Business

How much $1,000 earns in a money market account now

At Bankrate’s average money market account rate for July 10, 2026, a $1,000 balance earns about $4.50 over a full year. The FDIC’s national average is only slightly higher, and the best advertised accounts still require you to shop carefully if you want a return that matters for an emergency fund.

What $1,000 earns right now

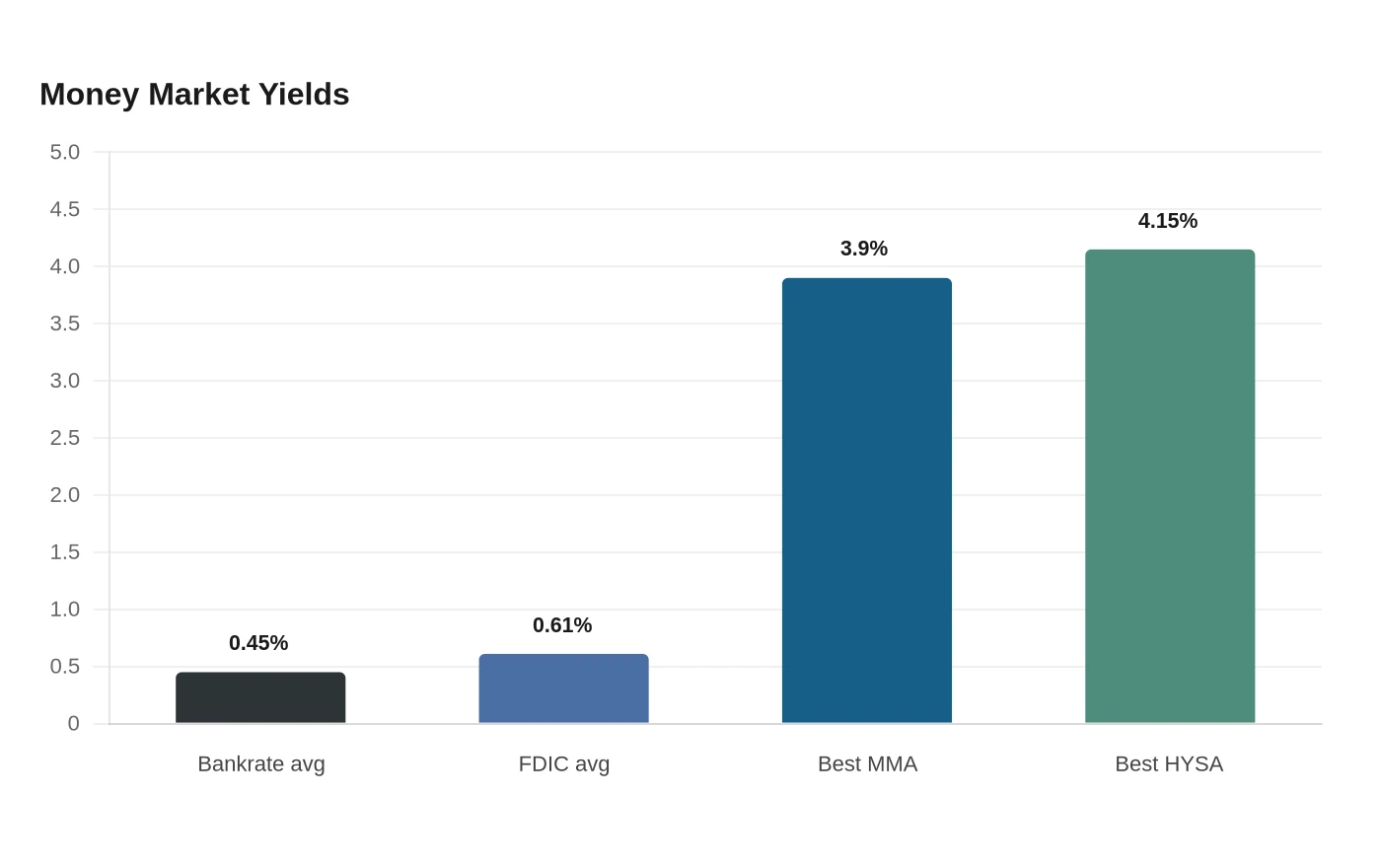

Bankrate lists the average money market account yield at 0.45% annual percentage yield for the week of Friday, July 10, 2026. The FDIC’s June 15, 2026 national rate data is a bit higher at 0.61% for the $10,000 tier, but that still works out to only about $6.10 on a $1,000 balance.

A money market account is not a vehicle for building wealth on a $1,000 balance. It is mainly a place to park cash with some yield, some liquidity, and a layer of deposit protection.

Why the headline APY can be misleading

The difference between average and best-in-market offers is huge. Bankrate’s July 2026 best-money-market-account list shows top advertised APYs up to 3.90%, which would generate about $39 a year on a $1,000 balance if that rate held for the full year. That is a much better return than the average account, but it is still modest in absolute dollars.

Even that better outcome can shrink fast once taxes enter the picture. Interest from a taxable account is counted as income, so the saver does not keep the full amount, and inflation chips away at the purchasing power of what remains. On a small balance, a money market account can preserve liquidity and safety, but it usually does not create a real gain in spending power.

How money market accounts fit beside high-yield savings, CDs, and Treasury bills

Money market accounts can offer check-writing privileges and debit card access, which makes them more flexible than many savings accounts. At FDIC-insured banks, they are covered by FDIC deposit insurance just like savings accounts and certificates of deposit, and that insurance is automatic. FDIC deposit insurance generally protects up to at least $250,000 per depositor, per insured bank, per ownership category.

That safety is one reason money market accounts remain popular for emergency funds, but yield is where they usually fall short. Bankrate’s July 2026 list puts the best online high-yield savings accounts at 4.15% APY, above the top advertised money market rate of 3.90%. CDs and Treasury bills often compete for the same cash, and their main appeal is that they can pay more if you are willing to give up some flexibility or accept a maturity date.

For a small balance, the choice is less about squeezing every last penny out of the account and more about deciding whether the convenience is worth the lower yield. If you need easy access, a money market account can be useful. If the goal is simply to maximize return, high-yield savings accounts, CDs, and Treasury bills can pay more.

Why rates have moved down

Money market yields tend to follow Federal Reserve policy, which helps explain why today’s payouts are muted. The Federal Reserve lowered the target range for the federal funds rate to 4 to 4-1/4 percent on Sept. 17, 2025, then cut it again to 3-1/2 to 3-3/4 percent on Dec. 10, 2025. Before that, the Board of Governors of the Federal Reserve System had held the target range at 4-1/4 to 4-1/2 percent on July 30, 2025.

Short-term deposit yields usually move in the same direction as the Fed’s policy rate. When the policy rate declines, banks often have less reason to pay aggressively on cash deposits, and money market accounts feel that pressure quickly.

How to tell whether a money market account is actually worth it

The most useful question is not whether a money market account has an eye-catching APY. It is whether the account gives you enough flexibility and insurance for the role you need it to play. For an emergency fund, the combination of FDIC coverage, liquidity, and the ability to write checks or use a debit card can be worth more than a slightly higher rate elsewhere.

Before moving cash, check three things:

• The APY, not the teaser rate • Whether the account is at an FDIC-insured bank • How much of your balance is covered under FDIC rules

FDIC tools such as EDIE can help you verify what portion of your deposits is insured. That matters most when balances rise above standard coverage limits or when money is spread across multiple accounts and ownership categories.

Sources

- [1]cbsnews.com

- [2]bankrate.com

- [3]fdic.gov

- [4]federalreserve.gov