Business

Start-ups bet on geothermal energy as costs and risks remain high

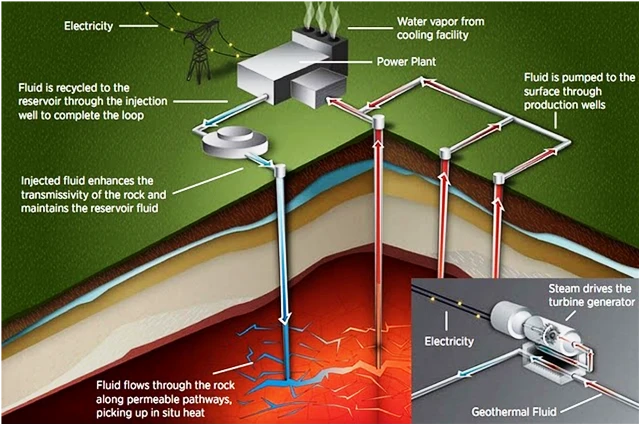

Drilling and well costs can account for as much as 80% of a geothermal project's total cost, the basic reason the technology has stayed a niche for more than a century. Start-ups are now trying to change that with new drilling and engineering methods, and the pitch is simple: if the wells can be drilled faster, deeper and with less risk, geothermal can sell round-the-clock power that competes on reliability as much as on price.

Why geothermal is back on investors’ radar

Geothermal still meets less than 1% of global energy demand, yet the IEA projects next-generation geothermal could supply up to 15% of global electricity demand growth by 2050 if project costs keep falling. That would translate into as much as 800 GW of capacity and about 6,000 TWh a year.

The resource has another advantage that investors and utilities understand immediately: it runs continuously. In IEA data, average global geothermal capacity factor was over 75% in 2023, compared with less than 30% for wind and less than 15% for solar PV. That makes geothermal especially valuable in markets that need firm power for data centers, heavy industry and grids already strained by variable renewables.

The economics are still dominated by drilling

For all the promise, geothermal remains a capital-intensive business. Even a good reservoir does not guarantee a good project if the wells are expensive, slow or unsuccessful. That cost structure is why developers talk less about generation equipment than about subsurface risk, drilling speed and the ability to repeat successful wells at scale.

The technical frontier is also moving deeper. New drilling technologies are pushing geothermal beyond 3 km depth in nearly all countries, and the IEA says thermal resources below 8 km could support almost 600 TW of capacity over a 25-year operating life. That is a huge theoretical resource, but it comes with real-world hurdles: project-development risk, permitting delays, environmental concerns and questions about social acceptance still slow projects before they ever reach commercial operation.

This is where oil-and-gas expertise becomes relevant. Horizontal drilling, hydraulic fracturing, subsurface mapping and large-scale project management are all transferable skills, and geothermal start-ups are leaning on that overlap. The U.S. Department of Energy calls enhanced geothermal systems, or human-made geothermal energy, the next frontier for deployment. The industry’s growth now depends on engineering the reservoir rather than waiting for the right geology to appear at the surface.

Big tech is helping finance the first wave

The newest demand signal is coming from artificial intelligence and data centers, where operators want dependable power that does not fluctuate with the weather. In December 2024, interest from companies such as Meta and Google was already pulling geothermal start-ups into the conversation about how to power rising data-center loads. A large technology customer can give a project a bankable offtake agreement, which improves financing and reduces the risk that a plant is built without a buyer.

The sector has expanded quickly. A December 2024 Reuters tally counted more than 60 geothermal start-ups that had emerged since 2022 and about $700 million in financing over that period. Fervo Energy has become the clearest example of how the market is trying to scale: it raised $462 million in a Series E round in December 2025, with investors including Google and Breakthrough Energy Ventures.

Fervo’s commercial progress also shows why first customers matter. Google committed to buy 115 MW from Fervo to help power its Nevada data centers after Fervo delivered 3.5 MW from a demonstration plant to a nearby Google data center in 2023. That kind of sequence, from pilot output to an anchor contract, is what turns a promising concept into a project finance story. It does not eliminate the technical risk, but it helps answer the more immediate question of whether a well can support revenue before the capital stack collapses.

What still has to change for geothermal to compete at scale

The policy agenda is now centered on reducing uncertainty. Better geothermal data, more research and development, more demonstration projects, stronger workforce training and international technical standards would address environmental concerns. Those are the ingredients that lower financing costs, shorten development timelines and make it easier for banks and utilities to compare geothermal with gas, solar plus storage, or transmission upgrades.

The U.S. market shows how broad the opportunity could be. The sector has grown steadily since 2020, and the 2025 U.S. geothermal market update now includes geothermal heat pumps in its market analysis. The commercial future of geothermal may not rest only on power plants. Heating and cooling markets can provide a steadier near-term revenue base, and they may expand faster than deep power projects if drilling costs remain high.

Sources

- [1]bbc.co.uk

- [2]iea.org

- [3]energy.gov

- [4]inc.com

- [5]datacenterdynamics.com

- [6]nlr.gov