Business

Social Security income can qualify retirees for mortgages, Fannie Mae says

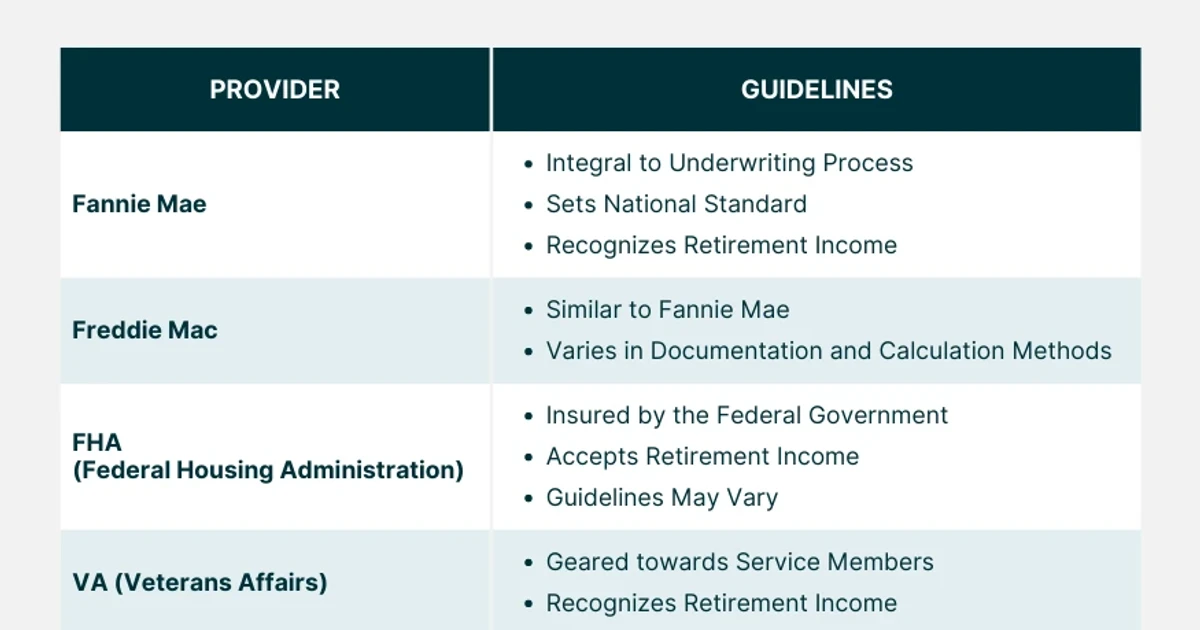

A fixed retirement check is not automatically a dead end in mortgage underwriting. Fannie Mae says Social Security retirement income can count as qualifying income, which means a retiree may be able to borrow against home equity if the income is documented, the debt load is manageable, and the loan still makes sense after the monthly payment is added.

That reality matters because many older homeowners are living on income that is steady, but not large. The estimated average monthly Social Security retirement benefit was $2,071 in January 2026, enough to support some borrowers on paper, but not enough to excuse weak credit, thin equity, or an already strained budget. The central question is less about whether Social Security counts and more about whether the rest of the file can survive underwriting.

How lenders count Social Security income

Fannie Mae’s rules are more flexible than many retirees assume. Social Security retirement income may be documented with an SSA award letter, an SSA-1099, recent signed federal income tax returns or tax transcripts, or proof of current receipt. Fannie Mae also says no minimum income history is required for Social Security income, which is important for borrowers whose benefit is newly claimed or recently re-documented.

That does not mean the income gets an automatic pass. Under Fannie Mae’s general income rules, lenders still need to show that the income is stable and predictable. If a source has a defined expiration date or is limited, the lender must document that it is expected to continue for at least three years from the note date. For retirees, that rule turns Social Security from a retirement benefit into an underwriting question: will the payment keep coming long enough to support the debt being taken on now?

Fannie Mae also notes that a borrower may sometimes qualify using benefits drawn from a spouse’s, ex-spouse’s, dependent parent’s, or dependent child’s record. That can matter in households where the borrower’s own work history is thin, but the Social Security record tied to the household is stronger. In practical terms, the paperwork trail matters as much as the benefit amount.

What home equity lenders actually look at

For a home equity loan or a HELOC, income is only one piece of the decision. Lenders typically review debt-to-income ratio, credit score, equity position, and supporting documents such as bank statements, tax returns, and proof of income. In many 2026 lender guides, a debt-to-income ratio around 43% or lower remains a common benchmark, although some lenders will go higher when a borrower has strong credit and substantial equity.

That underwriting framework is what makes retirement borrowing a reality check. A homeowner with a modest Social Security benefit may still qualify if housing costs are low, other debts are limited, and the home has enough tappable equity. But the same fixed income that can help qualify for a loan can also make repayment more fragile, especially if the loan adds a new monthly bill that did not exist before.

The Consumer Financial Protection Bureau describes a HELOC as a loan secured by the home that lets a borrower borrow, spend, and repay as needed. Regulation Z applies to open-end credit plans secured by a consumer’s dwelling, which means lenders must follow disclosure and underwriting rules that are designed to make the terms more transparent. That structure can make a HELOC useful for irregular expenses, but it also means the payment can change as the balance changes, which is not always ideal for a retiree living on fixed income.

When tapping equity helps, and when it hurts

Home equity borrowing can solve a cash-flow problem when it replaces more expensive debt, covers a one-time repair, or creates a buffer for a temporary strain. It can also be a rational move if the borrower has ample equity, enough residual income after the payment, and a clear plan to repay. In that case, borrowing against the home can convert illiquid housing wealth into usable cash without forcing a sale.

But the tradeoff is real. Interest costs add up, and the home becomes collateral. If the borrower cannot keep up with the payment on a home equity loan or a HELOC, the lender can foreclose. That risk is especially serious for retirees, because a loan that looks manageable on the first month can become harder to sustain after medical bills, inflation, insurance increases, or other living costs rise.

That is why the decision should be framed as a balance sheet test, not a comfort test. A retiree may feel “house rich,” but the lender is looking for monthly capacity. If the borrowing adds pressure to a tight budget, equity extraction can solve today’s problem by creating a larger one later.

The reverse-mortgage alternative

For some older homeowners, the federally insured alternative is the Home Equity Conversion Mortgage, or HECM. The U.S. Department of Housing and Urban Development says the HECM is the only federally insured reverse mortgage and is available only to seniors. HUD says it is designed to let eligible homeowners tap home equity for living expenses, maintenance, or repairs.

The key difference is repayment timing. HUD says HECM borrowers may remain in the home indefinitely as long as property taxes and homeowners insurance stay current. That can make a reverse mortgage easier on monthly cash flow than a traditional home equity loan or HELOC, because the loan is structured around the home’s value rather than a monthly principal-and-interest payment in the usual sense.

The HECM still carries important obligations, though. HUD requires counseling, and it maintains a counselor roster for borrowers who need help evaluating whether a reverse mortgage fits their situation. That counseling step is not a formality; it is a safeguard for a product that can preserve cash flow but also reduce home equity over time.

Why the policy backdrop matters

The federal rules around retirement and disability income point in the same direction: lenders should evaluate the real stability of income, not assume Social Security disqualifies a borrower. The Consumer Financial Protection Bureau has warned lenders against imposing unnecessary burdens on consumers receiving Social Security disability income, reinforcing the broader principle that public benefits can be legitimate qualifying income when properly documented.

That policy stance matters in 2026 because many older borrowers are navigating a narrow path between liquidity and leverage. Social Security income may be enough to pass underwriting, but passing underwriting is not the same as making a wise borrowing choice. The better fit is usually the loan that leaves room in the monthly budget, protects against default risk, and matches the borrower’s expected time in the home.

For retirees, the takeaway is straightforward: Social Security income can open the door, but the loan still has to survive the rest of the test. Strong equity, manageable debt, documented income, and a realistic repayment plan are what turn a home from a source of stress into a source of flexibility.

Sources

- [1]cbsnews.com

- [2]selling-guide.fanniemae.com

- [3]ssa.gov

- [4]consumerfinance.gov

- [5]files.consumerfinance.gov

- [6]hud.gov

- [7]entp.hud.gov

- [8]bankrate.com