Technology

Micron posts record results as AI demand tightens memory market

Micron Technology’s fiscal third-quarter revenue jumped to $41.46 billion, and the Boise, Idaho company said customers had already committed $22 billion to lock in memory-chip supply as AI demand tightened the market. The largest U.S. maker of computer memory chips also posted GAAP net income of $28.24 billion, or $24.67 per diluted share, and non-GAAP net income of $28.86 billion, or $25.11 per share.

The numbers were striking not just for their scale, but for what they signaled about Wall Street’s hunt for the next Nvidia. Micron projected fiscal fourth-quarter revenue of about $49 billion to $51 billion, far above market expectations, and said its outlook reflected “the strategic value of memory in the AI era.” Shares surged after the report, and global chip stocks followed higher as investors piled back into the AI trade.

Micron is not a graphics processor maker. It sells DRAM, NAND and high-bandwidth memory, the components now sitting closer to the center of AI infrastructure as server builders stuff more memory into systems that train and run large models. That shift has turned memory from a sleepy commodity business into one of the market’s most closely watched AI beneficiaries, even as investors continue to ask whether the enthusiasm is being stretched across every adjacent semiconductor name.

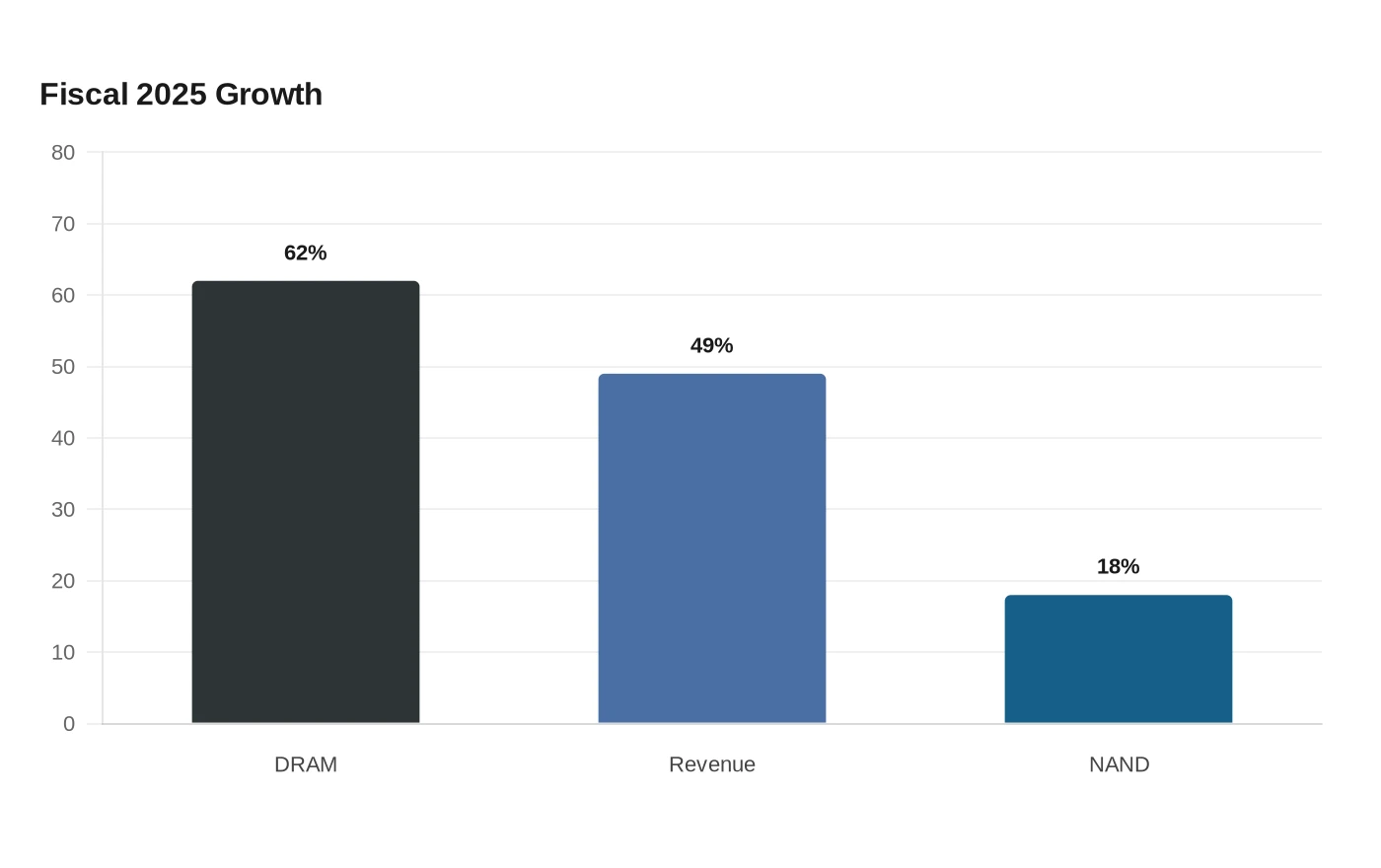

The company’s own filings show how sharply the business has changed. In fiscal 2025, Micron said revenue rose 49% from a year earlier, helped by a 62% increase in DRAM sales and an 18% increase in NAND sales. It also shifted part of its DRAM supply toward data-center and hyperscale cloud customers, with particular emphasis on high-bandwidth memory products designed for AI workloads.

That is the bullish case now gripping Wall Street: AI may finally be altering memory’s old boom-bust pattern. For years, chipmakers have expanded capacity just as demand weakened, leaving valuations depressed relative to faster-growing semiconductor designers. Micron’s latest results suggest the cycle may be different this time, with constrained supply, stronger pricing and a richer product mix tied to AI infrastructure all working in the company’s favor.

Still, the debate remains unresolved. Micron’s record profit and $22 billion in supply commitments point to durable demand today, but the market’s reaction also showed how eager investors remain to find a public company that can capture Nvidia-like gains without Nvidia-like economics.

Sources

- [1]techcrunch.com

- [2]investors.micron.com

- [3]money.usnews.com

- [4]wsau.com

- [5]publicnow.com

- [6]ca.finance.yahoo.com