Business

Retirement happiness depends on purpose, not just savings balances

A bigger nest egg does not automatically buy a better retirement. The real planning test is how you will spend your days, because housing, health care, work, travel and caregiving choices can change the income you need as much as your account balance does. Recent surveys show many Americans sense that shift, even if their plans have not caught up.

Confidence is still uneven

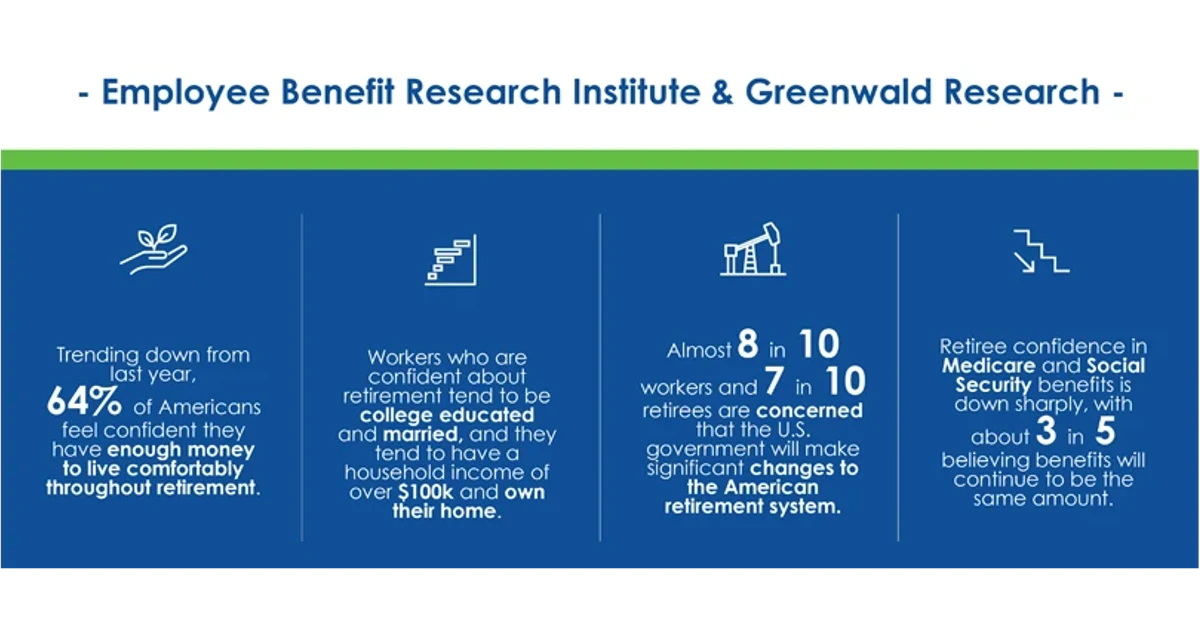

The 34th annual Retirement Confidence Survey, fielded in 2024 by Employee Benefit Research Institute and Greenwald Research, found that worker and retiree confidence had not fully recovered from the prior year’s drop, even though majorities still said they felt optimistic about retirement prospects. That gap matters because confidence often shapes behavior long before the last paycheck arrives.

A separate 2024 national opinion poll from the National Institute on Retirement Security found working-age Americans increasingly worried about retirement, and many of them see a return to pensions as part of the answer. That is a telling signal about the direction of anxiety: people are not just worried about market swings, they are worried about whether their retirement income will be predictable enough to support a real life after work.

The missing step is turning savings into income

One of the biggest planning blind spots is not accumulation, but decumulation. Allianz Life said in October 2024 that less than half of Americans, 44%, currently have a plan for how they will draw from retirement savings to create retirement income. That is a crucial distinction, because a balance can look healthy on paper and still fail if withdrawals, taxes, spending spikes or longevity are not mapped out in advance.

Employee Benefit Research Institute’s 2024 Spending in Retirement Survey helps explain why that transition matters. The third Spending in Retirement study, fielded during the summer of 2024, surveyed roughly 3,600 American retirees ages 62 to 75 to examine how spending patterns and retirement well-being have changed since retirement. The design itself reflects the right question: retirement readiness is not only about how much money was saved, but how spending evolves once the paychecks stop.

Purpose and emotional readiness belong in the budget

The Financial Planning Association’s 2024 work on retirement preparation identified emotional readiness and health expenses as key issues. That framing is important because retirement pressure is not purely mathematical. If the plan ignores identity, routine, social connection and health, the budget may be accurate while the life is not.

MassMutual’s 2024 Retirement Happiness Study adds a concrete behavioral pattern to that idea. Happier retirees tend to be more active, exercise more, pursue hobbies and spend more time with loved ones. Another research finding cited in coverage put numbers on the role of purpose: 97% of retirees with a strong sense of purpose reported happiness, compared with 76% of those without it. The implication is clear. Purpose is not a soft extra layered on top of finances; it is one of the variables that shapes whether retirement feels rich or empty.

How lifestyle choices change the number you need

The smartest retirement plan starts by pricing the life you actually want. A person who keeps a large home, travels often, helps adult children, or expects to provide care for a spouse or parent will face a very different spending pattern from someone who downsizes, stays local and lives quietly. The same is true for work: part-time consulting, seasonal work or a phased exit can reduce pressure on savings, while a clean stop from paid work requires a larger income cushion.

A practical retirement budget should separate the major choices that drive spending:

• Housing: staying put, downsizing or moving closer to family changes housing costs, maintenance needs and the likelihood of paid help around the house.

• Health: the Financial Planning Association flagged health expenses as a core retirement issue, and those costs can rise quickly with premiums, prescriptions, out-of-pocket care and support needs.

• Work: any continued earnings can reduce the amount you must pull from savings, but only if you plan that income realistically.

• Travel: frequent trips, seasonal moves or family visits can make a large difference in annual spending.

• Caregiving: helping others, or needing help yourself, can become one of the biggest and least predictable cost categories.

This is why the most useful retirement number is not a single target balance. It is a spending plan built around the way you want to live, with a backup plan for the way life actually changes. The surveys are pointing in the same direction: confidence, income strategy, emotional readiness and purpose all belong in the same conversation, because retirement happiness depends on how well the money supports the life you intend to build.

Sources

- [1]nytimes.com

- [2]ebri.org

- [3]greenwaldresearch.com

- [4]nirsonline.org

- [5]allianzlife.com

- [6]financialplanningassociation.org

- [7]massmutual.com

- [8]kiplinger.com

- [9]soa.org