Business

How much a $10,000 18-month CD can earn now

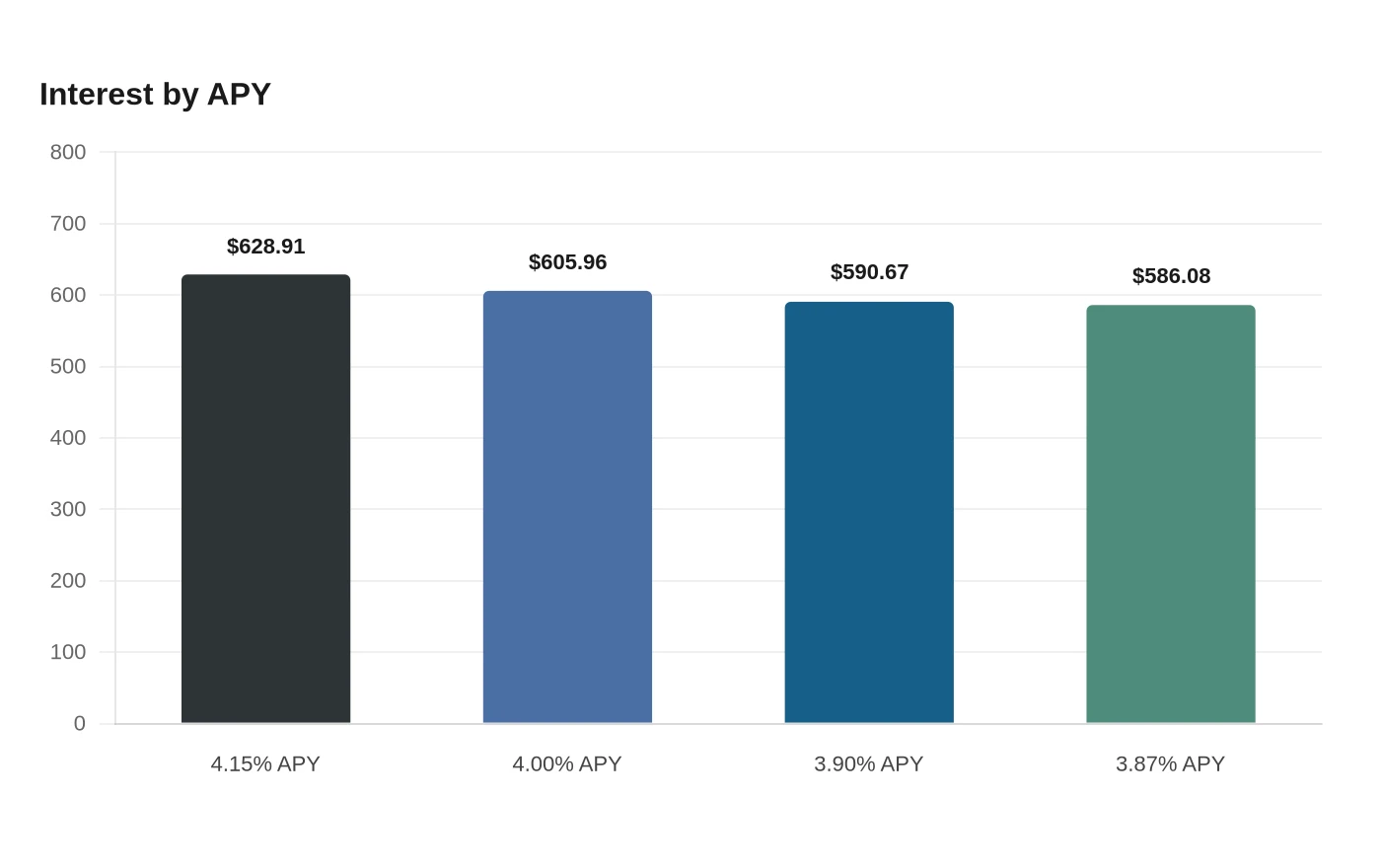

A $10,000 18-month CD at 4.15% APY would earn $628.91 in interest by maturity. The bigger question is whether locking in a fixed return now is smarter than leaving the money in a savings account that could drift lower if rates keep falling.

What a $10,000 CD pays right now

The math is straightforward, and the range still matters. The best 18-month CDs in July 2026 are about 4% to 4.30% APY, which puts a $10,000 deposit on track to produce hundreds of dollars in interest before maturity.

At 4.00% APY, the same deposit would earn $605.96. Small rate differences still move the final payout: a $10,000 CD at 3.87% APY would earn $586.08, while 3.90% APY would return $590.67.

The return is guaranteed if you keep the deposit in place through maturity, so the saver knows in advance exactly what the account will deliver.

Why savers are looking at CDs now

The Federal Reserve cut rates three times in 2024 and cut again in September 2025, which is one reason deposit rates have been under pressure. Bankrate's weekly national survey and Forbes Advisor both project that savings rates are likely to be lower in 18 months.

If rates soften over the next year and a half, a new CD opened later could pay less than a CD opened today. The tradeoff is simple: a CD protects today’s yield, while a savings account leaves you exposed to whatever banks decide to pay next.

CDs versus high-yield savings accounts

High-yield savings accounts still matter because liquidity has value. You can add or remove money without a penalty, which makes them better for emergency funds, near-term home repairs, tuition bills, or any expense that could arrive before an 18-month term ends.

An 18-month CD asks you to give up that flexibility in exchange for a fixed rate. If a top CD is paying around 4% to 4.30% APY and a high-yield savings account is close to that range, the gap may not be large enough to justify tying up cash you might need. If the savings rate slips while the CD stays fixed, the CD can become the better deal almost immediately.

A practical way to think about it is this:

• Use a savings account for money you may need at any time.

• Use an 18-month CD for cash you can leave untouched through maturity.

• Compare the CD yield not just to a headline savings rate, but to what you expect those savings rates to be six months, 12 months, or 18 months from now.

How inflation changes the decision

Inflation is the quiet force behind the decision. A fixed 4.15% APY looks attractive in nominal terms, but the real gain depends on whether prices rise more slowly than your return, and on how taxes affect the interest you keep. A saver who locks in 4% or a little above that is at least giving cash a chance to keep pace with moderate inflation, instead of watching a checking account earn almost nothing.

When rates are moving down, locking in a known return can help preserve purchasing power better than waiting for a better offer that may never show up. If inflation cools and rates fall together, the saver who acted earlier keeps the higher payout.

The safety net behind the return

The other part of the appeal is safety. CDs at FDIC-insured banks are covered up to at least $250,000 per depositor, per ownership category, and no depositor has lost a penny of FDIC-insured funds since the agency was founded in 1933. For a typical $10,000 deposit, that insurance means the money sits well inside the federal coverage limit.

That protection does not erase interest-rate risk, but it does remove credit risk at an FDIC-insured bank. In plain terms, the saver is not betting on the bank’s survival, only on whether the fixed rate is worth surrendering liquidity for 18 months.

When an 18-month CD is smart timing, and when it is a trap

An 18-month CD works best when cash is already earmarked for the medium term and you want certainty. It is a solid fit for money that is not needed for emergencies, because the term is relatively short compared with 2-year, 3-year, or 5-year CDs and still long enough to lock in a yield before deposit rates drift lower.

It becomes a trap if the money is likely to be needed sooner, or if you will resent the penalty for breaking the CD early. The saver who needs flexibility may do better in a high-yield savings account, even if the posted rate is a little lower, because access has its own economic value. The saver who can truly hold the money for 18 months can use the CD to turn today’s rate environment into a known outcome: roughly $606 to $629 on a $10,000 deposit at the rates now in play.

Sources

- [1]cbsnews.com

- [2]fdic.gov

- [3]bankrate.com

- [4]forbes.com

- [5]nerdwallet.com

- [6]congress.gov

- [7]cnbc.com