Business

Warsh signals hawkish Fed shift, markets brace for higher rates

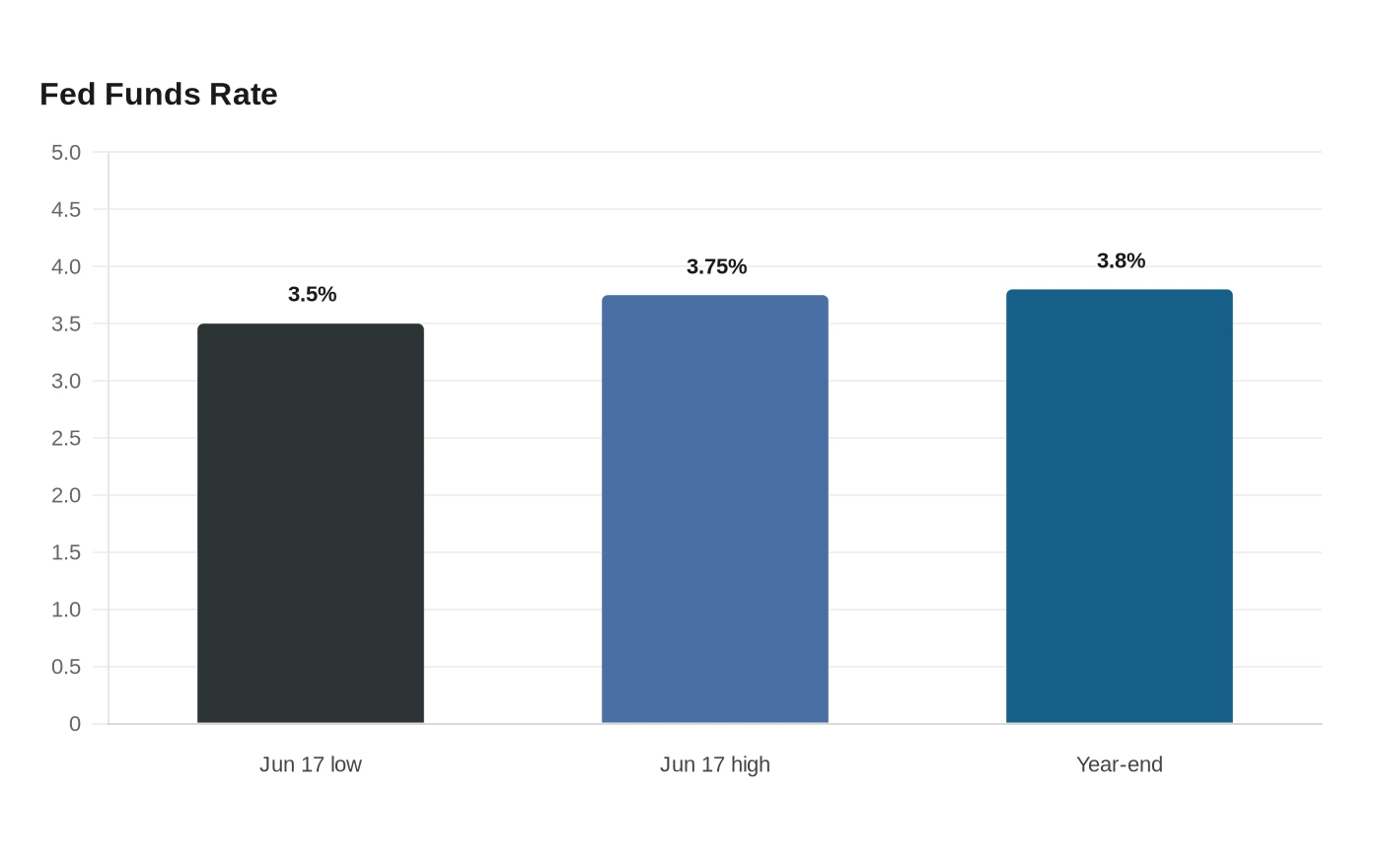

Kevin Warsh’s first Federal Open Market Committee meeting as Fed chair ended with no change in rates, but the signal to households and markets was anything but neutral. The central bank kept its benchmark federal funds rate in a range of 3.5% to 3.75% on June 17 in a unanimous 12-0 vote, yet the post-meeting statement was shorter and stripped of language that had hinted at future cuts.

That change in tone matters because it affects the borrowing costs people actually feel. A Fed that sounds less inclined to ease policy can keep pressure on mortgage rates, auto loans, credit cards and business lending even when the target rate itself stays put. Investors quickly treated the meeting as a pivot toward a more hawkish stance, reading the message as a warning that rates could stay higher for longer, or even move up.

Warsh reinforced that interpretation in his first press conference by announcing five task forces to review Fed communications, balance sheet policy, data sources, productivity and jobs, and the inflation framework. He said the groups would include both Fed staff and outside experts, and he declined to submit his own forecasts for the Summary of Economic Projections. That combination points to a central bank that wants to say less, lean more heavily on incoming data, and give markets fewer clues about its next move.

The market response was immediate. The 2-year Treasury yield, the part of the curve most sensitive to expectations for the fed funds rate, rose after the meeting, while the 10-year yield eased to 4.453% and the 30-year yield fell to 4.90%. The dollar also climbed to a one-year high as traders priced in higher U.S. interest rates. Reuters reported that officials were split between no cuts in 2026 and one or more hikes, and other coverage said the median projection pointed to a 3.8% fed funds rate by year-end, implying at least one increase from the current range.

For households, that means relief on borrowing costs may take longer to arrive. For businesses, it raises the hurdle for investment and refinancing. For retirement portfolios, higher yields can pressure existing bond prices even as new fixed-income investments become more attractive. The Fed still held the line on rates, but Warsh’s early message suggested the policy debate has shifted from when cuts begin to whether the next move could be up.

Sources

- [1]news.google.com

- [2]federalreserve.gov

- [3]cnbc.com

- [4]finance.yahoo.com