Business

SpaceX IPO sparks index inclusion worries for investors

SpaceX’s public debut is not just a capital-raising event. It is a stress test for who gets paid first when a mega-cap private company finally enters public markets, and for how quickly passive investors are forced to follow. SpaceX planned to sell 555,555,555 Class A shares at $135 each, while a Senate Banking Committee letter warned that recent index rule changes could raise risks for retail investors and retirement savers.

Insiders and early backers take the first windfall

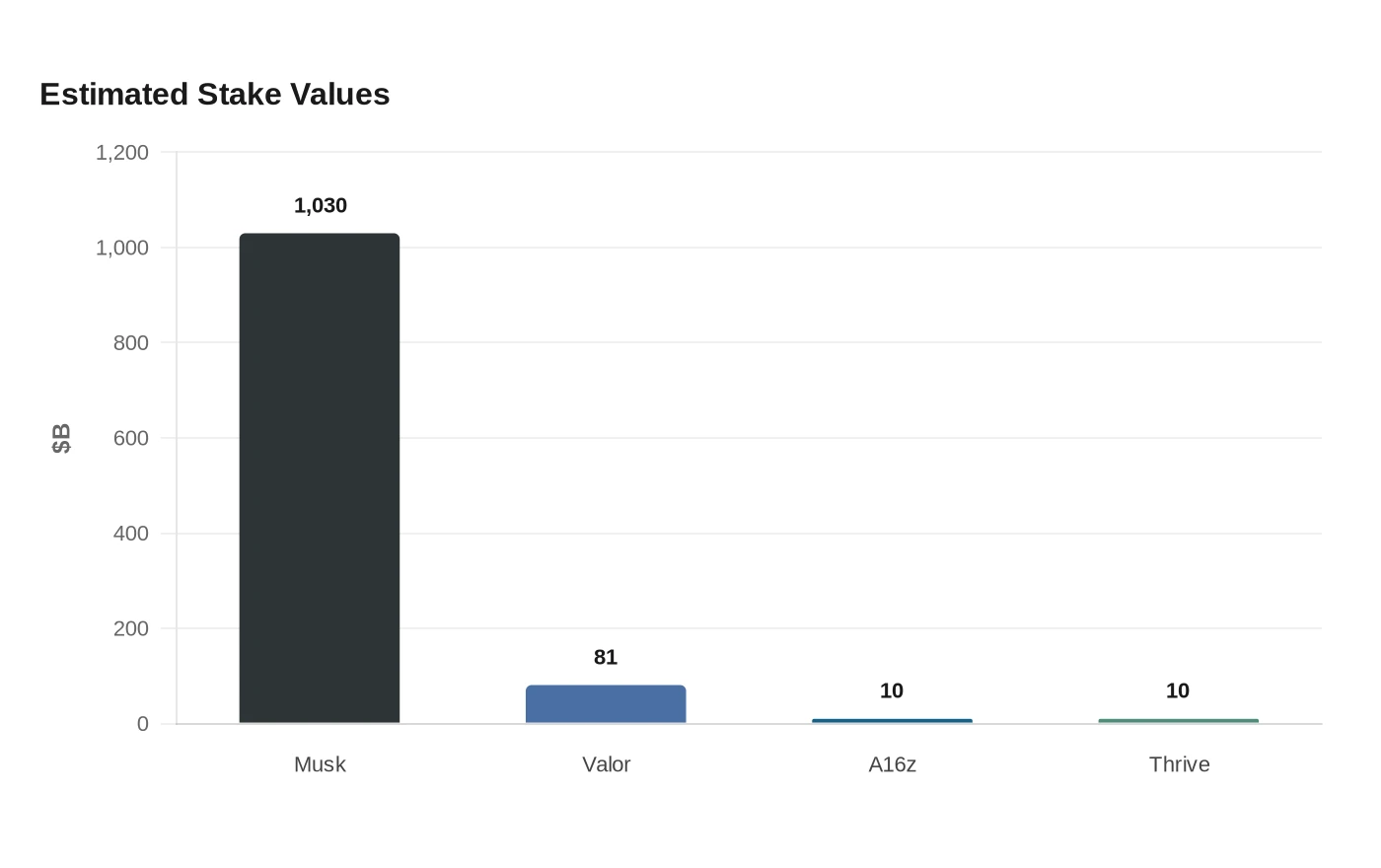

The first gains flow to the people who owned SpaceX long before the stock became a public ticker. PitchBook estimated Elon Musk’s stake at about $1.03 trillion after the first day of trading, with Musk still controlling more than 80% of the voting power. The same report put Valor Equity Partners’ stake at $81 billion, Founders Fund at more than $50 billion, DFJ Growth at more than $20 billion, Sequoia at more than $20 billion, Andreessen Horowitz at roughly $10 billion, and Thrive Capital at around $10 billion.

That payoff extends well beyond the headline names. Observer reported that Gwynne Shotwell, SpaceX’s president and chief operating officer, owned 12.6 million shares and could see her stake approach nearly $3 billion at a $2 trillion valuation, while Bret Johnsen, the chief financial officer, owned about 9.6 million shares that could be worth $1.4 billion. Forbes also highlighted Luke Nosek, a SpaceX board member and longtime Musk ally, as a billionaire on paper, underscoring that the company’s wealth is concentrated in a narrow inner circle that has been in place for years.

Institutional demand does not mean equal access

The biggest outside checks are being written by institutions that already sit closest to the IPO allocation process. Bloomberg reported that BlackRock was targeting about $5 billion in SpaceX shares, while other market reports said several institutional investors submitted orders of roughly $10 billion or more each and that retail demand surpassed $70 billion. CNBC also reported that SpaceX reserved up to 30% of the IPO for retail buyers, far above the typical 5% to 10%, but that still leaves underwriters deciding where the rest of the stock lands.

That structure matters because it separates access from performance. Fidelity said the offering was available to customers with at least $2,000 in a retail brokerage account and listed broker platforms including Charles Schwab, Robinhood, SoFi and E-Trade, but it also cautioned that final allocation depends on demand and can be limited. In practical terms, that means the first layer of ownership is shaped by anchor orders, underwriting relationships and brokerage channels, not by a level playing field.

Index rules determine when passive money arrives

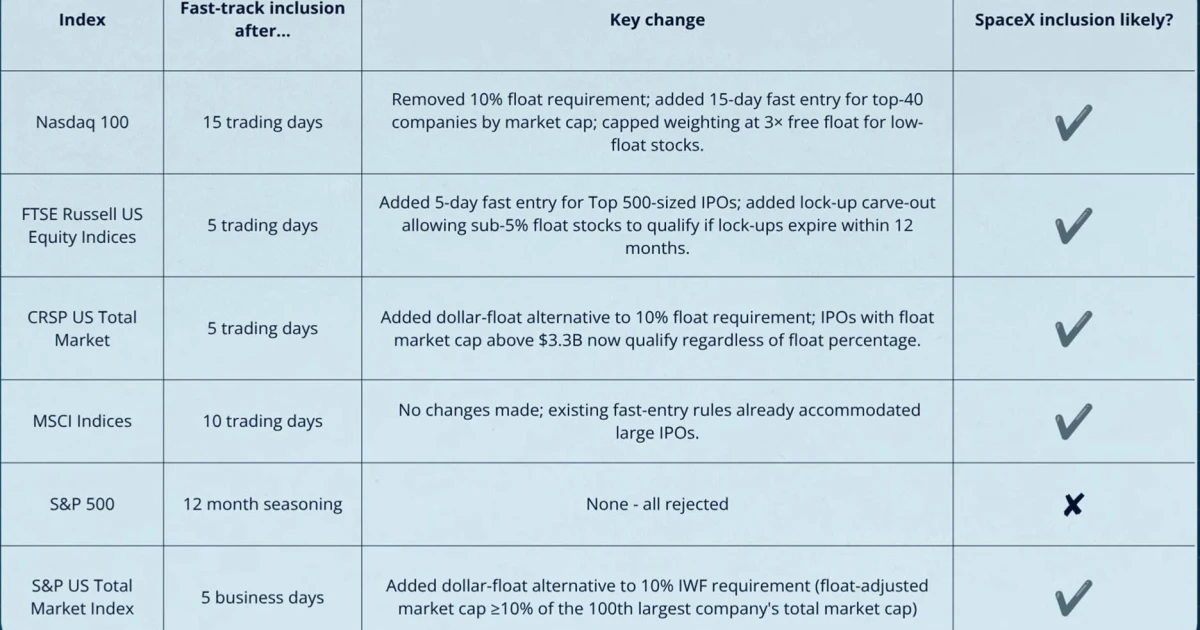

The biggest long-run controversy is not the IPO itself. It is when index funds are allowed, or forced, to buy. MSCI said SpaceX would be added to its standard and large-cap indexes effective June 29, 2026, after a fast-track process that can be announced no earlier than the first trading day and no later than before the third trading day. MSCI’s early-inclusion rules waive the usual length-of-trading and liquidity screens, but still require large-cap thresholds based on full market capitalization and free-float-adjusted market capitalization.

That fast track is exactly what critics worry about. If a company with a huge valuation and a small free float enters index baskets quickly, passive funds must buy according to benchmark rules, even if much of the upside has already been captured by the original owners. MSCI’s own modeling suggests the effect can still be modest at the index level, but the flow of money is real, and it arrives only after the listing mechanics are already set.

S&P is holding the line, at least for now

S&P Dow Jones Indices took a different path. After consulting on whether to change its rules for mega-cap companies, it said it would make no changes to the eligibility criteria for the S&P 500, S&P MidCap 400 or S&P SmallCap 600, including financial viability screens, seasoning periods and minimum float requirements. S&P said exceptions should not be granted solely because a company is large, which means SpaceX is not getting a shortcut into the S&P 500.

That does not mean passive investors are insulated. S&P’s own clarification says the S&P Total Market Index and the S&P Composite 1500 have no financial viability requirement. In other words, even if the S&P 500 keeps SpaceX out, broad-market funds can still absorb it through other S&P-linked benchmarks that sit inside retirement portfolios.

Nasdaq-100 is the pressure point for benchmark design

Nasdaq updated its Nasdaq-100 methodology on May 1, 2026, saying public markets now feature companies that stay private longer, list at larger scale and arrive with lower public floats. The benchmark is designed to track 100 of the largest Nasdaq-listed non-financial companies, and Nasdaq framed the update as a way to keep the index investable as ownership structures change.

Coverage around the IPO says SpaceX is expected to be fast-tracked into the Nasdaq-100, which is why the exchange’s rule shift matters so much to fundholders. If that happens, index-tracking products tied to the Nasdaq-100 will need to buy SpaceX on the benchmark’s timetable, not on the timetable of ordinary investors who are still deciding whether they are comfortable paying a post-listing price.

What retirement savers should watch next

For retirement savers, the key issue is sequencing. Fidelity noted that investors who miss the IPO can buy after the stock begins trading, but MSCI’s June 29 inclusion and Nasdaq’s benchmark changes mean the earliest gains are likely to accrue to the IPO recipients, anchor funds and first-day traders, while 401(k) exposure arrives later through passive replication. That is the core market-structure concern: broad retirement money can become the exit path for stock that was already re-priced by insiders and institutions.

MSCI’s own simulation suggests the effect on a broad index may be smaller than the rhetoric around the IPO implies. Even at a 25% float assumption, SpaceX’s simulated weight in the MSCI USA Index reached only 58 basis points, limiting its annualized contribution to 12 basis points during the study period even as SpaceX’s annualized return ran near 90%. The lesson is not that passive funds are harmless or dangerous in the abstract; it is that the mechanics of index construction determine who gets access first, who bears the timing risk, and who ends up buying after the headline gains have already been booked.