World

Closing the Strait of Hormuz would shock global oil markets

Closing the Strait of Hormuz still carries the power to rattle crude prices, but the threat is less potent than it was when Iran could count on surprise and scarcity alone. The waterway between Oman and Iran carried about 20 million barrels a day in 2024, roughly 20% of global petroleum liquids consumption, yet repeated warnings have also taught buyers, shippers and navies how to prepare.

Why the strait still matters

The Strait of Hormuz is deep and wide enough for the world’s largest crude tankers, which is why it remains one of the oil market’s true choke points. The U.S. Energy Information Administration says about 20 million barrels per day moved through it in 2024, while the Congressional Research Service puts the share of global maritime trade at roughly 27% for crude oil and petroleum products and about 20% for liquefied natural gas.

Those figures are not abstract. The Center for Strategic and International Studies says nearly 15 million barrels of crude oil, more than 4 million barrels of refined products and 11 billion cubic feet of LNG pass through the strait on an average day. If that flow stopped, there are very few immediate substitutes with the same scale and geography, which is why even talk of disruption can move benchmarks fast.

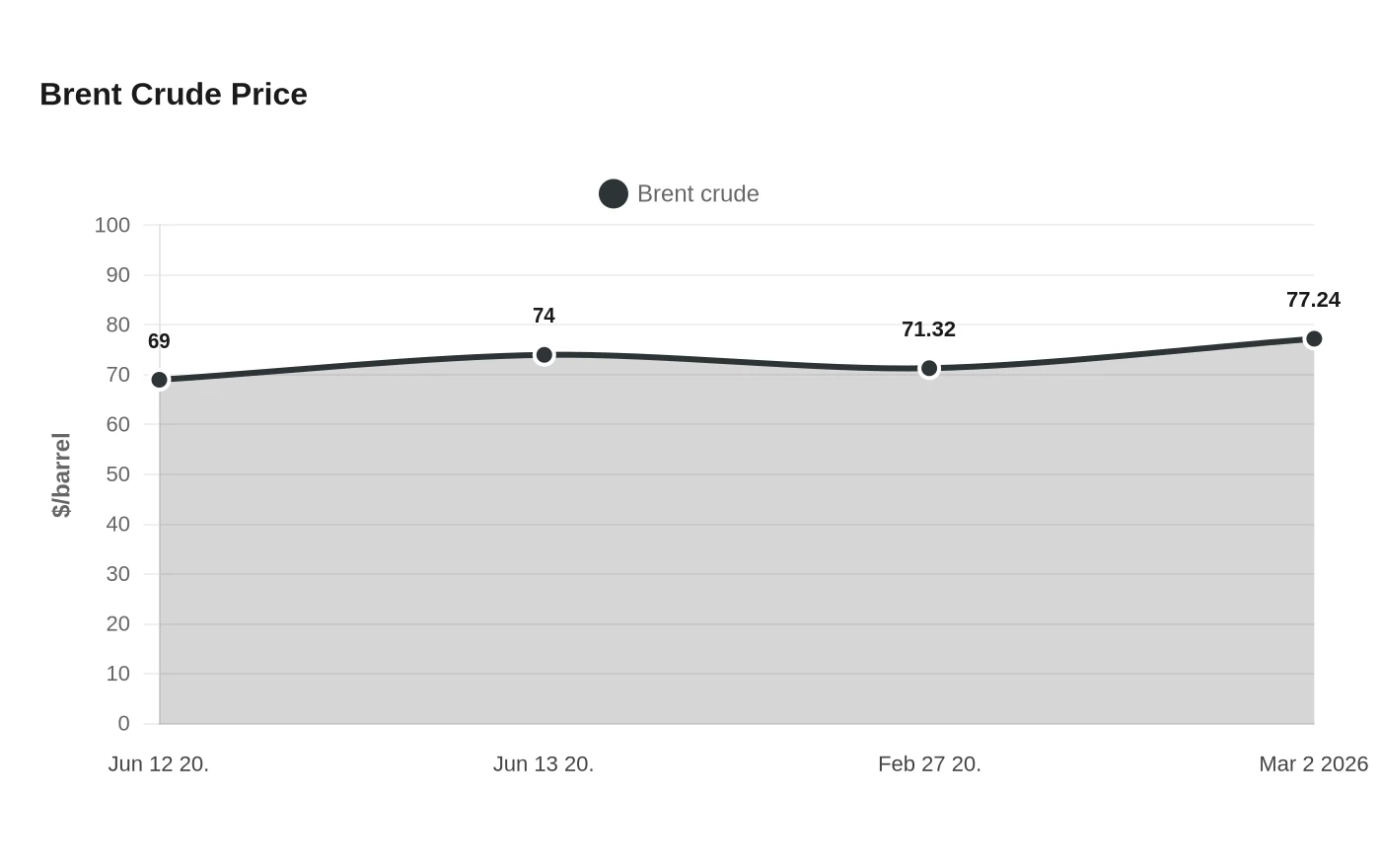

Markets still price the threat immediately

Oil markets do not wait for an actual blockade to reprice risk. In June 2025, the Energy Information Administration said Brent crude rose from $69 per barrel on June 12 to $74 on June 13 after regional tensions, a sharp move without any formal closure of the strait.

The same pattern repeated in the February-March 2026 conflict. A congressional report said Iranian forces declared the strait closed on March 4, 2026, and Brent climbed from $71.32 per barrel on February 27 to $77.24 on March 2. That is the market’s warning signal: even the threat of a shutdown can tighten supply expectations before a single tanker is turned back.

What has changed since Tehran first used the card

The leverage is still real, but the market has had repeated reminders and has started to adapt. The 2024 disruption around the Bab al-Mandeb Strait pushed Saudi Aramco to shift some crude flows from sea to the East-West pipeline, a route with limited spare capacity compared with total Gulf export volumes.

That matters because the alternatives are partial, not complete. CSIS estimates Saudi Arabia’s East-West Pipeline has about 2.7 million barrels per day of spare capacity after existing commitments, while the United Arab Emirates can reroute about half of its Gulf exports through pipeline connections to Fujairah. Those routes soften the blow, but they do not replace the Strait of Hormuz at Gulf export scale.

The result is a narrower margin for coercion. Tehran can still threaten the market, but buyers now know exactly which barrels can move elsewhere, which ones cannot, and how quickly rerouting becomes physically constrained. That makes every new warning less unique than the last.

Legal claims do not stop traffic, but they do not compel it either

On March 3, 2026, shipping-law specialists at Stephenson Harwood said a unilateral Iranian closure declaration would have no legal effect under the UN Convention on the Law of the Sea. The Strait of Hormuz is an international strait, so vessels of all states enjoy transit passage and the coastal state cannot suspend or block it.

Law, however, is only part of the calculation. Stephenson Harwood also said the wartime threat environment led major oil companies, trading houses and tanker operators to suspend shipments through the strait, and more than 250 vessels were idled in the area. That is the clearest example of a de facto closure: ships stop moving not because paper rules changed, but because the risk of attack became too high to ignore.

The human and military cost has made the bluff less credible

The balance changed further in the February-March 2026 conflict. The Sheffield Press reported at least 46 verified attacks on international shipping since February 28, 2026, with 10 seafarers killed and several others injured. In June 2026 statements, the International Maritime Organization said about 20,000 civilian seafarers remained in the Persian Gulf region, a reminder that the danger extends far beyond oil pricing screens.

This is where repeated use of the Hormuz threat begins to cut against Iran. The Congressional Research Service says Iran’s earlier disruption attempts in the Gulf brought it into direct conflict with the United States in 1987 and 1988. Each new round of pressure adds to the record that rivals can cite when building countermeasures, from convoy planning to rerouting and stockpiling.

Oman, navigation management and the limits of leverage

Oman has kept navigation management in the foreground by designating temporary routes and saying it would keep the strait open without tolls. That stance matters because it shows the regional response is no longer just rhetorical. It is operational, with route management and transit rules aimed at keeping oil moving even under pressure.

That is the essence of diminishing leverage. Hormuz still matters because the barrel count is enormous and the alternatives are incomplete. But the more often Iran threatens to close it, the more shipping companies, Gulf exporters and foreign governments move to reduce dependence, harden routes and call the bluff earlier. The chokepoint remains powerful, but its deterrent value is no longer what it was when surprise alone could freeze the market.

Sources

- [1]nytimes.com

- [2]eia.gov

- [3]congress.gov

- [4]csis.org

- [5]stephensonharwood.com

- [6]thesheffieldpress.com