Business

How much $35,000 earns in a high-yield savings account now

A $35,000 balance in Bankrate’s top 4.15% high-yield savings account earns about $1,452.50 in a year before taxes.

What $35,000 earns at today’s best rates

The spread across the top of the market is small. NerdWallet’s July list, current as of July 7, showed savings APYs up to 4.10%, which would produce about $1,435 in annual interest on $35,000 before taxes, only $17.50 less than Bankrate’s 4.15% leader from Forbright Bank. By contrast, Bankrate’s national average savings yield of 0.6% would generate only about $210 over the same year, a gap of $1,242.50 before taxes.

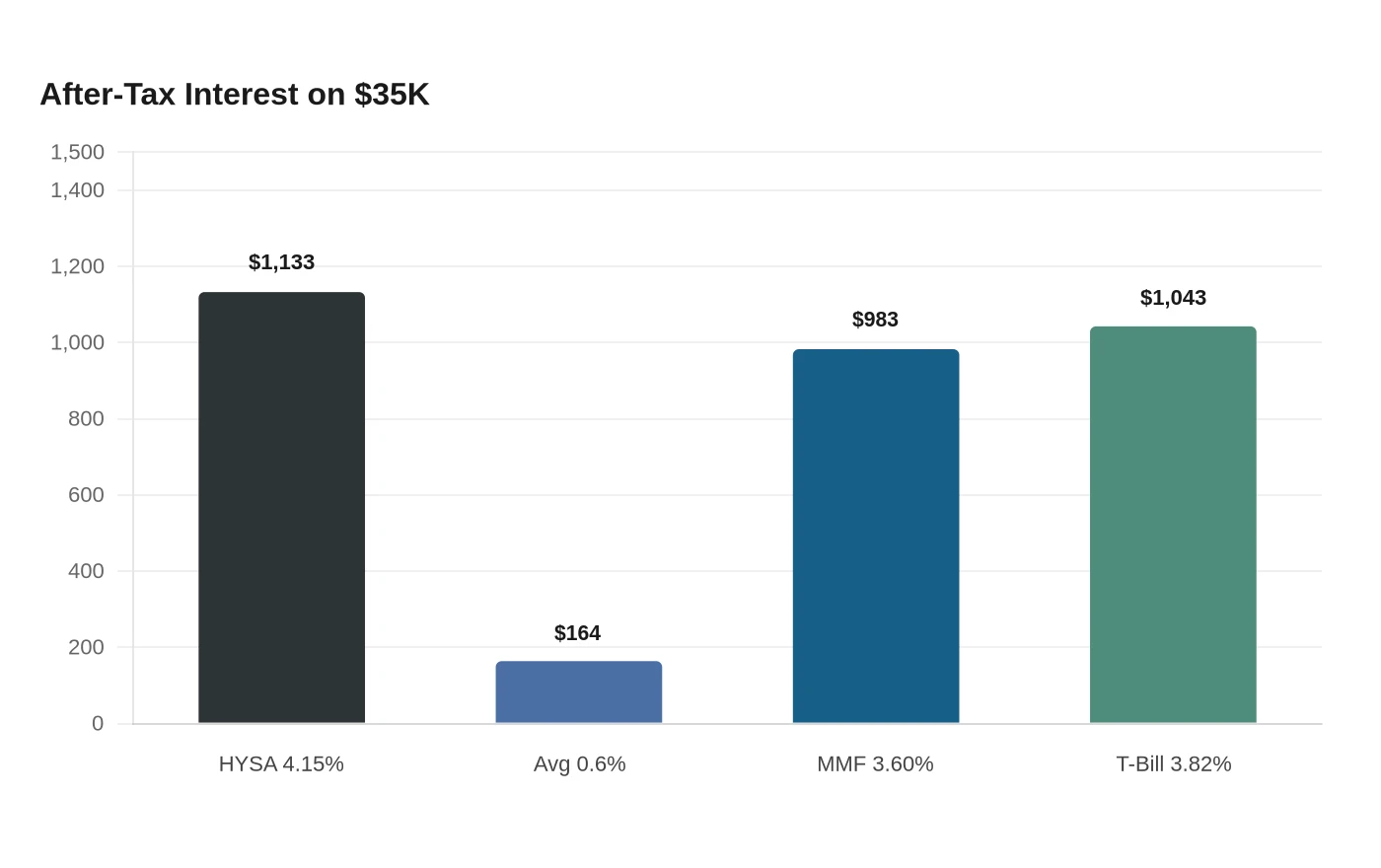

For a saver in the 22% federal bracket, which begins above $50,400 of taxable income for a single filer in 2026, that top 4.15% account would leave about $1,133 after federal tax. The national-average 0.6% account would leave only about $164 after tax, so the higher-yield option improves after-tax interest by roughly $969 on a $35,000 balance before inflation is even considered.

Why the Fed backdrop matters

The Federal Reserve kept its target range at 3.5% to 3.75% on June 17, 2026, and that backdrop helps explain why deposit yields are still attractive relative to the last few years. Savings rates generally move with broader interest-rate conditions, so when short-term rates stay elevated, banks can continue offering high-yield accounts that are far above the old 0.6% average.

The Consumer Financial Protection Bureau’s Regulation DD is designed to help consumers comparison-shop for deposit accounts, and institutions must disclose APY, interest rates, minimum-balance requirements, account-opening disclosures and fee schedules. APY itself measures the total amount of interest paid based on the interest rate and the frequency of compounding over a 365-day period.

How the alternatives stack up

A high-yield savings account is still a deposit account, so the safety profile is different from a mutual fund. FDIC deposit insurance is automatic at FDIC-insured banks and covers savings accounts, money market deposit accounts and CDs up to at least $250,000 per depositor, per bank, per ownership category; NCUA share insurance protects savings at federally insured credit unions. By contrast, a money market mutual fund is an investment product, not an insured deposit.

Vanguard’s Federal Money Market Fund showed a 7-day SEC yield of 3.60% on July 2, 2026, while the Federal Reserve’s 3-month Treasury constant maturity rate stood at 3.82% on July 2. On a $35,000 balance, those rates translate to about $983 and $1,043 of after-tax interest, respectively, assuming the same 22% federal bracket used above.

Under IRS rules, interest on Treasury bills, notes and bonds is subject to federal income tax but exempt from state and local income taxes. That state-tax exemption can make short-term Treasuries especially competitive for savers in states with higher income taxes, even when the headline yield looks close to a bank account.

What the inflation math says

May’s 4.2% annual CPI reading is the number that matters for buying power, not just the bank’s APY. A 4.15% account looks strong against the 0.6% average, but it still trails inflation before taxes, and after tax it falls further behind in real terms. Using the 22% bracket, the 4.15% account leaves you about $323 poorer in purchasing power after one year, while a 0.6% account leaves you about $1,254 poorer.

Moving from a 0.6% traditional savings account to a 4.15% high-yield account adds about $969 of after-tax interest on $35,000, and improves the real outcome by about $930, even though inflation still erodes part of the gain.

What to check before moving the money

The best rate is only useful if it is actually available on your balance and does not come with a fee structure that eats the yield. Bankrate’s top high-yield accounts typically pair competitive APYs with low minimum deposits and no monthly fees, but APYs can change and may vary by region or account conditions.

Sources

- [1]cbsnews.com

- [2]federalreserve.gov

- [3]consumerfinance.gov

- [4]bankrate.com

- [5]nerdwallet.com