Business

Mortgage rates dip to 6.47% as housing demand improves

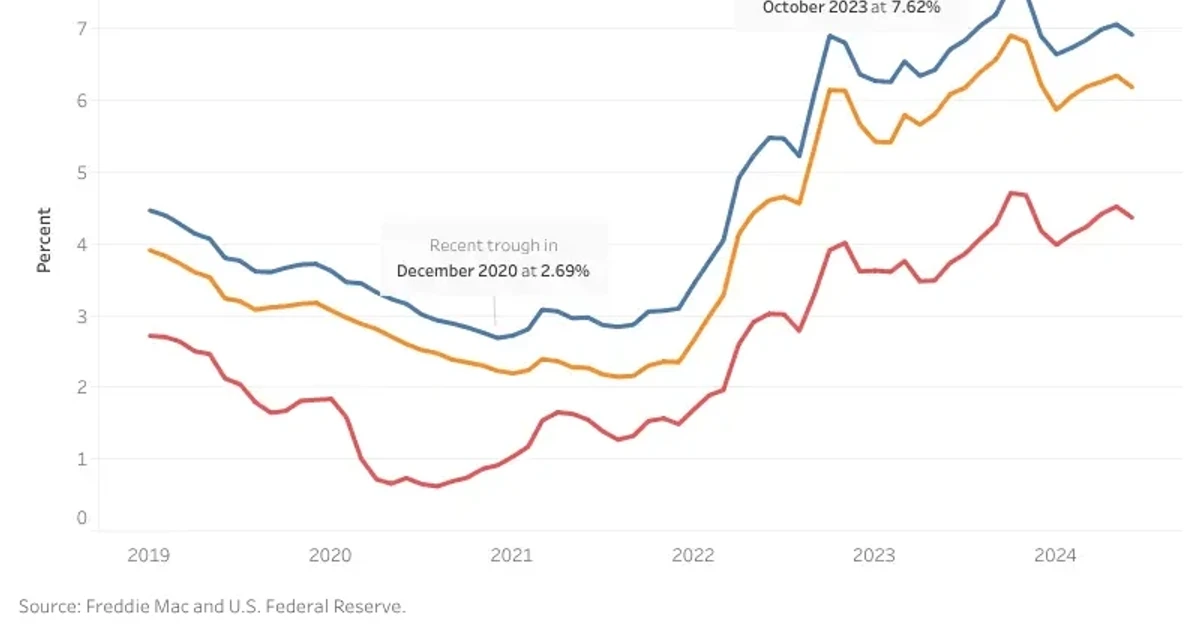

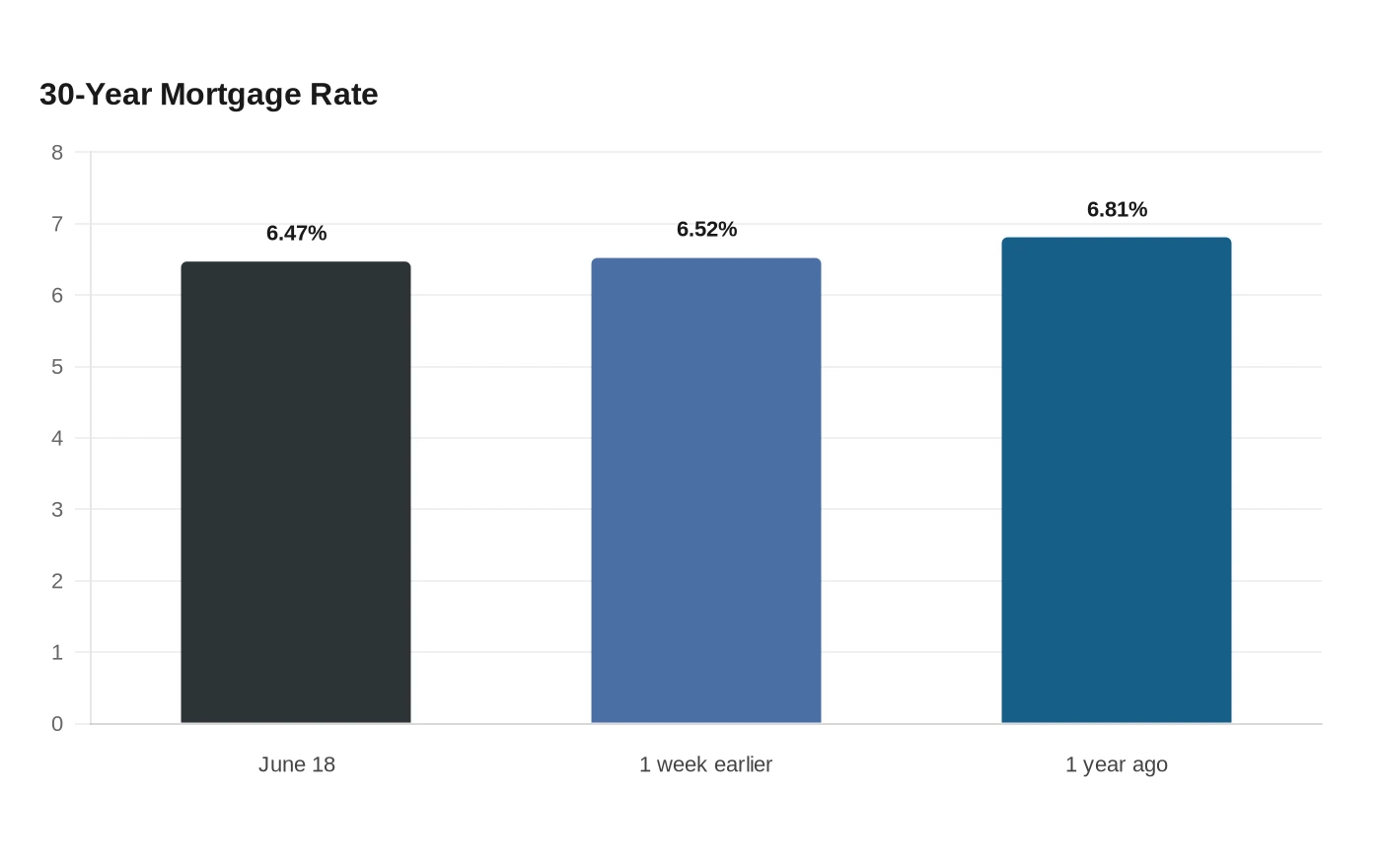

Freddie Mac said the average 30-year fixed mortgage fell to 6.47% on June 18, down from 6.52% a week earlier and 6.81% a year ago, while the 15-year loan averaged 5.81%. On a $400,000 loan, that five-basis-point drop cuts principal and interest by about $13 a month, a small move that still matters to buyers deciding whether to lock a rate now or wait for one more dip.

July’s next turn will come from the Fed, inflation and the bond market. The Federal Open Market Committee left its target range at 3.5% to 3.75% at its June 17-18 meeting, and its next scheduled meeting is July 28-29. The U.S. Bureau of Labor Statistics said the Consumer Price Index rose 0.5% in May and 4.2% over the past 12 months, the biggest annual increase since April 2023. The Fed will also be watching incoming jobs data, because policy changes work through employment and prices, while Treasury yields remain a key benchmark for mortgage pricing. If inflation cools and yields ease, rates can drift lower; if price pressures stay sticky, locking sooner looks safer.

Housing demand is already firming enough to keep lenders from relaxing too far. Freddie Mac’s economists said retail sales improved and pending home sales strengthened, signs that purchase demand is modestly improving, and the National Association of REALTORS® said existing-home sales rose 3.2% in May to a seasonally adjusted annual rate of 4.17 million. The median existing-home price reached $429,300, while inventory stood at 1.55 million units, equal to 4.5 months of supply. That mix usually limits how far rates can fall, because more buyers start competing for the same listings at the same time.

Freddie Mac’s Primary Mortgage Market Survey is built from loan-rate applications submitted by lenders nationwide and has data going back to 1971, making it a useful weekly check on whether mortgage quotes are actually following the bond market. With the survey released Thursdays at 12 p.m. ET, the clearest July strategy is to compare each lender’s quote against the national average, then decide whether a modestly lower rate is worth waiting for or worth protecting now.

Sources

- [1]cbsnews.com

- [2]freddiemac.com

- [3]federalreserve.gov

- [4]bls.gov

- [5]nar.realtor