely

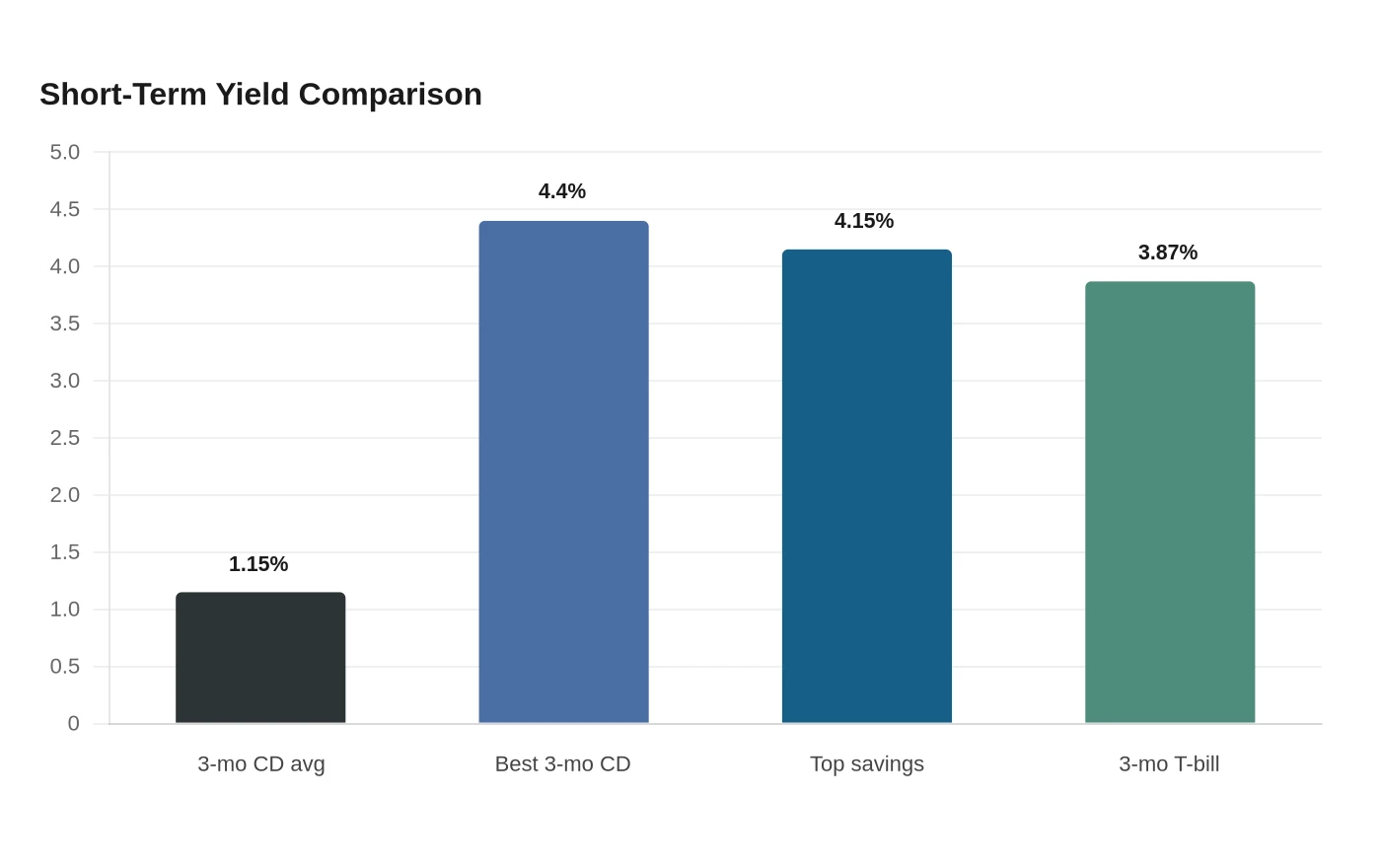

The FDIC’s June 2026 table puts the national average rate on a 3-month CD at 1.15%, but the best short-term offers are still clustered near 4% APY. A three-month CD fixes your return for 90 days. That gap is why online banks and credit unions still dominate the rate search, and why the decision is less about chasing the top sticker and more about deciding whether certainty is worth the lockup.

What a $100,000 three-month CD really pays

At 4.0% APY, a $100,000 deposit earns about $985.34 over three months. At 4.4% APY, the same balance earns about $1,082.30 over the same 90-day stretch. They also show how modest the dollar gain is on a short term, even before tax.

In Bankrate’s July 2026 tracker, the best CD rates are still around 4% APY overall, and the highest rate tracked is 7.50% at SF Fire Credit Union. CNBC Select’s July 2026 list has the best 3-month CDs at up to 4.40% APY. For most households, the realistic short-term CD range is a little above 4%, not the extreme advertised rates that headline national lists.

Why the safety label matters

The safety case for a $100,000 CD is straightforward: FDIC insurance covers up to $250,000 per depositor, per FDIC-insured bank, for each ownership category. That means a single $100,000 CD can be fully insured at one bank if it sits in one ownership category, without any need to spread it around just for coverage. Use the FDIC’s EDIE calculator if the account structure is more complicated, because it maps coverage by ownership type rather than by guesswork.

Taxes and inflation are the real test

CD interest is taxable as ordinary income, and the IRS treats interest as taxable in the year it becomes available to you. On a $100,000 three-month CD earning 4.0% APY, the roughly $985 in interest falls to about $749 after 24% federal tax. At 4.4% APY, the after-tax interest is about $823.

Inflation is the harder part of the math. In the latest BLS reading for May 2026, consumer prices were up 4.2% over the prior 12 months, and that works out to about $1,034 of purchasing-power erosion over three months on a $100,000 balance. Against that backdrop, the CD’s after-tax interest does not fully offset inflation, which means the nominal gain is real on paper but thin in purchasing-power terms.

How CDs compare with savings and Treasuries

High-yield savings is the main alternative when you want access without a maturity date. In Bankrate’s July 9, 2026 survey, the top savings account APY is 4.15% from Forbright Bank, while the national average savings yield is only 0.6% APY. On a $100,000 balance, that top 4.15% rate produces about $1,021.73 over three months before tax, or about $776.52 after a 24% federal tax rate, but the money stays liquid.

Treasury bills are the other obvious comparison. Treasury’s July 8, 2026 daily curve shows a 3-month rate of 3.87%, which generates about $953.77 over three months before tax on $100,000 and about $724.86 after a 24% federal tax rate. Earnings on marketable Treasury securities are exempt from state and local income taxes, so the after-tax picture can look better than the headline rate suggests for households in states with their own income tax.

When the lockup is worth it

A short-term CD makes the most sense when the cash has a near-term job and you can live without it until maturity. In Forbes Advisor’s 2026 outlook, CD and savings rates generally follow the federal funds rate, and rates fell significantly late in 2025, which is why locking a fixed 90-day return still has value if you expect yields to drift lower.

FDIC truth-in-savings rules require at least seven days’ simple interest if money is withdrawn within the first six days, and Bankrate’s July 2026 guidance puts common early withdrawal penalties at 60 to 365 days of interest depending on the institution and term.

Sources

- [1]cbsnews.com

- [2]bankrate.com

- [3]cnbc.com

- [4]fdic.gov

- [5]irs.gov

- [6]edie.fdic.gov