Business

Target shareholders reject split of chair and CEO roles again

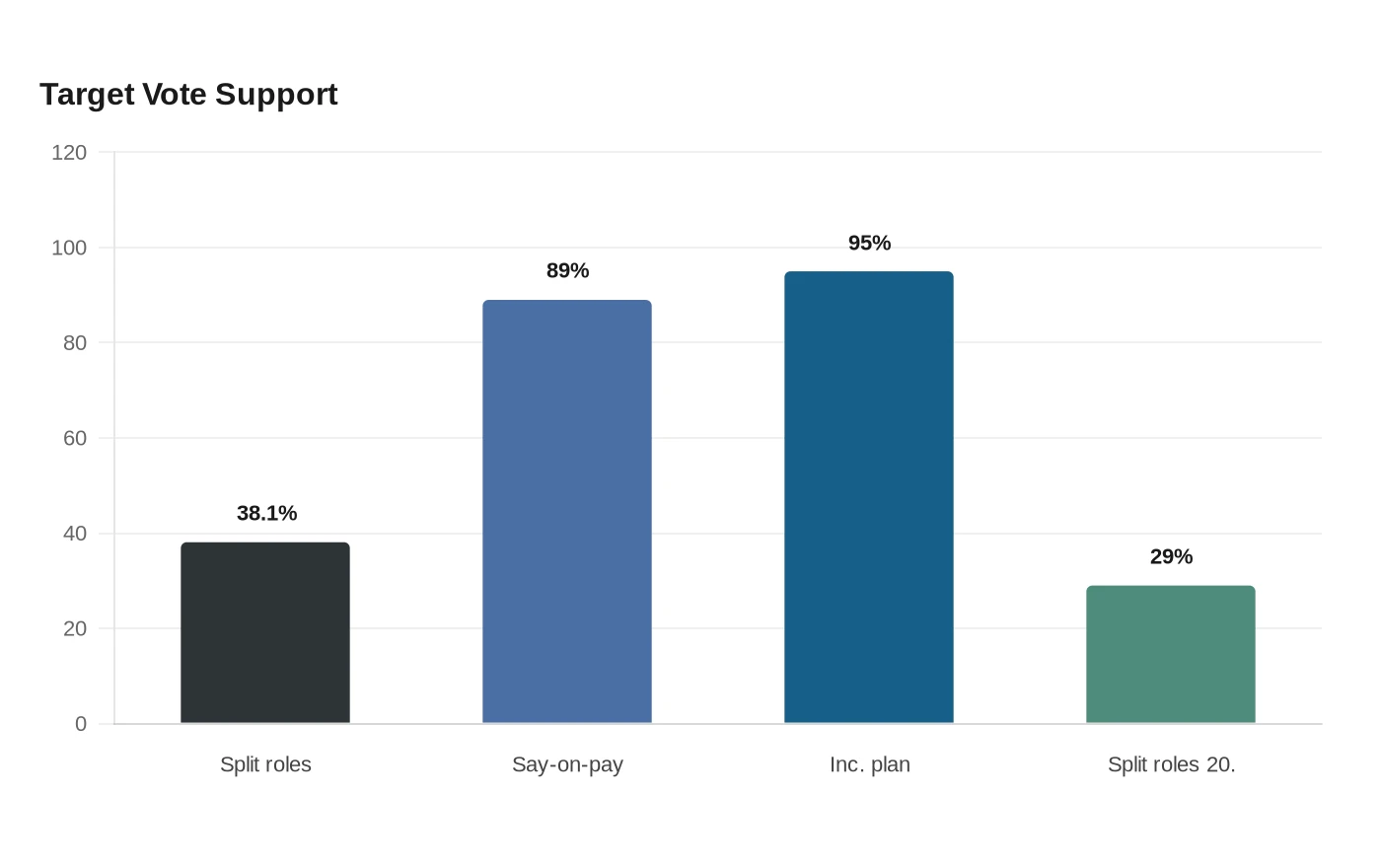

Target shareholders again stopped short of forcing a split between the board chair and chief executive jobs, giving Brian Cornell a fresh win even as dissent over the company’s governance structure kept building. The proposal to separate the roles drew 38.1% support, up from 29% for a similar measure in 2024, but it still fell well short of passage.

The vote, certified by The Carideo Group after Target’s 2026 Annual Meeting of Shareholders on June 10, showed 392,543,988 shares were cast, equal to about 86.4% of the company’s outstanding stock as of the record date. All 12 director nominees were elected, including Cornell, Michael J. Fiddelke, Stephen B. Bratspies and John R. Hoke III, while the board also retained the backing needed to keep its broader governance slate intact.

The result points to a familiar tension in Target’s investor base: shareholders are willing to register dissatisfaction, but not enough of them are ready to trigger a structural overhaul. Target has lost roughly half its market value since 2021, a stark sign of how badly the retailer’s execution has been tested by merchandising missteps, inflation-weary consumers and fierce competition from Walmart and Costco. Yet the latest vote suggests that many investors still prefer to give management more time than to force a new governance model.

That patience comes as Target is trying to reset its growth strategy with a heavier investment push. In March, the company said it would make an incremental $2 billion investment in 2026, including more than $1 billion in additional capital expenditures and $1 billion in additional operating investment, bringing total 2026 capital investment to about $5 billion. Target said the plan would touch every store more than in any year of the last decade, with spending aimed at store refreshes, payroll and training, technology and AI-driven shopping improvements.

Shareholders also backed the rest of the company’s agenda. They approved an advisory say-on-pay vote with 89.0% support, ratified Ernst & Young LLP as Target’s independent registered public accounting firm for fiscal 2026, and approved the amended and restated 2020 long-term incentive plan with 95.0% support. Other shareholder proposals, including measures on pesticide disclosures and microfiber shedding, failed to win approval.

Target’s proxy statement said the board had completed a deliberate CEO succession process and argued that Fiddelke’s experience across merchandising, finance, operations and human resources made him the right leader for the next chapter. The board also welcomed two new independent directors, Stephen Bratspies and John Hoke III, after Douglas Baker and Grace Puma did not seek re-election and Donald Knauss retired under tenure policies. The latest vote showed investors are still pressing harder, but not yet enough to break Target’s combined leadership structure.