US News

Older Americans rely on home equity as housing costs rise

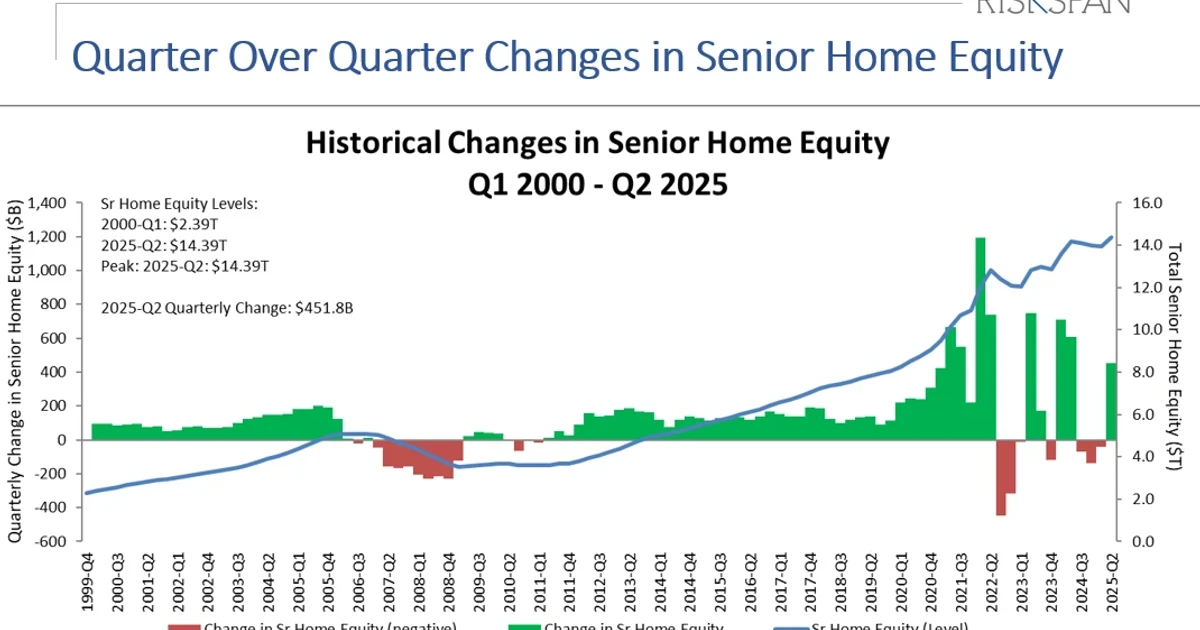

The National Reverse Mortgage Lenders Association put housing wealth held by homeowners age 62 and older at a record $14.18 trillion in the second quarter of 2024. At the same time, younger buyers are being priced out, making the same house both a shelter and a financial asset in a tightening national economy.

Housing has become a balance sheet problem

The U.S. is getting older, and the housing system is not adjusting quickly enough. The U.S. Census Bureau put the median age at 39.1 in July 2024 and projects that older adults will catch up to and eventually outnumber children in the coming years. More households are entering retirement with home equity as their largest store of wealth, while more renters and first-time buyers are shut out by high prices and borrowing costs.

Harvard’s Joint Center for Housing Studies found in 2024 that millions of potential homebuyers were priced out by elevated home prices and interest rates, while renters faced cost burdens at an all-time high. In practical terms, the market is forcing younger households to delay ownership and pushing older households to stay put longer than planned.

Older adults want to age in place, but the market makes that harder

AARP’s 2024 Home and Community Preferences Survey found that 75% of adults age 50 and older want to remain in their current homes as they age, and 73% want to stay in their communities. That preference is deeply rooted in economics as well as sentiment: moving can mean higher monthly costs, fewer available homes that fit mobility needs, and less certainty about what a sale will net after transaction costs and a new purchase.

For senior households, many of whom live on fixed incomes, the problem combines affordability, accessibility, and availability. The Urban Institute’s 2025 research found that severely cost-burdened senior households nearly doubled over two decades, rising from 5.2 million to nearly 11.7 million. Among households headed by someone age 50 or older, the share that was severely cost burdened climbed from 11.5% in 2000 to more than 16% by 2020.

The number of older adults experiencing homelessness increased 37% between 2019 and 2022, the Urban Institute found.

Home equity is the reserve many retirees are counting on

For many older owners, the house is still the main retirement backstop. In February 2024, Fannie Mae put the homeownership rate among adults age 60 and older at nearly 80%. In the same research, 72% of older homeowners were confident they would have enough income during retirement, yet only 15% would consider using home equity for extra retirement funds.

Older Americans often see their home as a reserve, but they do not necessarily want to draw it down unless they have to. Fannie Mae found that in 2022, Americans age 60 and older made up 29% of the adult population but 44% of homeowners. Fannie Mae projected that, if current patterns continue, that group could approach nearly half of all homeowners within a decade.

The Social Security Administration estimated the average monthly retirement benefit at $2,071 for January 2026. That check helps, but it leaves limited room for rent, property taxes, repairs, insurance, medical bills, and the costs of caregiving or long-term care.

Record wealth does not eliminate retirement risk

The National Reverse Mortgage Lenders Association put housing wealth held by homeowners age 62 and older at $13.19 trillion in the first quarter of 2024, and more than 1.3 million households have used FHA-insured reverse mortgages to access that wealth.

But housing wealth is not the same as spendable cash. Older sellers can receive less than expected when they actually sell, creating a possible shortfall just when they need money for retirement, downsizing, assisted living, caregiving, or long-term care costs.

Policy is now about more than construction

The underlying problem is no longer just how many homes get built. It is whether the housing market can support aging in place, provide realistic downsizing options, and let owners use equity without exposing themselves to a financial shock later. In Whose Housing Crisis?, Nick Gallent argues that housing’s social purpose as a home is increasingly being overtaken by its economic function as an asset, a hedge against weaker pensions, or a source of equity release.

Sources

- [1]nytimes.com

- [2]fanniemae.com

- [3]jchs.harvard.edu

- [4]urban.org

- [5]aarp.org

- [6]nrmlaonline.org

- [7]academic.oup.com

- [8]ssa.gov

- [9]census.gov