Business

Top 5-year CDs still near 4%, far above national average

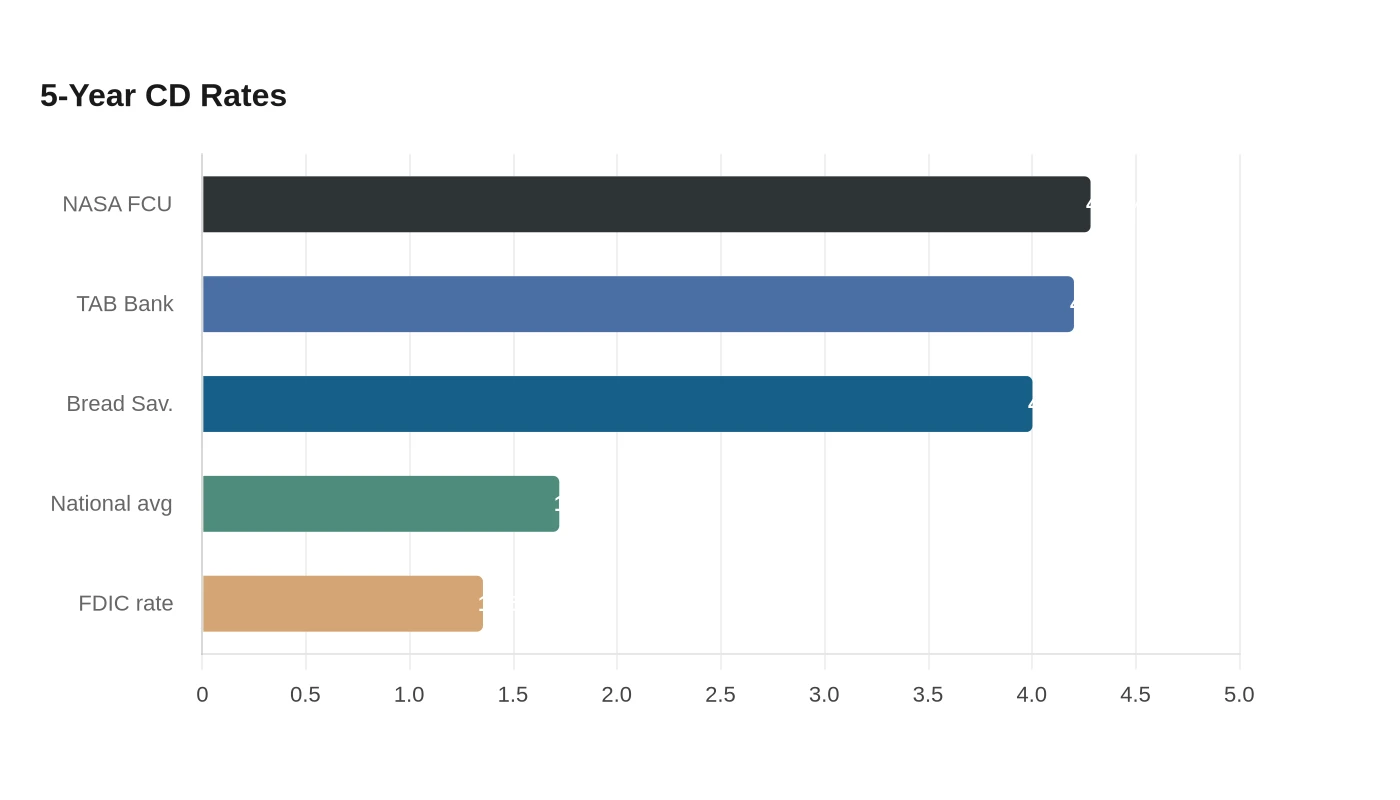

Five-year CDs are still paying about 4% at the top end, but the national average is only 1.72% APY, and the FDIC’s June 2026 national rate for 60-month CDs under $100 million is 1.35241%. NerdWallet lists NASA Federal Credit Union’s 5-year certificate at 4.28% APY, TAB Bank’s 5-year CD at 4.20% APY and Bread Savings at 4.00% APY, with the best long-term offers typically found at online banks and credit unions. CDs also come with fixed APYs, and deposits at FDIC-insured banks and NCUA-insured credit unions are protected up to applicable limits.

At a 22% federal marginal tax rate and May’s 4.2% inflation reading, a $15,000 deposit in NASA Federal Credit Union’s 60-month certificate would grow to $18,496.79 before tax, $17,727.50 after federal tax, and $14,431.41 in today’s dollars. A $15,000 five-year Treasury yielding 4.24% would end at $17,699.85 after federal tax and $14,408.90 after inflation, while a top high-yield savings account at 4.15% would finish at $17,637.79 after tax and $14,358.38 in real terms. Treasury interest is taxable at the federal level but exempt from state and local income taxes, which can improve the after-tax result for savers in taxable states.

Shorter-term CDs do not change the picture much on today’s averages. Bankrate puts the national average at 2.00% APY for one-year CDs and 1.67% APY for three-year CDs as of July 6, 2026. At those rates, the same $15,000 would end the one-year term at $15,234.00 after tax and $14,619.96 in today’s dollars, or the three-year term at $15,596.01 after tax and $13,785.12 in today’s dollars.

That gap is why the long-term lock still matters: the best CDs are holding near 4% even as the average 60-month rate sits far lower, and the rate stays fixed through maturity. For savers who may need cash flexibility, a Treasury or a high-yield savings account gives access without the same commitment, but for anyone who wants to lock in today’s yield before the next shift in deposit pricing, the headline APY is only part of the story. The real test is whether a fixed rate now beats the cost of giving up liquidity later.

Sources

- [1]cbsnews.com

- [2]nerdwallet.com

- [3]bankrate.com

- [4]fdic.gov

- [5]fred.stlouisfed.org

- [6]thesheffieldpress.com