Business

How much a $50,000 CD can earn at today’s top rates

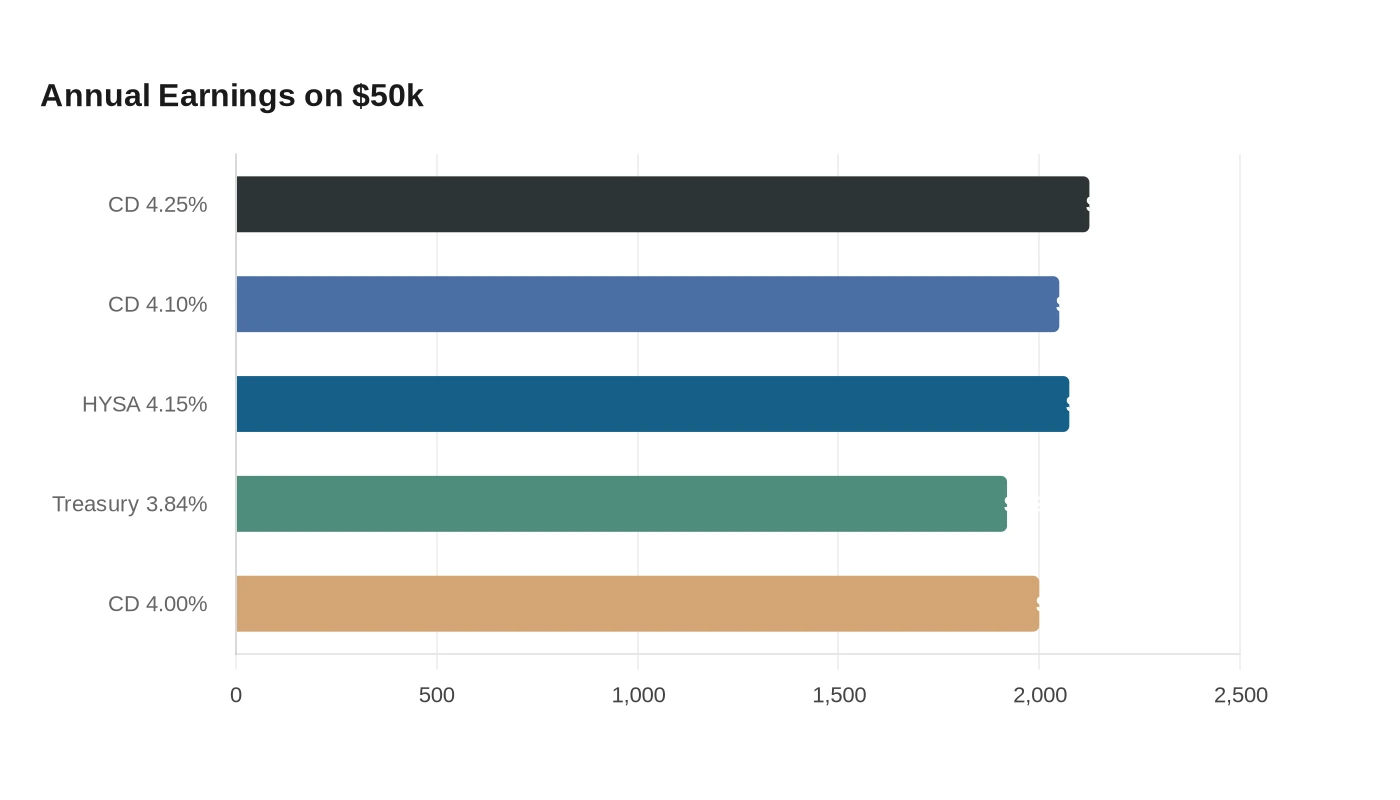

A $50,000 certificate of deposit at 4.25% APY would throw off about $2,125 in one year before taxes. At 4.10% APY, the same deposit would earn about $2,050, while a high-yield savings account paying 4.15% APY would produce about $2,075 and a one-year Treasury yield of 3.84% would generate about $1,920. The spread is small in headline terms, which is exactly why the opportunity cost matters: the money you lock into a CD is money you do not keep fully liquid.

That tradeoff is cushioned by deposit protection. The Federal Deposit Insurance Corporation insures deposits to at least $250,000 per depositor, per insured bank, per ownership category, so a single $50,000 CD sits well inside the standard coverage limit. The FDIC says no depositor has lost a penny of FDIC-insured funds since the agency was founded in 1933. CDs also fall under Regulation DD, which requires clear disclosures on APY, interest rates, and other account terms so consumers can compare time accounts before they lock money away.

Taxes change the picture quickly. The Internal Revenue Service treats CD interest as ordinary taxable income, and Treasury interest is federally taxable too, but exempt from state and local income taxes. That matters because inflation is still running hot enough to erase much of a nominal return: the Consumer Price Index rose 4.2% over the 12 months ending in May 2026. A 4.00% CD on $50,000 earns about $2,000 before tax, which already trails inflation by 0.2 percentage points; at 4.25%, the cushion is only about $25 a year before taxes. Once ordinary income tax is applied, the real return on either CD shrinks further.

That leaves a fairly clear sorting line. Savers who can leave cash untouched for the full term have a good case for locking in now, because Bankrate says the best CDs are still clustered around 4% APY and concentrated in short terms, a setup that protects today’s yield if rates fall later. Savers who may need the money soon are better off staying in a high-yield savings account, where the rate is close and the funds remain available. Treasurys sit in the middle: lower headline yield than the top CDs, but a tax advantage that can help investors in high-tax states.

Sources

- [1]cbsnews.com

- [2]bankrate.com

- [3]nerdwallet.com

- [4]fdic.gov

- [5]irs.gov

- [6]bls.gov

- [7]consumerfinance.gov