Health

Insurers urged to lend money to Obamacare consumers facing high deductibles

High deductibles are turning health insurance into a bridge to debt. One-third of Americans said they cut back on daily expenses to pay for health care, and KFF says 41% of adults reported medical or dental debt in 2022, including balances owed to banks and other lenders. Even insured households are not insulated from the strain, with borrowing now part of how many families keep up with care costs.

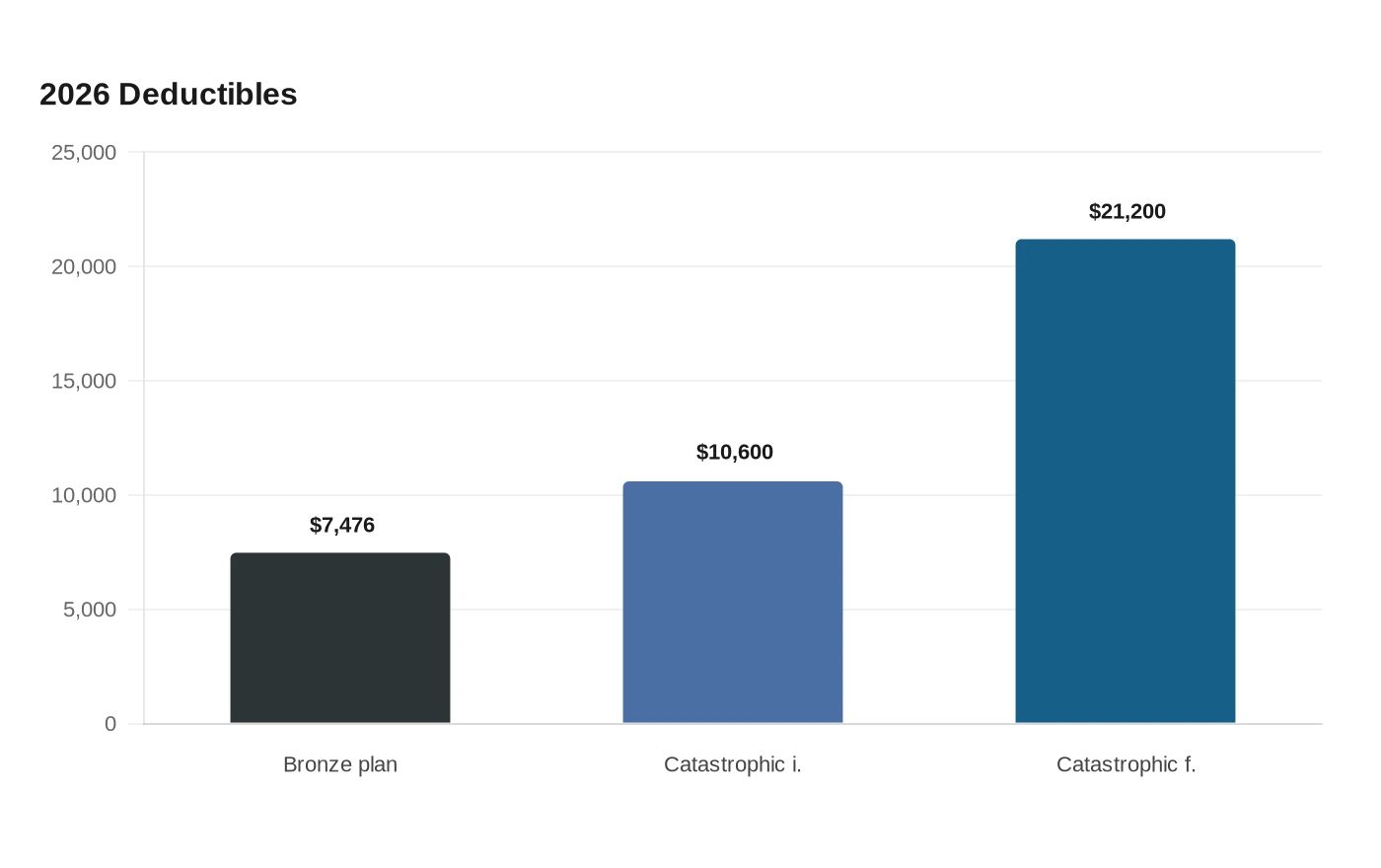

The pressure is especially visible in Obamacare plans. KFF says insurers are raising ACA premiums by 26% on average in 2026, and if enhanced premium tax credits expire, subsidized enrollees would see monthly payments more than double, by about 114% on average. For many shoppers, the cheaper premium comes with a much steeper bill later: the average bronze-plan deductible is $7,476 in 2026, while catastrophic plans carry deductibles equal to the ACA out-of-pocket maximum, $10,600 for an individual and $21,200 for a family.

Federal policy is moving in the same direction. A CMS proposal for 2027 would expand cost-sharing flexibility for bronze and catastrophic plans, establish catastrophic coverage terms of up to 10 consecutive years, and broaden hardship exemptions and other Marketplace changes. The result is a market that can advertise lower monthly premiums while shifting more of the financial burden to the point when a patient actually needs care.

That is the affordability paradox at the center of the current debate: insured patients are being nudged from medical coverage into debt products. Gallup’s West Health survey found that among uninsured adults, 32% had borrowed money to pay for health care, but the larger point is that financing is already part of the system for millions of Americans. If insurers are now being pressed to lend money to consumers facing high deductibles, the question is whether that is a practical bridge for patients or a concession that coverage no longer covers enough. Either way, the economics are plain: lower premiums are being bought with higher out-of-pocket risk, and households are left to finance the gap.

Sources

- [1]nytimes.com