Business

Why you should avoid low-yield savings accounts right now

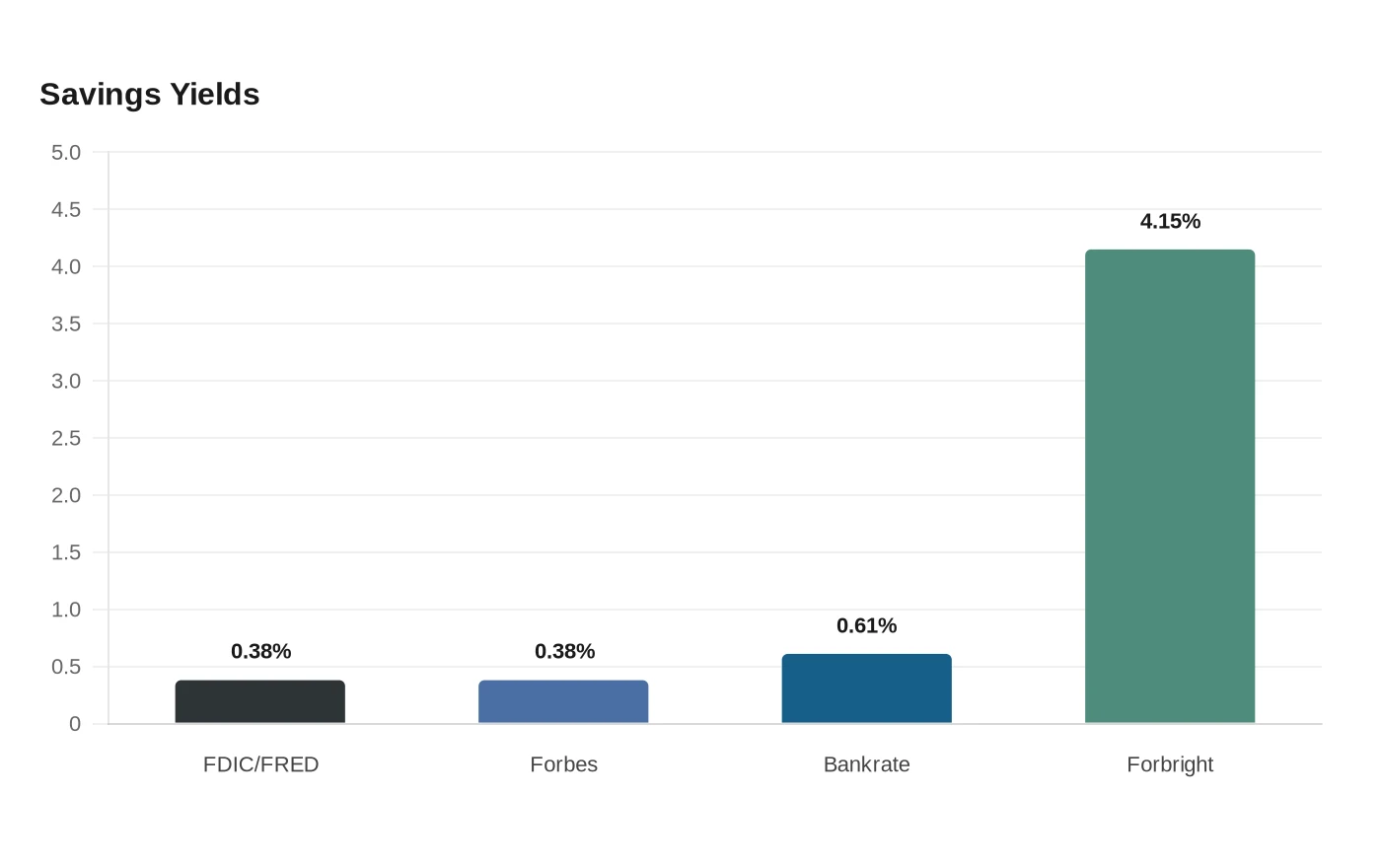

The savings account to avoid right now is the one that still pays close to the national average. The Federal Reserve left its benchmark rate at 3.50% to 3.75% on June 17, 2026, but the typical U.S. savings account is still yielding only 0.38% APY, far below the 4.15% to 5.00% APY available in top high-yield accounts. That spread can leave hundreds of dollars a year on the table for households that keep cash parked in the wrong place.

The account to avoid: the plain savings account that hugs the average

The account that deserves the most scrutiny is the standard savings account at a big bank or other institution that pays near the national average. FDIC data compiled in FRED show a June 2026 savings rate of 0.38%, and the FDIC says its national rate is a weighted average of rates paid by insured depository institutions and credit unions, with each institution weighted by its share of domestic deposits. That structure helps explain why a lot of ordinary accounts still pay very little even when headline interest rates are elevated.

Different rate trackers can land on slightly different numbers, but they point in the same direction. Bankrate put the national average savings yield at 0.61% as of June 18, 2026, while Forbes Advisor reported 0.38% as of June 15, 2026. Even with that higher Bankrate benchmark, the best available rate in its roundup was 4.15% from Forbright Bank, which the publication said is about six times the national average.

Insurance still matters, but it does not improve your return. Bankrate notes that its top high-yield accounts are offered by FDIC banks or NCUA credit unions, which means your cash can remain federally insured while still earning a much higher APY. The mistake is treating safety and yield as the same thing, when the real question is whether your money is safe and working hard enough.

Why the Fed pause matters, and why it is not enough

The Fed’s decision to hold the target range at 3.50% to 3.75% was unanimous, a 12-0 vote. That pause matters because it keeps the rate backdrop supportive for savers, which is one reason online banks and other high-yield accounts can still advertise strong yields right now. But the Fed does not set your account APY directly, and a bank that wants to keep deposits cheap can still pay far below the market leaders.

That is why this period is so awkward for cash holders. The broad rate environment is still relatively high, yet the national average savings rate remains stuck near 0.38%, which means many households are getting only a sliver of the income their balances could generate. If the Fed eventually cuts, those top yields can come down too, so the window to lock in a better savings rate is more valuable than it looks.

How much money a low-yield account can cost you

The difference is not abstract. On $10,000, the gap between 0.38% and 4.15% is about $377 a year, before taxes. On $25,000, moving from 0.38% to 5.00% means roughly $1,155 more in annual interest, again before taxes. That is the money many households leave on the table simply by keeping savings in an account that pays close to the average instead of a competitive high-yield rate.

For families building an emergency fund, paying for near-term expenses, or parking money between goals, that difference adds up quickly. A cash reserve should be liquid, but liquidity does not have to mean surrendering most of the interest income to a low-rate account. In a pause period like this, the opportunity cost is large enough to justify a review.

What to compare before you move your cash

Start with APY, but do not stop there. Bankrate says its best high-yield savings accounts pair higher yields with no fees and low minimum deposit requirements, while CNBC Select’s June 2026 comparison also weighs minimum deposit, monthly fee, withdrawal and transfer limits, and whether the account comes with an ATM card. Those details determine whether a headline rate is actually usable for your situation.

• Look for the highest APY you can actually qualify for, not just a teaser rate.

• Check monthly fees and the balance needed to waive them, since fees can erase the benefit of a better yield.

• Review minimum opening deposits. Forbes noted some high-yield offers can require a $10,000 minimum even when the rate looks attractive.

• Confirm the account is with a federally insured bank or credit union, so your cash keeps its protection while earning more.

• Pay attention to withdrawal and transfer rules, because access matters for emergency savings and short-term cash.

The practical takeaway

A Fed pause is not a reason to accept a bad savings rate. It is a reminder that the benchmark can stay elevated while your own account still earns almost nothing, which is why the low-yield savings account is the one to avoid now. Keep the insurance, keep the liquidity, but move the cash to the best rate you can get while the market still offers it.

Sources

- [1]cbsnews.com

- [2]federalreserve.gov

- [3]fred.stlouisfed.org

- [4]fdic.gov

- [5]bankrate.com

- [6]cnbc.com

- [7]forbes.com