Business

Lucid Motors denies bankruptcy rumors as stock plunges 57%

Lucid Motors denied bankruptcy and take-private rumors as “completely false” while its shares plunged as much as 57% to $2.37 in afternoon trading, with trading halted multiple times for volatility. The stock’s collapse left the Newark, California-based EV maker with shares down about 99% since the company went public nearly five years ago.

Lucid has sufficient liquidity to fund operations well into next year and has not formed any special board committee to explore bankruptcy or a take-private transaction. AlixPartners is helping improve execution and operations and has not recommended bankruptcy.

The pressure on Lucid has built even as the company has been reshaped under new chief executive Silvio Napoli, who took over in June 2026. On June 22, Lucid cut about 18% of its U.S. workforce, and chief operating officer Marc Winterhoff left the company. The leadership changes aimed to simplify the structure, sharpen accountability and improve execution.

On July 2, Lucid produced 4,774 vehicles and delivered 3,953 in the second quarter of 2026. In the first quarter, it produced 5,500 vehicles, delivered 3,093 and generated $282.5 million in revenue, ending the period with about $3.2 billion in liquidity. That figure rose to about $4.7 billion on a pro forma basis after its April capital raise.

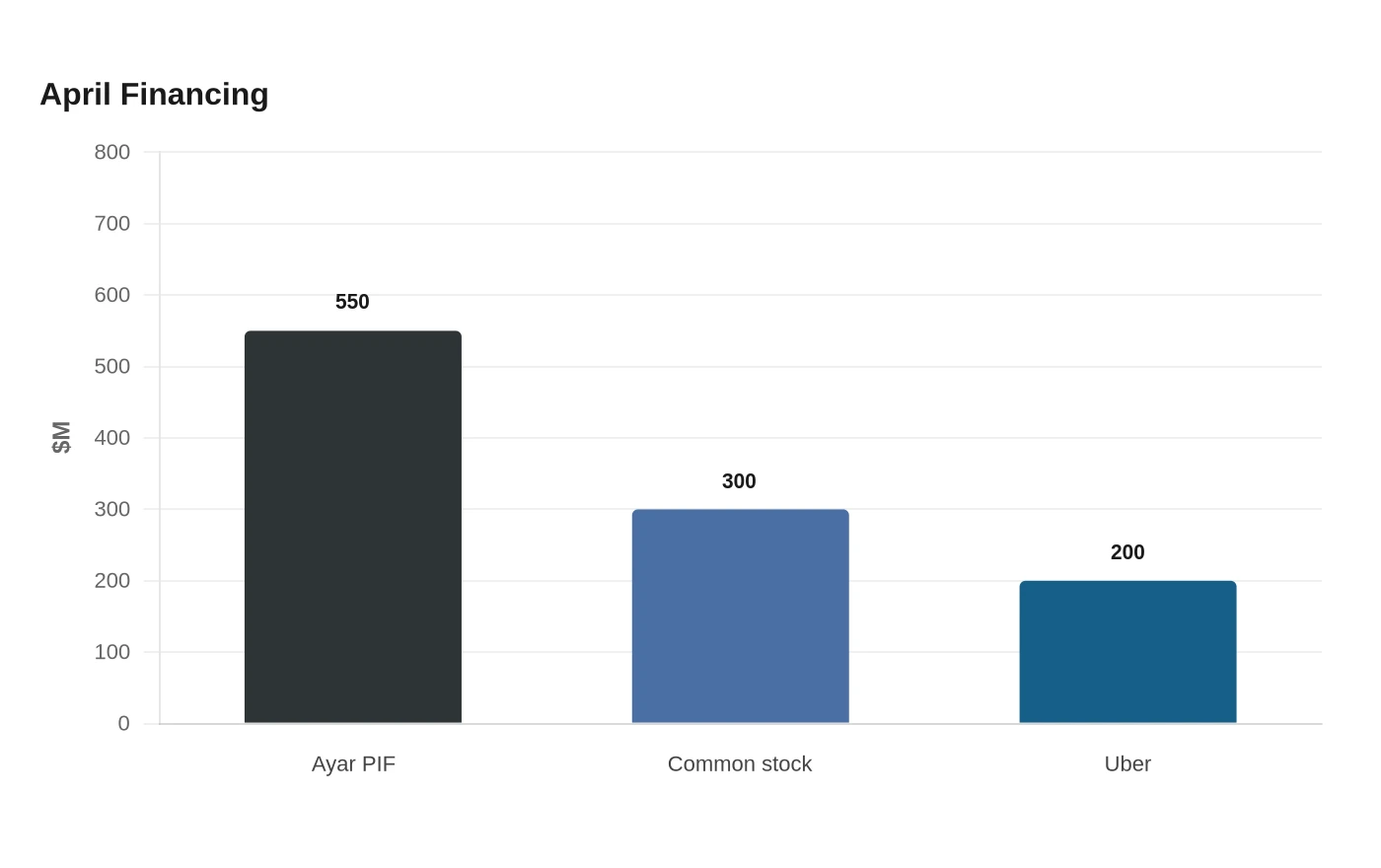

That April 14 financing totaled about $1.05 billion, including $550 million in convertible preferred stock from Ayar Third Investment Company, an affiliate of Saudi Arabia’s Public Investment Fund, $300 million from a registered common-stock offering and $200 million from Uber, lifting Uber’s total investment in Lucid to $500 million. Lucid also increased its Delayed Draw Term Loan by $500 million and drew $500 million in cash in April.

Lucid suspended its 2026 production target of 25,000 to 27,000 vehicles in May after supplier-related issues hit Gravity SUV deliveries.